Strait of Hormuz shock: Disruption is real but not indefinite

The market is facing a severe but likely temporary disruption. The key variable is duration, not capability. If Iranian military assets are neutralized within days, flows should partially recover and prices stabilize. If de facto closure persists beyond one week, production cuts across non-bypass Gulf producers become unavoidable, raising the risk of a materially tighter physical market.

Market & trading calls

- Bearish Dated Brent time spreads even as the Strait of Hormuz remains effectively closed, the risk-reward ratio to long here is limited.

- Bullish Dubai front spreads vs Brent as Middle East export risk disproportionately supports Dubai-linked grades, although a resumption of flows will ultimately pressure the front of the Dubai curve down.

- Bullish Russian delivered prices in India and China as Asian refiners are likely to increase Russian crude intake as a tactical buy, due to the willingness to secure alternative barrels.

1. Strait of Hormuz: de facto closure without a formal blockade

Two days after the outbreak of war between the US, Israel, and Iran, traffic through the Strait of Hormuz remains virtually halted. Iran has launched missiles at three vessels, yet the collapse in traffic is primarily precautionary. Shipowners are stepping back voluntarily, while insurance premiums have surged.

The next phase hinges on how quickly US and Israeli forces degrade Iran’s missile launchers, drone inventories, and senior leadership. Iran lacks the naval capacity to sustain a full physical blockade; its fleet is weakened, and missile stocks are finite and rapidly being depleted.

However, Tehran does not need a permanent blockade. Credible threats alone are sufficient to suppress transit. As long as a functioning leadership remains in place, Iran’s strategy is likely to mirror that of the Houthis in recent years: sporadic attacks that keep commercial traffic effectively frozen without requiring continuous escalation.

Given US military superiority, most of Iran’s combat-ready capabilities will likely be neutralised over the coming days. That should allow a gradual recovery in flows, but not an immediate normalisation. Even if the military threat diminishes, shipowners will remain cautious. Meanwhile, Iran’s widening attacks on regional infrastructure are likely to push Gulf states more openly toward supporting the intervention, accelerating Tehran’s strategic isolation. US General Caine today said that Saudi Arabia, Qatar and Jordan have “joined the fight”.

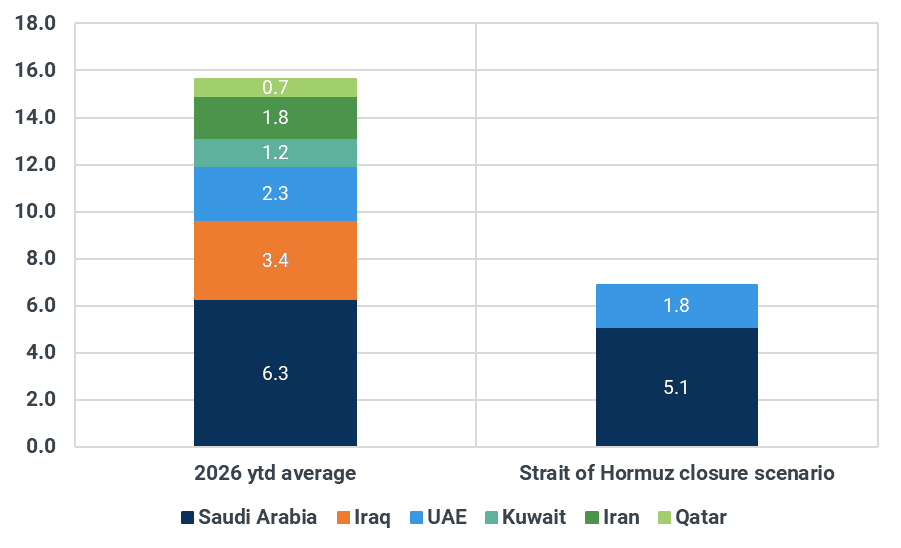

2. Bypass Capacity: Saudi and UAE Cushion, but 8.7 mbd at risk

Saudi Arabia and the UAE are already increasing utilisation of pipelines that bypass the strait. Saudi Arabia’s East–West pipeline links Abqaiq to Yanbu on the Red Sea. Capacity stands at around 7.0 mbd following recent expansions. West coast exports averaged ~813 kbd in 2026 YTD. We estimate current utilisation at roughly 38%, implying around 4.3 mbd of spare capacity.

In the UAE, we estimate the 1.5 mbd ADCOP pipeline is operating at 71% utilization, leaving around 440 kbd of spare capacity. ADNOC can temporarily raise throughput to 1.8 mbd if required.

Iran itself has the ability to ship crude from its Jask terminal on the Gulf of Oman, with capacity to handle ~350-400 kbd of crude. However, the terminal has only been used once until now, and with its loading volumes through February, NIOC doesn’t need to rush in using this option.

Even with these bypass options, around 8.7 mbd of crude and condensate remains at risk of disruption for several days. Iraq, Kuwait, Bahrain, and Qatar have no alternatives to Hormuz. Iraq cannot send Basrah crude to the north, apart via the use of trucks, which means volumes that could be brought from the south to Ceyhan ultimately would be very limited in terms of volumes (40 kbd at best). Despite reports of reduced southern Iraqi production, we understand output has so far remained steady. If the strait remains effectively closed for a week, however, production curtailments become almost imminent.

Medium-term crude flows impact from a Strait of Hormuz closure, mbd

Source: Kpler

This supply shock could incentivise additional purchases of Russian crude by Indian refiners. At the same time, elevated crude volumes already on the water in Asia-Pacific provide a short-term buffer. That floating cushion limits immediate price overshoot, unless the disruption extends beyond several days.

Crude and condensate on water in Asia-Pacific, mbbls

Source: Kpler

3. US/Israel hitting Iranian energy infrastructure remains a low-probability event

We assess direct US or Israeli strikes on Iranian oil and gas infrastructure as low probability. Washington’s priority remains containing oil price escalation. Targeting export infrastructure would not materially reduce Iranian revenues in the short term, but would sharply lift global prices, an outcome the US seeks to avoid.

Moreover, preserving core Iranian energy infrastructure serves a longer-term strategic purpose. Any future government in Tehran will depend heavily on oil exports to finance reconstruction. Destroying that capacity now would complicate post-conflict stabilisation.

Market insights you can actually trust

Kpler delivers unbiased, expert-driven intelligence that helps you to track critical crude oil market developments for your own analysis. Our precise forecasting empowers smarter trading and risk management decisions. In times of conflict and geopolitical uncertainty, our real-time data keeps you ahead of supply disruptions and price volatility.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler