Delicately balanced

The USGC refining system has quietly been doing some heavy lifting. Strong US production has kept European import volumes healthy while simultaneously absorbing demand from Latin American and African buyers displaced by renewed drone strikes on Russian export infrastructure. For now, flows work and the barrels are moving. But this is a thin margin of comfort. The transatlantic arb is sensitive to freight, refinery run rates, and crack spreads that can shift fast. A tumultuous USGC hurricane season could close this window quickly. The market is balanced, not buffered.

Market & Trading Calls

Gasoil/diesel

- Slightly bearish WoS: Strong USGC output is keeping European import volumes healthy while simultaneously allowing US refiners to absorb Latin American and African demand affected by renewed drone strikes on Russian export infrastructure.

- Slightly bullish EoS: The NDRC's formalized run-cut floor — 80% of year-ago output — makes a large July Chinese export program unlikely, keeping regional supply tight until South Korean refiners clear maintenance and return to full run rates.

Jet/kero

- Slightly bearish EoS: Above-trend US production and healthy PADD 5 arrivals from elsewhere have reduced Asian outflows, keeping the region largely self-sufficient. Price-responsive demand reduction has done the rest of the rebalancing work.

- Neutral WoS: Airline and refiner assurances of adequate summer supply, backed by high continent-wide production, have taken the sting out of spot prices near-term.

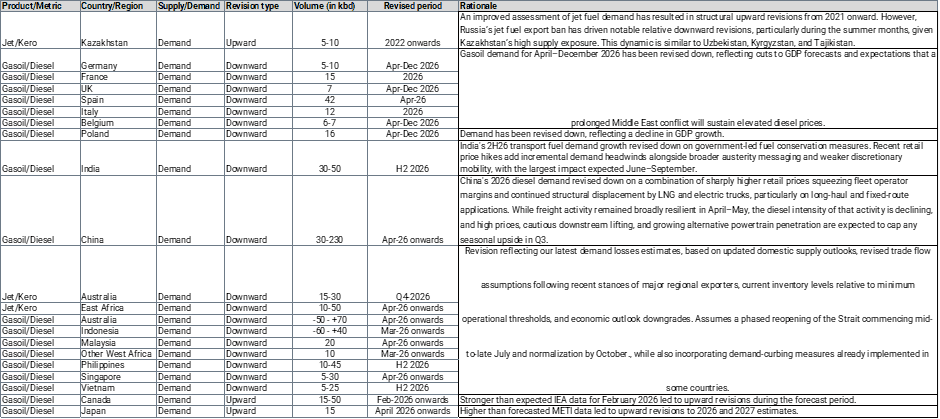

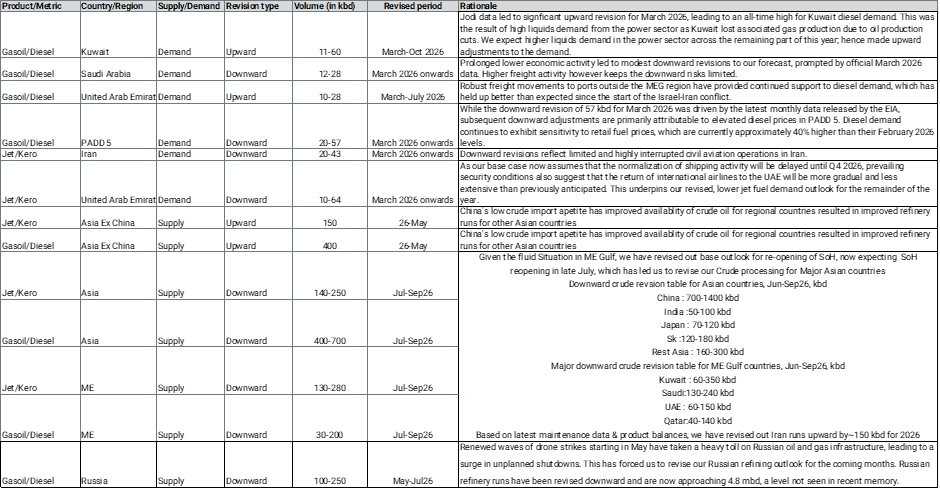

Middle Distillates S&D

Table of Supply and Demand revisions

Source: Kpler

Global middle distillate balances have tightened further in our June outlook edition, by ~680 kbd for June–September versus the previous edition. The tightening is overwhelmingly supply-driven, following downward revisions to crude run assumptions across Asia, the Middle East and FSU East after incorporating our updated de-escalation scenario into our refinery outlook, which now assumes a phased reopening of the Strait commencing mid-to-late July and normalization by October, instead of September.

Delving deeper into gasoil balances, during the summer months, balances are expected to tighten by an average of ~1070 kbd versus last year, expectations of lessened supply from the Middle East and Asia (mainly China) as the conflict drags on have been juxtaposed with a worsening supply outlook from Russia.

Russian refinery operations continue to face disruptions from ongoing Ukrainian drone strikes. Refinery runs have remained near multi-year lows during April–May, sitting below 5.0 Mbd, as outages, maintenance and operational disruptions impacted more than 2.0 Mbd of refining capacity. May middle distillate production fell sharply by ~320kbd, while seaborne exports fell sharply, ~270 kbd lower y/y, further tightening availability from the region at a time when global middle distillate markets are undersupplied, and should largely continue to be for as long as the Strait of Hormuz remains effectively closed. As a result, Russian gasoil exports to Brazil fell by ~100 kbd y/y. To cope with this lower supply, we are seeing higher crude runs in Brazil; accordingly, we have raised our Brazilian crude run estimates by ~70 kbd over April–July versus our last update. Looking ahead, Russian refinery runs are expected to average around 4.9 mbd in June, constrained by residual maintenance and continued drone attacks. Runs should recover modestly to around 5.1 mbd in July as maintenance winds down, although downside risks remain elevated due to ongoing operational disruptions.

Within the Atlantic Basin, US refineries continue to operate at elevated utilisation rates, supported by favourable middle distillate economics. Therefore, any unplanned maintenance can have a major impact on already tight refined product balances.

During the summer months, we have also revised gasoil/diesel demand lower by ~190 kbd, mainly across Asia and Africa (~120 kbd and ~90 kbd respectively). Offsetting part of the expected further supply losses versus last month’s outlook, India and Southeast Asia have undergone material downward revisions to their H2-2026 demand. Indian demand is down on government-led conservation measures and price hikes.

On a side note, PADD 5 is leading the downward demand revisions in the US, where we have revised gasoil demand lower by ~20 kbd owing to high fuel prices, which have risen ~50% since the conflict started.

Turning to jet fuel/kerosene, over June–September, global jet fuel balances are forecast to tighten by ~150 kbd, primarily on a ~240 kbd downward supply revision. Asia and the Middle East each see supply cut sharply by ~200 kbd each, though we have raised supply forecasts for Europe and North America by ~120 kbd and ~60 kbd respectively, driven primarily by optimisation to maximise kerosene recovery. That said, inventory drawdowns are still expected, and Europe remains poorly positioned to secure jet fuel supply. On the demand side, jet has been revised down by ~100 kbd over the same period, globally, as elevated jet prices have increasingly pressured airline economics, prompting several carriers globally to rationalise capacity and suspend selected routes that have become commercially unviable.

Further out, however, we expect some lengthening in middle distillate balances from our previous outlook by ~340 kbd over October 2026–March 2027, driven mainly by sharp downward demand revisions for diesel and jet of ~200 kbd and ~100 kbd respectively on GDP downgrades across regions, particularly Asia, Africa and the Middle East, coupled with expectations that higher diesel and jet prices will keep demand depressed for longer. Once supply returns, particularly into next year, we expect surplus barrels in the market. Global middle distillate balances are expected to increase by ~1,200 kbd y/y in 2027, driven by a ~1,900 kbd rise in supply, which should allow global inventories to rebuild.

See why the most successful traders and shipping experts use Kpler