Crude market adapts as Mideast supply gradually returns and demand lags

Crude markets are increasingly adapting to recent geopolitical and operational disruptions as Hormuz transit recovers, Canadian outages prove temporary, and Russian refinery runs rebound. However, weak Chinese buying and ample replacement barrels from the Americas are preventing tighter physical balances from translating into sustained strength across global crude differentials.

Market Calls

Executive Summary

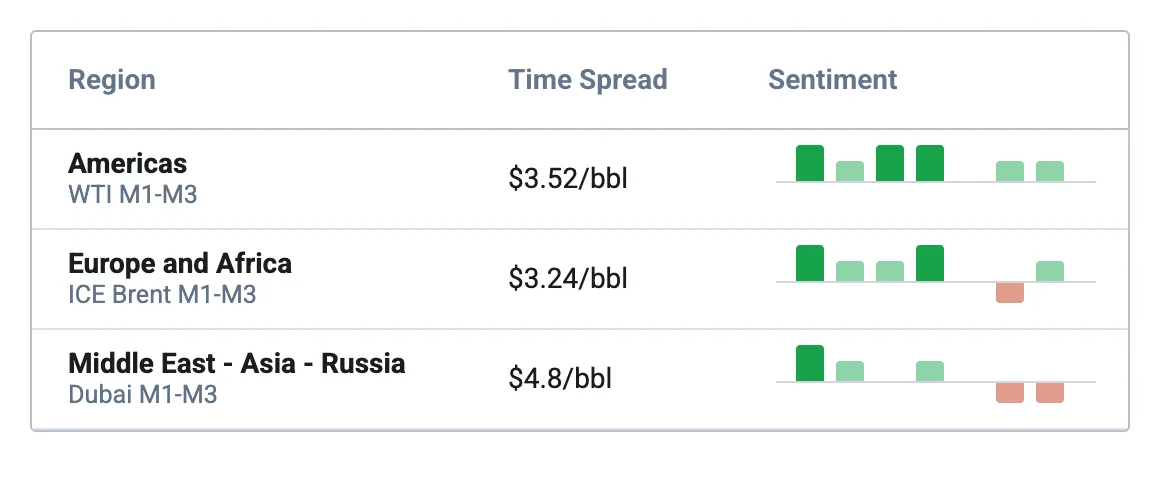

Americas:

- Pessimistic on Canadian supply throughout summer with extreme weather forecasts likely to continue and cause disruptions

- Optimistic on medium-term Canadian exports due to rapid work on tackling several infrastructure pinch points

- Slightly bullish on Medanito differentials with Cushing tank bottoms nearing, suggesting that less WTI will be available for seaborne export

Europe and Africa:

- Expected increase in Russian refinery runs of 350 kbd between May to July as various refineries complete maintenance after drone attacks.

- Stable on elevated LatAm crude flows to EU-27 in June as the Strait of Hormuz blockade shows no signs of resolving.

- Decrease expected for EU-27 crude inventories in July/August from current levels of 365 Mbbls amid peak summer demand.

Middle East, Asia and Russia:

- Bearish Dubai timespreads. Rising non-Iranian transit through the Strait of Hormuz and accelerating UAE production recovery are increasing prompt crude availability, easing immediate supply concerns.

- Bearish Murban-Dubai. Most of the incremental UAE exports consisting of Zakum crude, demand for the grade will narrow its spread against Murban.

- Neutral to slightly bearish Russian crude diffs into Northeast Asia. Chinese state-owned refiners remain reluctant buyers of Saudi crude despite a $6/bbl reduction in July OSPs, while Russian grades and Atlantic Basin alternatives continue to offer a significant delivered-cost advantage.

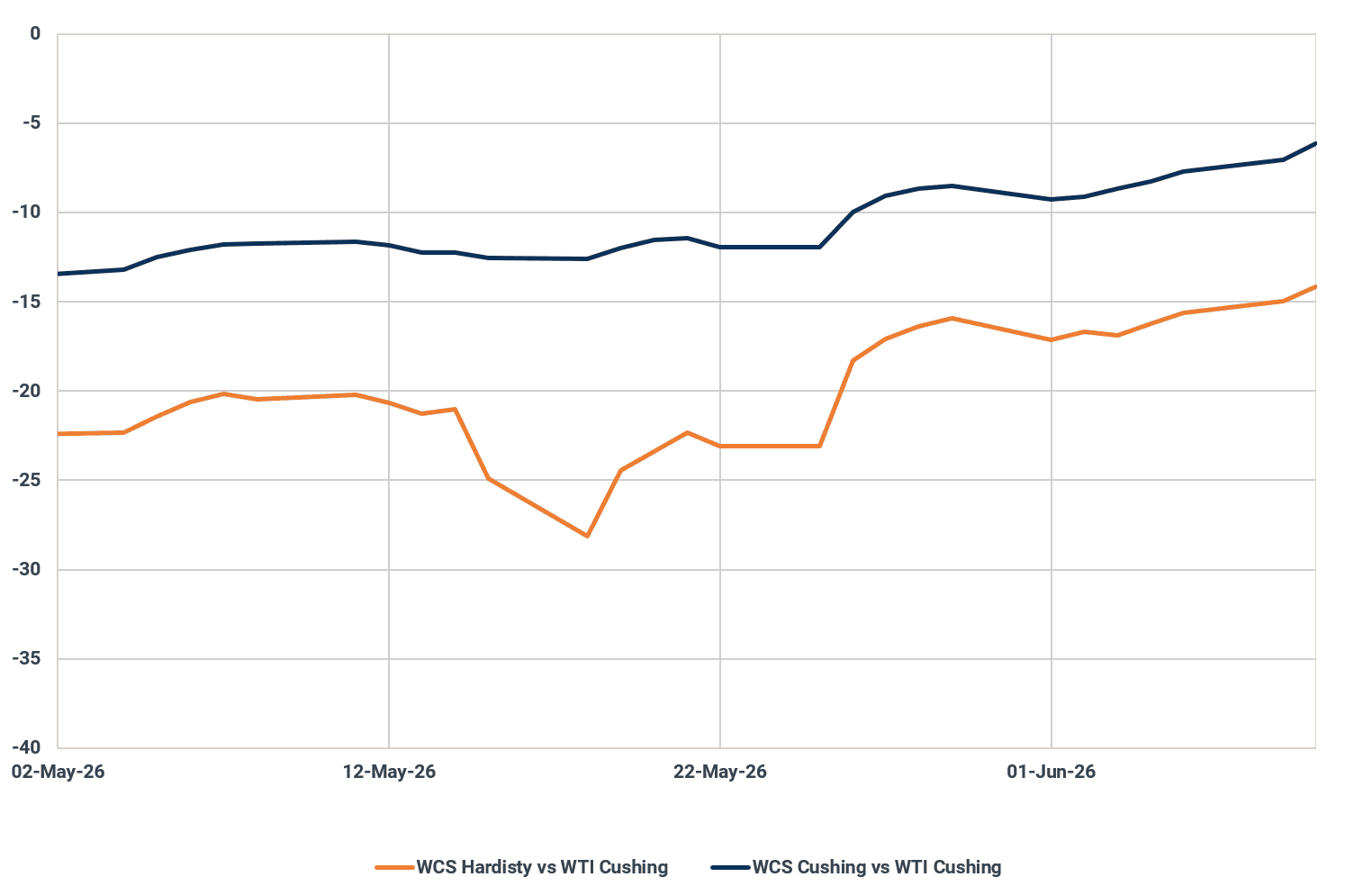

Americas: Extreme weather and Cushing levels could topple fragile balance

Extreme Canadian weather finally hits supply

Extreme weather events in northeastern Alberta, encompassing wildfires, flooding, and thunderstorms, have triggered critical power outages and forced Cenovus Energy to declare force majeure at its two largest oil sands assets. The disruption struck the Foster Creek and Christina Lake facilities last week, curtailing an estimated 4% of the firm’s bitumen output.

This sudden supply shock has aggressively tightened Canadian heavy sour balances, driving a sharp pricing divergence across the complex. The July-delivery Western Canadian Select (WCS) discount at Hardisty surged to around $12/bbl under the July CMA Nymex, hitting a three-month high (Argus Media). Concurrently, WCS at Houston narrowed to a near $2.70/bbl discount.

Conversely, this bitumen curtailment has entirely crushed regional condensate demand. With producers requiring significantly less diluent for blending, excess condensate is flooding the spot market. Consequently, Fort Saskatchewan condensate collapsed to a near $9/bbl discount against July Nymex, marking its lowest valuation since June 2022 (Argus Media). While recent heavy rains have brought all regional wildfires under control, the timeline for Cenovus' full operational recovery remains opaque, warranting a strictly bullish short-term outlook for heavy Canadian differentials.

WCS crude differentials to WTI, $/bbl

Source: Argus Media

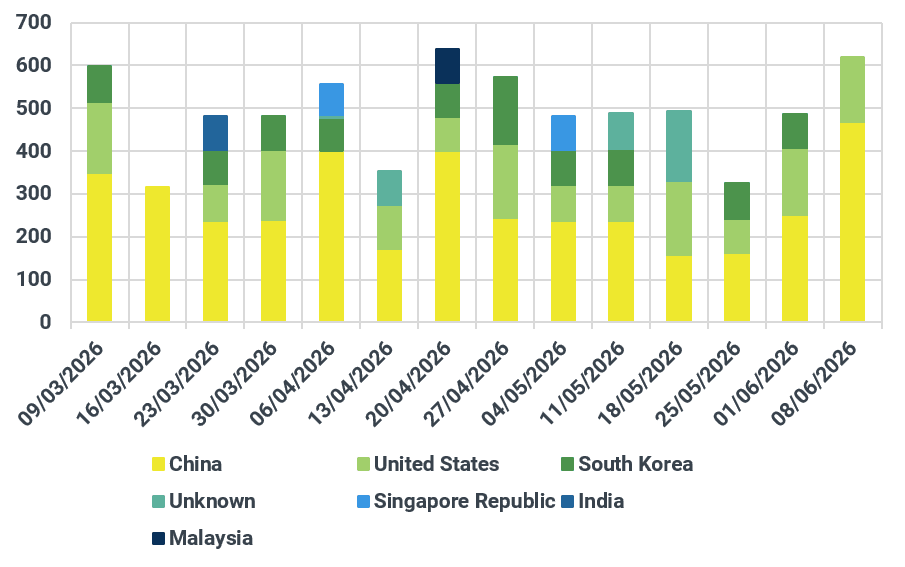

Canada focusing on infrastructure projects to boost exports

Canada is actively advancing critical infrastructure projects to maximize the export viability of its heavy crude, primarily focusing on marine logistics out of British Columbia.

The Vancouver Fraser Port Authority aims to commence essential dredging operations near the Second Narrows Bridge by late summer, contingent on final federal and environmental permits following a March public engagement phase. Currently, Aframax vessels loading at the Westridge Marine Terminal, which is fed by the newly expanded 890 kbd Trans Mountain system, are severely restricted by tide and draft limits, capping loadings at 550-600 kbbl.

The proposed dredging will unlock the ability to fully load these tankers up to 750 kbbl, fundamentally transforming the voyage economics for long-haul arbitrage flows into the Asia-Pacific basin.

In tandem with these port optimizations, Trans Mountain secured regulatory approval on 4 June for a 10% capacity expansion. By deploying drag-reducing agents, the federally-owned pipeline operators intend to inject an additional 90 kbd of throughput capacity as early as January 2027. In the immediate term, the recent upstream production curtailments across Alberta may unexpectedly ease the intense nomination pressures on Trans Mountain, potentially averting the severe June apportionments that shippers had anticipated following the pipeline's highly subscribed commercial launch

Weekly Westridge crude oil exports by destination, kbd

Source: Kpler

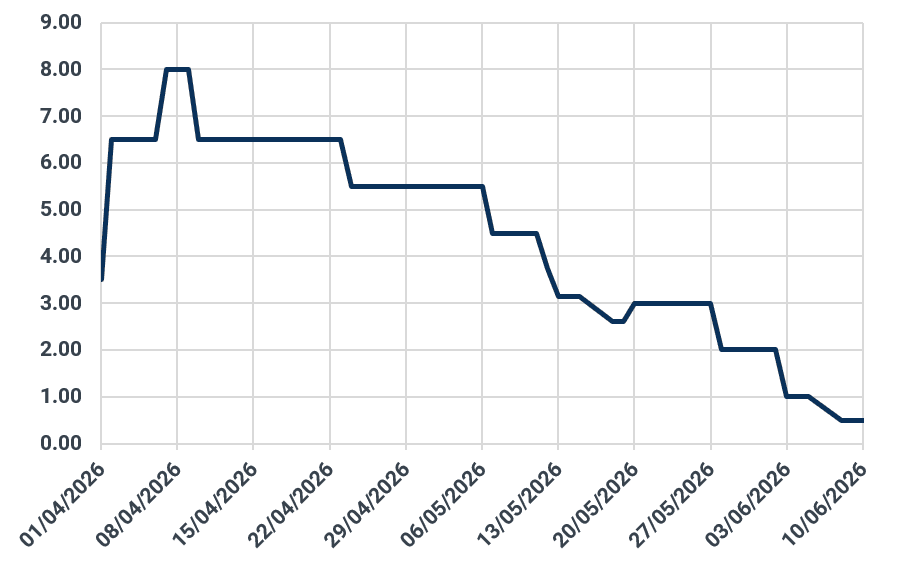

‘Balanced’ market weighs on Medanito diff, but Cushing draws could offer relief

Argentina’s light sweet Medanito crude is facing intense downward pressure, with its premium to ICE Brent falling earlier this week to its narrowest margin since 13 March.

As participants trade the first August-loading cargoes, Medanito's premium has sharply narrowed to just $0.50/bbl against October ICE Brent, from $1/bbl in previous trade (Argus Media). This brings the crude down to pre-war levels on an outright price basis.

This bearish correction is driven by a more balanced spot market, and in Asia, the availability of the UAE's light sour Murban at highly competitive prices is disincentivizing Asian buyers from seeking Atlantic Basin alternatives.

Simultaneously, Medanito faces aggressive competition along the US West Coast, where narrower premiums for the competing Alaska North Slope grade are further suppressing Argentinian values. Consequently, the July trading cycle was extended by two weeks as sellers stubbornly attempted to maintain the record-high premiums captured during June.

Looking ahead however, the low Cushing inventories as we approach peak summer demand is already incentivising more WTI barrels to stay domestically, which could open opportunities for other Atlantic barrels, such as Medanito.

Medanito differential to ICE Brent, $/bbl

Source: Argus Media

Europe and Africa: EU-27 crude inventories are up for a downwards correction

Recovery in Russian refinery runs should weigh on crude exports in June

As previously reported by Kpler, Ukrainian drone strikes on Russian refineries since March have significantly disrupted domestic processing capacity. As these extensive refinery outages curtailed domestic crude demand, Russian crude and condensate exports averaged close to 3.9 Mbd in May, reaching multi-year highs. However, export volumes are likely to ease in June as refinery operations gradually recover. We estimate that Russian crude demand fell from 5.3 Mbd in March to 4.85 Mbd in May, but expect a rebound to around 5 Mbd in June and 5.2 Mbd in July.

Maintenance and repair work is being completed at several major facilities, including the Volgograd, Syzran, Saratov, and Ryazan refineries. As a result, offline refining capacity is expected to decline sharply from roughly 2.9 Mbd in May to just 300 kbd by July (IIR). The recovery in refinery runs is also being supported by seasonal growth in fuel demand and efforts to avoid domestic fuel shortages.

At the same time, we expect Russian crude and condensate production to increase modestly to 10.14 Mbd in June, before rising further to 10.2 Mbd by August. Additional upside may come from the normalization of crude flows through the Druzhba pipeline to Hungary and Slovakia.

Russian crude and condensate exports, kbd

Source: Kpler

More Syrian crude finds its way to the EU-27

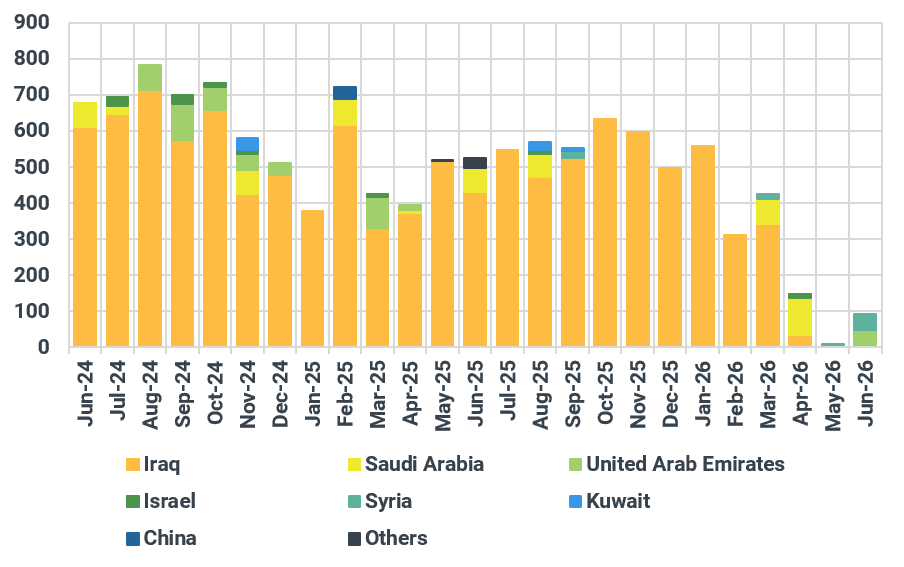

Crude imports into the EU-27 and the UK ended May at 10.37 Mbd, slightly below April levels, as arrivals from the Middle East and Asia fell to near-zero levels. While April still saw around 70 kbd of Saudi crude from Ras Tanura and 35 kbd of Iraqi crude arrive in Europe, these cargoes had departed in late February, before the outbreak of the conflict. May imports included a 260 kb cargo of Syrian crude, which discharged at the port of Trieste on 13 May. Another Syrian cargo, carried onboard the Minerva Kythnos, arrived in Trieste on 7 June. This latest delivery marks only the fourth recorded arrival of Syrian crude into the region, following the first two deliveries in September 2025 and March 2026.

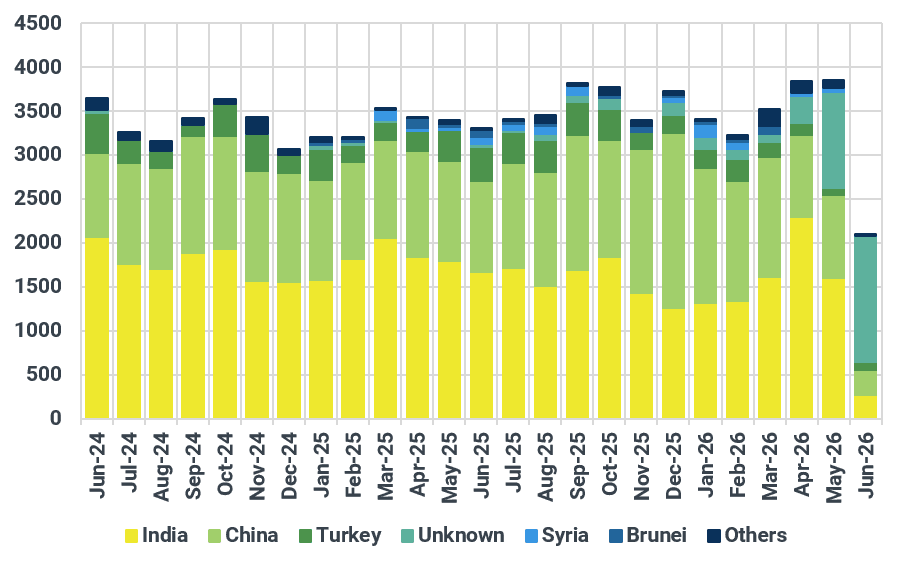

To compensate for the loss of Middle Eastern barrels, which historically averaged around 500-600 kbd, crude imports from the Americas surged above 4 Mbd in May, reaching a record high. The increase was driven primarily by a 600 kbd m/m rise in US crude imports, alongside stronger inflows from Brazil, Mexico, Venezuela, and, to a lesser extent, Colombia.

US crude exports to the bloc climbed to 2.4 Mbd, with most incremental volumes heading to the Netherlands, Italy, and Germany. Meanwhile, the Netherlands emerged as a notable buyer of Venezuelan crude, receiving three Merey-laden vessels in May—the first such arrivals since late 2019. We expect crude inflows from the US to decrease in June and July amid falling US crude inventories and elevated US crude prices.

EU-27 crude imports from EoS, kbd

Source: Kpler

Stable EU-27 crude inventories reflect ample oil availability

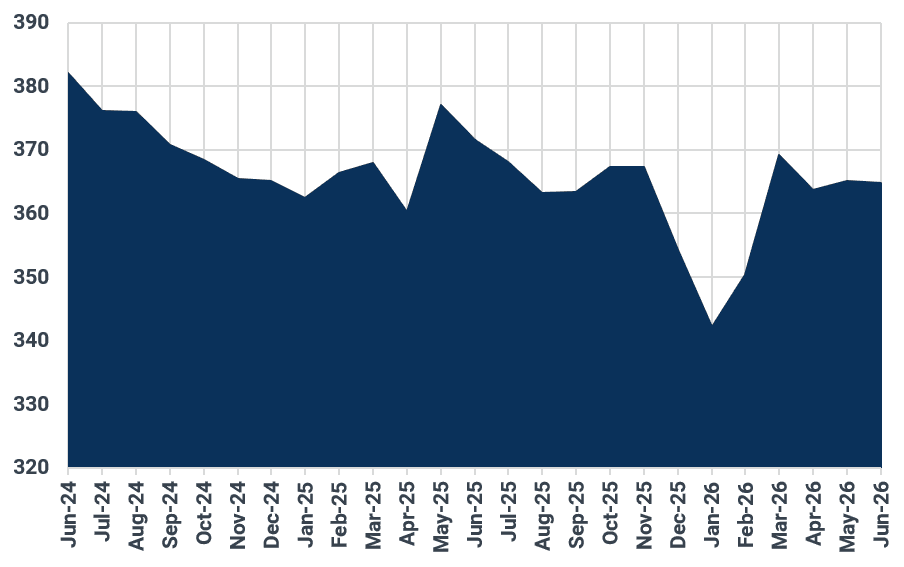

Amid stable crude imports into the EU-27 and the UK, crude inventories across the region remained broadly unchanged in May, averaging 365 Mbbls. Stocks were largely in line with April levels and only 4 Mbbls below those recorded in March. Crude inventories remain concentrated in key storage hubs, including Germany, the Netherlands, France, Italy, Spain, and the UK. It should be noted that strategic petroleum reserve (SPR) volumes cannot be fully tracked in some countries, particularly where stocks are held in underground storage facilities, such as in Germany.

At first glance, stable inventory levels may appear counterintuitive given the significant Middle Eastern supply disruptions caused by the US-Israel conflict. Yet physical crude market indicators show that Europe remains well supplied. The North Sea Dated (NSD) M1-M3 spread has narrowed sharply from the elevated levels seen in early April, falling to around $3/bbl in late May before recovering modestly to approximately $6/bbl by mid-June. In line with this, crude differentials across the North Sea, Mediterranean, and West African markets have steadily weakened over the past two months.

These developments indicate that the global crude market has largely adapted to the reshuffling of trade flows following the loss of Middle Eastern barrels. Strong replacement supplies from the Americas have helped offset disruptions. Still, we expect EU-27 and UK crude inventories to decline during July and August. Lower US crude arrivals, combined with higher regional refinery runs during the peak summer demand season should gradually tighten crude availability and draw down stocks from current levels (we see EU-27 crude demand rise to 10.3–10.4 Mbd during July and August, roughly 400 kbd above June levels).

EU-27 and UK crude inventories, kbd

Source: Kpler

Middle East, Asia, and Russia: Higher Hormuz flows and weak Chinese demand weigh on price diffs

Strait of Hormuz transit nears 3 mbd as disruption continues to ease

Transit of non-Iranian crude and condensate through the Strait of Hormuz continues to recover, with flows reaching 2.9 mbd in June month-to-date, the highest level since the start of the conflict. Most of the increase originates from the UAE, although Iraqi and Kuwaiti exports have also strengthened. A further 1.56 mbd remains difficult to attribute, with cargoes transferred via ship-to-ship operations in the Gulf of Oman near Fujairah.

The recovery likely reflects improved security conditions. President Trump recently stated that around 100 mb of oil had transited the strait over the past month, broadly consistent with Kpler tracking of 98 mb since 1 May. This suggests some level of US-backed protection for commercial shipping. At the same time, diplomatic engagement between Iran and the UAE may be reducing regional tensions and facilitating greater movement through the waterway.

Nevertheless, conditions remain highly constrained. Around 80% of transits are now conducted via dark activity. Total crude and condensate exports exiting the Persian Gulf averaged 3.76 mbd month-to-date, although this includes 695 kbd of Iranian crude that remains stranded in the Gulf of Oman due to the ongoing US blockade. This is still far from pre-war levels of ~15 mbd.

Persian Gulf crude and condensate transiting through the Strait of Hormuz, mbd

Source: Kpler

Inventory draws support export recovery while UAE production rebounds

The recent increase in Persian Gulf exports has been driven primarily by inventory withdrawals rather than a full recovery in upstream production. Since late April, floating storage volumes in the Persian Gulf, excluding Iran, have fallen by 69 mb. The largest declines have been recorded in Basrah Medium (-13 mb), Arab Extra Light (-8 mb), Arab Light (-7 mb), and Das (-7 mb), reflecting the release of barrels that had remained idle for extended periods.

Kuwait has relied heavily on onshore inventories to maintain exports, with estimated storage levels declining by 7.6 mb over the past two weeks, equivalent to roughly 580 kbd. In contrast, the UAE has begun restoring production capacity. Increased activity at Upper Zakum and Das, together with a notable rise in Adnoc tenders, points to a gradual normalization of output. Recent sales included 12 mb of Upper Zakum crude awarded primarily to Asian buyers, while Adnoc has also marketed Zakum barrels from Sidi Kerir into the Mediterranean, a rare move highlighting the search for alternative outlets.

As a result, we have revised UAE crude production higher to 3.18 mbd in May, from 2.60 mbd in April and 2.28 mbd in March, although output remains around 720 kbd below pre-war levels.

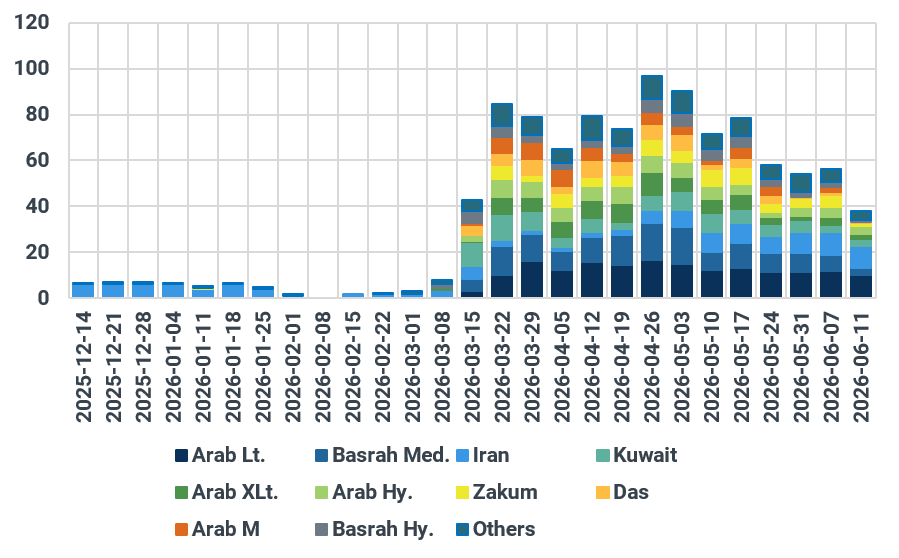

Persian Gulf oil in floating storage by grade, mb

Source: Kpler

Chinese demand remains weak despite lower Middle Eastern price diffs

Despite improving export availability from the Persian Gulf, demand signals from China remain weak. Sinopec has not nominated any Saudi crude cargoes for July loading, despite Aramco reducing Asian OSPs by $6/bbl. Arab Light remains priced at a premium of $9.50/bbl to Oman/Dubai, leaving it uncompetitive against alternative feedstocks.

With the Brent-Dubai EFS near $9.60/bbl, freight-adjusted delivered costs place Arab Light more than $10/bbl above ICE Brent into Northeast China. By comparison, Brazilian Tupi and Norwegian Johan Sverdrup are delivered at roughly +$7–7.50/bbl, while Russian grades remain substantially cheaper at around +$1.50/bbl for ESPO and -$1/bbl for Urals.

The combination of rising Gulf export availability, weak Chinese buying, and stronger domestic refinery demand in western Saudi Arabia has reduced exports from Yanbu. Shipments fell by 400 kbd to 3.74 mbd in May after the East-West Pipeline reached maximum throughput in April.

Chinese refining margins remain under pressure and refinery run rates continue to weaken, particularly among state-owned processors that rely on non-sanctioned crude. While Russian arrivals have lifted imports modestly month-to-date, seaborne crude imports are likely to remain close to May's low of 6.7 mbd, limiting support for Middle East crude differentials.

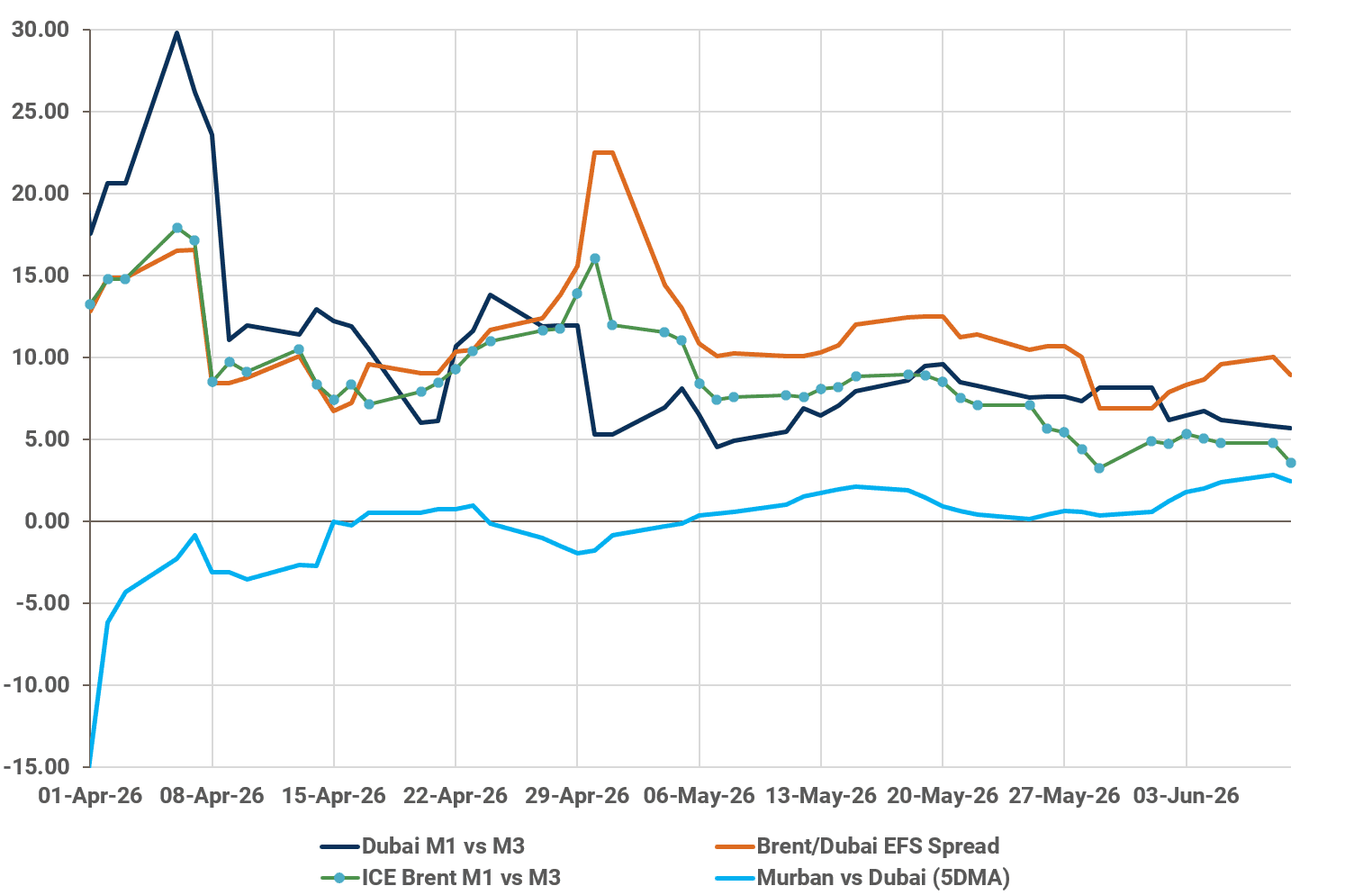

Key Asian market structures, $/bbl

Source: Argus Media

See why the most successful traders and shipping experts use Kpler