Are you ready for the copper concentrate supply squeeze?

In 2025, the copper concentrate market faces unprecedented tightness as new smelting capacity collides with Indonesia’s export ban. Supply chains are being redrawn, trade routes redefined, and smelters are adapting in real time.

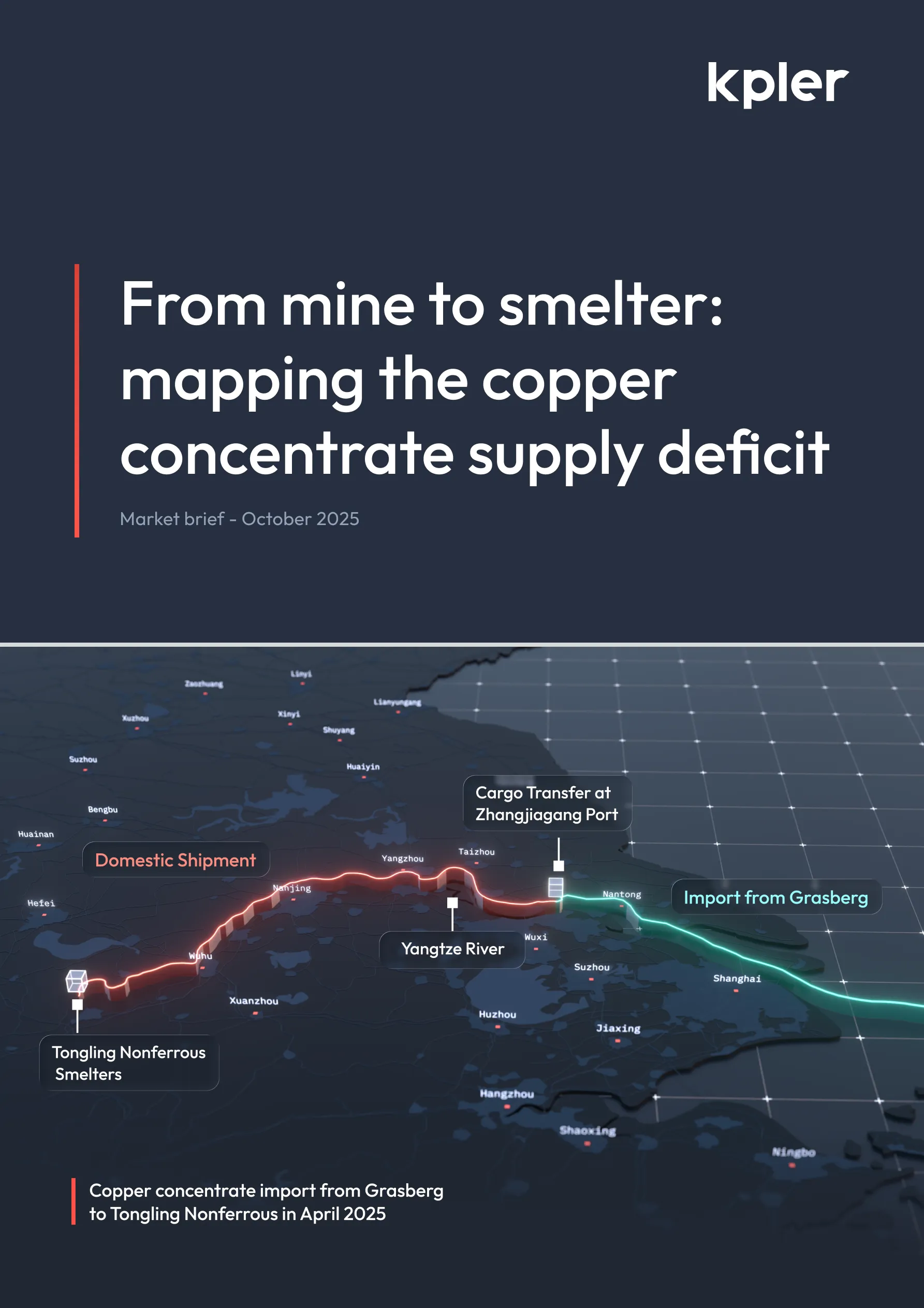

This whitepaper uncovers the full impact of these shifts, revealing where supply is being lost, who is securing volumes, and how the balance of power in the copper market is changing, all backed by Kpler granular trade flow data and facility-level analysis.

Ket takeaways

- How Japanese smelters are adapting to the loss of nearly 500kt of Indonesian concentrate.

- The rise of Adani’s new Kutch copper smelter, its 2mt feedstock strategy, and evolving plans at Birla Copper’s Dahej.

- How Chinese smelters are dominating supply, sourcing from major producers in Chile and Peru while expanding into niche markets such as Spain and Eritrea.

Access our free whitepaper to gain valuable industry insights:

“I rely on the Kpler Whitepapers to stay ahead of the latest market trends and industry insights.”

Michael Rodriguez

Chief Strategy Officer, Global Trade Inc

Known from...

%201.svg)