EU's staged fertiliser tariffs to increase costs for farmers through 2028

As part of reducing dependence on Russia, the EU’s reliance on Russian gas is now being replaced by dependence on Russian fertiliser. To address this, the EU has introduced staged fertiliser tariffs, which will rise from €40 to €430 per tonne by 2028. Over the next three years, these tariffs will make it nearly impossible to access Russian and Belarusian fertilisers, increasing reliance on alternative suppliers. As a result, prices for farmers are expected to rise, creating significant challenges for the agricultural sector.

European fertiliser prices have risen after the European Union announced additional tariffs on imports from Russia and Belarus. This decision aims to reduce Europe’s dependence on Russia by increasing additional tariffs in stages. This phased approach may allow time to boost domestic supply or increase dependency on imports from North Africa and the Middle East. However, it may lead to higher fertiliser prices for farmers and enable Russia to seek new markets, as additional factors such as Chinese quota-based supplies in the global market are already driving higher operating rates in countries like Russia and Iran, aiding in their market expansion.

After the tariff announcement, urea prices in France rose to €397.5/t, up €7 from last month. Simultaneously, DAP prices increased, making the EU more dependent on Morocco for phosphate fertilisers.

Urea granular and DAP prices FCA French (€/t)

Source: Argus

EU proposed additional import tariffs for Russia and Belarus, product-wise (€/t)

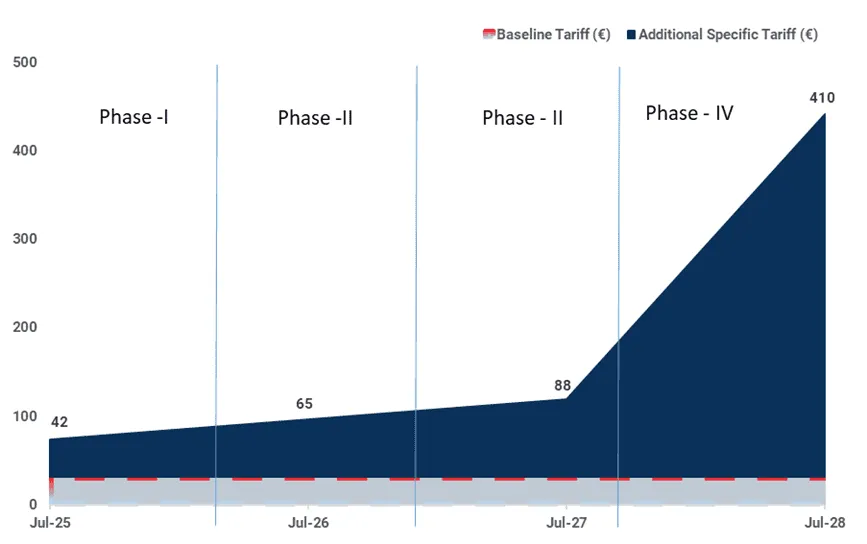

All tariffs on top of 6.5% import duty

Source: the EU

If the final text is formally agreed upon with EU members, tariffs will be implemented in stages starting from the first of July 2025. The goal is to raise tariffs from €40 to €430/t by 2028 over the next three years. This could stop imports from Russia and Belarus and reduce fertiliser dependence due to ongoing geopolitical tensions. However, there is apparent concern about how these higher costs will affect farmers and the agricultural market's stability in Europe.

The European Commission has suggested that if prices become excessively high, it may temporarily suspend the 6.5% import duty on fertiliser from non-preferential countries. This applies to suppliers outside Russia and Belarus, primarily from Eastern Europe, Central Asia, and certain Middle Eastern countries. However, the plan has not yet been announced. This approach indicates that the EU is attempting to strike a balance while ensuring fertilisers remain affordable for European farmers and preventing further market instability.

EU is heavily reliant on urea imports

EU relies heavily on imports of nitrogen fertilisers, particularly urea, to meet its demand. After Russia's invasion of Ukraine led to a rapid reduction in pipeline gas supplies to Europe, gas prices and nitrogen production costs soared. This resulted in a significant decrease in nitrogen production domestically. Consequently, EU urea imports surged from the usual around 4 Mt to 6.8 Mt, which has been sustained since then. These additional tariffs will affect the country's nitrogen supply the most.

EU urea imports from Russia and Belarus rose from 25% in 2023 to 33% in 2024

Source: GTT

Egypt, Russia, and Algeria are the main exporters of urea to the EU, making up over 85% of imports in 2024. Although Russia and Belarus accounted for 33% of urea exports, Egypt is still the largest supplier with 41%. When including Algeria’s 17%, the total supply from North Africa significantly increased that of Russia in 2024. As Algeria and Egypt do not have to pay the 6.5% import duty, Europe has become more reliant on these suppliers to meet import demand.

In July 2025, in the first stage, the €40/t tariff will reduce the competitiveness of Russian products compared to North African producers, but they will remain competitive with Middle Eastern products due to lower production costs and cheaper gas. Thus, Russia is expected to remain a key urea supplier during this stage. However, in the second stage with €60/t tariffs, competition with the Middle East will rise, initiating a supply issue that will affect Russian supply and create Europe as a more premium destination for other suppliers.

The tariff timeline: escalating costs to squeeze Imports

Source: European Commission

Europe is diversifying its fertiliser supply away from Russia, with increased imports planned from North Africa, the Middle East, and other regions. The availability of urea in the EU is expected to remain sufficient. However, price inflation is likely to impact the entire value chain. Additional import costs for Russian products, which are still part of the import mix, must be recouped. At the same time, as supply options tighten, the EU’s growing dependence on its two primary North African trading partners, Algeria and Egypt, is expected to drive up FOB prices.

This potential increase in fertiliser costs is a significant concern for the agricultural industry, particularly with the forthcoming implementation of the Carbon Border Adjustment Mechanism (CBAM) in January 2026. The CBAM will impose a tax on imported fertilisers based on their embedded carbon emissions. This new tax will coincide with domestic producers facing greater exposure under the EU Emissions Trading System (ETS). As a result, the overall cost floor for urea supply within the EU is expected to rise, putting additional financial pressure on the sector.

The council is expected to adopt the regulation without amendments. The upcoming tariffs are anticipated to impact Russian exporters negatively and increase costs for EU farmers, potentially affecting global food and fertiliser markets. As the EU shifts away from reliance on Russian gas, it is becoming dependent on Russian fertiliser instead. While this action signifies the EU's commitment to economic pressure on Russia, it may also lead to agricultural inflation in Europe.

Commodity news & research fueled by proprietary data

Kpler offers unbiased, expert-driven commodity research and news with daily, weekly, and monthly analysis across two services that are designed to deliver actionable trading and market intelligence. Don’t miss out on what thousands have already discovered and talk to our team today.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Expert research & analysis driven by proprietary data