Demand headwinds weigh on dry bulk commodities

Iron ore prices nudged higher but look set to soften again as demand falls in China and Japan, even as Hancock Iron Ore ramps up its new McPhee Creek mine. Coal markets are holding steady, with China's peak season off to a slow, rain-delayed start and Turkey returning to the market as hydro output fades. In grains, China's soft demand continues for US agricultural goods, as underwhelming soybean sales and the absence of corn or wheat purchases test confidence in previous commitments. Aluminium extends its recent slide despite an undersupplied market, and dry bulk freight sentiment diverges, with Capesize and Panamax earnings firming while Supramax and Handysize rates lag.

Iron Ore & Steel: A brief bounce, capped by weak demand and slipping freight rates

- Iron ore prices edged slightly higher over the past week, with the most traded iron ore price benchmarks rising 0.7% w/w. The DCE contract, September 2026 closed at 740 yuan/t on 2 July and the SGX 61% Fe August contract was trading at $98.25/t at the time of writing. Iron ore futures jumped briefly as CMRG reported restrictions on imports of FMG’s Super Special Fines and Fortune Fines, before paring some gains later. We expect this to have little effect on prolonged pricing. It echoes a similar move against BHP last year, when China continued to import BHP products during the company’s pricing dispute with CMRG. We expect prices to remain subdued over the next few weeks as demand from China (structural slowdown) and Japan (summer maintenance shutdowns) fall. India is entering a seasonal lull for crude steel output, but the monsoon typically lifts iron ore if mining and haulage activities are disrupted.

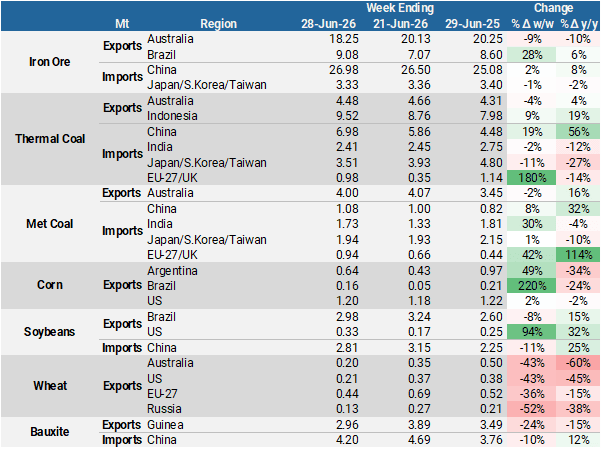

- Global seaborne iron ore exports rose 3% w/w to reach 34.19Mt in the week ending 28 June, but volumes remained 4% lower y/y and below the five-year average of 35.07Mt.

- Australian shipments stood at 18.25Mt, down 10% y/y, as exports to China and Japan weakened.

- Brazil iron ore shipments, by contrast, surged 8% y/y to 9.13Mt as miners ramped up volumes during the final week of the month to meet quarterly guidance targets.

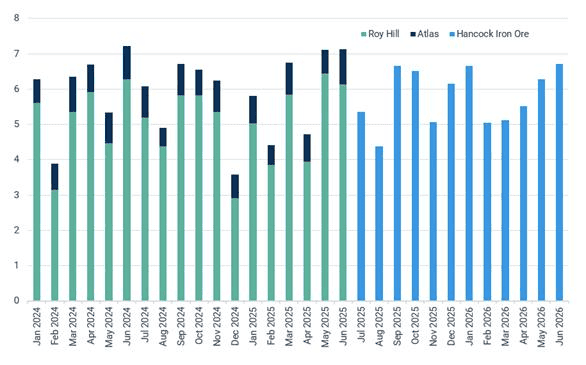

- Hancock Iron Ore has produced first iron ore at McPhee Creek, its newest Pilbara mine in Western Australia. Using the satellite orebody model, McPhee Creek will haul primary crushed ore to Roy Hill (Hancock's flagship operation) for further processing and blending.

- Effective July 2025, Roy Hill and Atlas Iron merged into a single brand, Hancock Iron Ore, giving a combined nameplate capacity of ~72Mtpa across four operating mines: Roy Hill and the former Atlas trio - Mount Webber, Sanjiv Ridge, and Miralga Creek. Hancock also holds a 50% stake in Hope Downs, a joint venture with Rio Tinto.

- Hancock shipped 61.3Mt of iron ore in 2025 from Roy Hill via the Stanley Point installation, largely bound for China and the JKT region, plus a further 8.8Mt from Utah Point (the Atlas mines), all bound for China.

- With Roy Hill's shipments softening and the Mt Webber orebody ageing, Hancock has designed McPhee Creek's 8-9.5Mtpa output to backfill Roy Hill's processing capacity rather than add a wholly separate export stream. This comes as higher-grade West African supply increasingly contests the competitive floor under Australian ore.

Hancock iron ore exports ramp-up in June 2026 (Mt)

Source: Kpler

- On the demand side, Chinese seaborne iron ore imports rose a 8% y/y to 27.06Mt in the week ending 28 June despite the broader demand lull.

- Shipments from FMG and Rio Tinto rose 27% y/y and 19% y/y respectively, while BHP and Vale saw a drops of 22-24% y/y.

- Iron ore inventories at Chinese ports fell slightly on modest increase in hot metal output, but buying interest continues to remain weak.

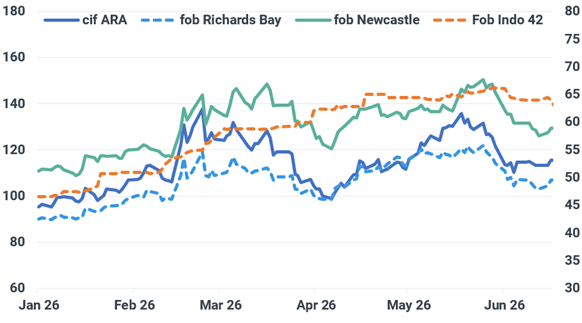

Coal: China returns to growth, Turkish utilities to boost coal burn

- Coal markets have stabilised after the wider energy complex moved lower in response to Iran/US peace deal possibilities. The extended force majeure at Qatar Energy and the start of peak demand season will keep prices elevated, despite a lack of actual coal demand from the EU. QatarEnergy extended the force majeure notice on 30 June, taking the total number of affected LNG cargoes for Italy's Edison to 21 between April and early September, equivalent to around 2 Mt of LNG. Edison has replaced 14 of these cargoes and says it holds sufficient alternative supply to meet customer demand.

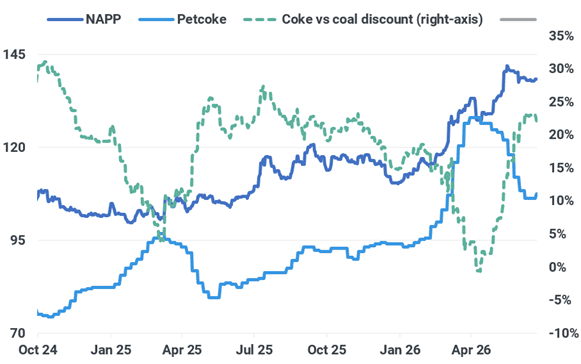

Month-ahead paper coal prices ($/t, fob Indo 4,200kcal/kg in secondary axis $/t)

Source: Marketview

- China had a weak start to peak demand season. The country's southern belt and hydro basins received strong rainfall in June, and rainy conditions are forecast to continue until the end of next week, improving supply availability. Demand will strengthen once temperatures rise above seasonal norms and dry conditions prevail. Early indicators show coal production for June was lower and mine utilisation July will be lower y/y, limiting domestic supply as well. Coastal coal inventories in China's eight coastal provinces rose by around 155,000t w/w. Daily coal consumption in the region fell by around 300,000t/day w/w, a 14.78% drop. Coal inventories in the Bohai Rim ports in northern China now sit above 2025 levels. But the main seasonal drawdown has not started, as high rainfall in June boosted hydropower generation and reduced cooling demand for power.

Coal inventories at China’s Bohai Rim (Mt)

Source: Sxcoal

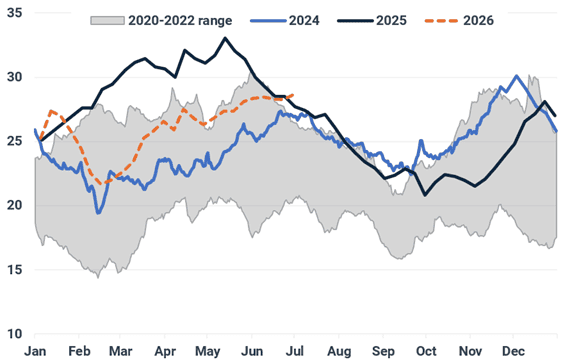

- Turkey is returning to the coal market after a period of weak coal burn, caused by high hydro and solar output that increased supply availability in the Atlantic basin in recent months. Hydro output will gradually decline, and power prices will start to reflect the generation costs of thermal utilities, bringing coal back into the picture. Russian coal producers will be the main beneficiaries of this, as they have limited alternative markets in the Atlantic basin. Higher Russian coal prices might move the needle in favour of petcoke for cement users, who have taken advantage of cheap Russian coal supply due to a lack of demand from the power sector.

- India remains on the sidelines of the coal market, as utilities and domestic industries increased domestic consumption. We expect India to return to the market in the coming months, as the rain season reduces domestic production. Petcoke demand faces some destruction in the cement industry, as kilns increase petcoke's share in their fuel mix after petcoke gained competitiveness against coal.

India delivered US coal vs petcoke pricing ($/t, %)

Source: Argus, Kpler Insight

Grains & Oilseeds: Lower US corn stocks question balance sheet fundamentals

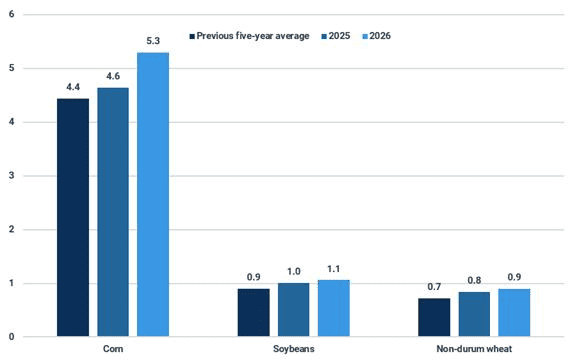

- In the USDA’s latest quarterly stocks report, corn was seen at 5.3 Bn bu, soybeans 1.1 Bn bu, and non-durum wheat 0.9 Bn bu as at the start of June. Though soybeans and wheat stocks were in line with what had been expected, corn stocks were surprisingly low relative to this year’s supply, offering some support to CBOT corn. However, the explanation behind the lower-than-expected corn stock is uncertain, as feed and residual is already beyond what could be reasonably expected. Therefore, some in the market believe this highlights that 2025 US corn production was overestimated and could be subject to revision.

US grain stocks at start of June (Bn bu)

Source: USDA

- For the USDA’s June Acreage report, corn acres were unchanged at 95.3 M ac while soybeans were increased by 0.7 M ac to 85.4 M ac. This keeps the corn planted area at the fourth highest level in over eight decades and brings soybeans in line with the previous five-year average. The report also offered a revised outlook for the 2026 wheat area. At 40.9 M ac for non-durum wheat, this would be the lowest area since records began. Adding to the production challenges, the harvested area is also lower y/y at 74%, as poorer quality saw more of the winter wheat crop used for grazing cattle instead.

- By 18 June, US soybean sales for the next marketing year totalled 2.2 Mt, with China accounting for 0.2 Mt. Furthermore, sales to unknown destinations are at 1.4 Mt, the highest for this time of year since 2022, raising speculation that Chinese sales could be slightly higher than is currently stated. Nonetheless, recent pace of Chinese sales is underwhelming, and the current pricing of US soybeans implies that the market is not convinced that the 25 Mt commitment will be upheld. Moreover, despite the $17 bn purchase agreement across all other US agricultural commodities, China is yet to purchase any corn or wheat.

- Brazilian soybean exports finished at 14.2 Mt in June, making the fourth consecutive monthly record for exports this year. At least 10.3 Mt was destined for China. Cumulative seaborne volumes from Brazil to China are at 68.7 Mt this marketing year since September, significantly above last year’s 59.7 Mt. After importing at last year's pace from Brazil, China only imported 12 Mt from the US. Even that required a political deal. Given the much higher pace of imports from Brazil this year, China’s fundamental need and commercial appetite for the promised 25 Mt, over double last year’s volume, from the US 2026 harvest is questionable.

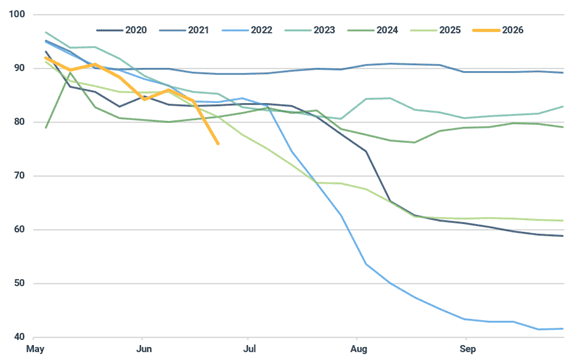

- The arrival of a second heatwave across much of western Europe has exacerbated drought concerns. For winter crops, the second heatwave is unlikely to have caused much of a penalty on yield as most of the crop has passed its key grain fill stage. Instead, this is likely to have accelerated the crop towards harvest-ready condition. In contrast, the corn crop is showing signs of deterioration. In France, the corn crop has begun its pollination stages, a period when it is particularly sensitive to adverse conditions. With France usually being the largest corn-producing member state, a smaller crop would require more imports and push more wheat into feeding. This would reduce the wheat export surplus, which helps consume some of the excess in the Western EU wheat balance. It will also increase EU corn imports, as reflected in Kpler’s S&D balances.

French corn rated in good or excellent condition (%)

Source: FranceAgriMer

- The winter barley harvest in southern Russia has begun, with latest yield reports appearing positive. This has supported optimism that winter wheat yields will be greater y/y, and therefore less likely to see a repeat of last year where Russian exports had a softer start to the export campaign due to lower production in the south. As a result, Russian wheat FOB offers have begun to decline, now closer to $230/t, with EU and Ukrainian prices falling in sympathy.

Minor Bulks: Aluminium prices extend decline as supply risks ease

- Aluminium prices have extended their decline over the past week as the market continued to unwind the supply risk premium associated with disruptions in the Middle East Gulf. At the same time, expectations of a more hawkish US monetary policy have strengthened the US dollar, weighing on the broader industrial metals complex. Consequently, the three-month LME aluminium contract fell 1.47% w/w to $3,076/t on 1 July, its lowest level since February. Despite the recent correction, the global aluminium market remains undersupplied, suggesting that any renewed supply disruption could quickly reverse the current price weakness.

- Alcoa and South32 reached a binding conditional agreement under which Alcoa will acquire South32's aluminium supply chain interests, including its bauxite, alumina and aluminium assets in Brazil, South Africa and Western Australia. The transaction would substantially expand Alcoa's upstream footprint while helping South32 to facilitate a strategic shift towards higher-margin assets. South32 is expected to produce 5.11Mt of alumina and 1.10Mt of aluminium in FY2026 ending June, while Alcoa has guided for 9.70–9.90Mt of alumina and 2.40–2.60Mt of aluminium production in calendar 2026.

- Meanwhile, governments are increasingly seeking to retain secondary raw materials domestically. The European Union is reportedly considering a 15% levy on aluminium scrap exports, amid stronger demand for scrap following Middle East supply disruptions, which affected around 9% of global primary aluminium production. The proposal follows the UAE's temporary ban on exports of aluminium, copper and ferrous scrap, effective from 10 June, highlighting a broader global trend towards strengthening domestic recycling industries and improving resource security.

- Alumina prices have continued to weaken over the past week as oversupply remained the dominant market driver. The absence of any Guinean announcement on bauxite export restrictions in June further undermined sentiment. The most traded alumina contract on SHFE, September 2026, dropped 3% w/w to 2,786 yuan/t on 1 July.

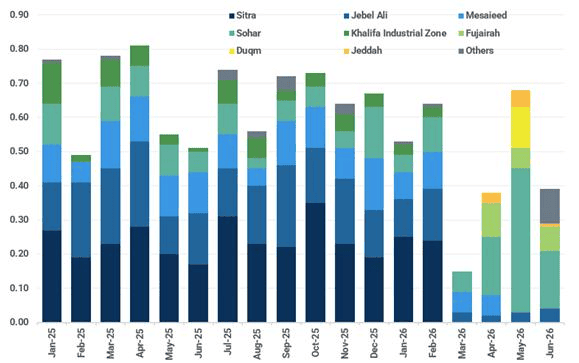

- Across the GCC, alumina imports continued to rely primarily on ports located outside the Strait of Hormuz, although shipping activity through the Strait has somewhat recovered. The Handysize Valsamitis became the latest alumina carrier to transit Hormuz via the Omani route on 27 June. Preliminary data indicate that GCC seaborne alumina imports totalled 0.39Mt in June, down from 0.67Mt in May, although final volumes may be revised upwards as additional cargoes are confirmed.

GCC alumina imports by destination ports (Mt)

Source: Kpler

- Since the resurgence of trade via the Strait of Hormuz saw most fertiliser-laden vessels exit the Strait, this has partially relieved the tighter global supply. However, the number of ballast ships seeking to load fertiliser in the Middle East Gulf (MEG) remains historically low due to concern of not being able to exit once loaded. Therefore, this could see a return of tighter global fertiliser supply as exports of sulphur and nitrogen fertiliser from the MEG account for approximately 50% and 25% of global seaborne trade, respectively.

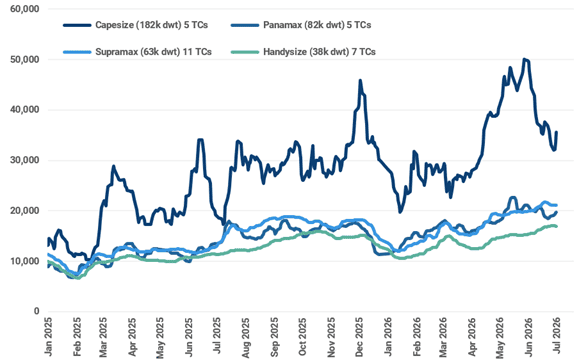

Dry Bulk Freight: Sentiment diverges as larger bulker markets firm but the geared vessel outlook remains weak

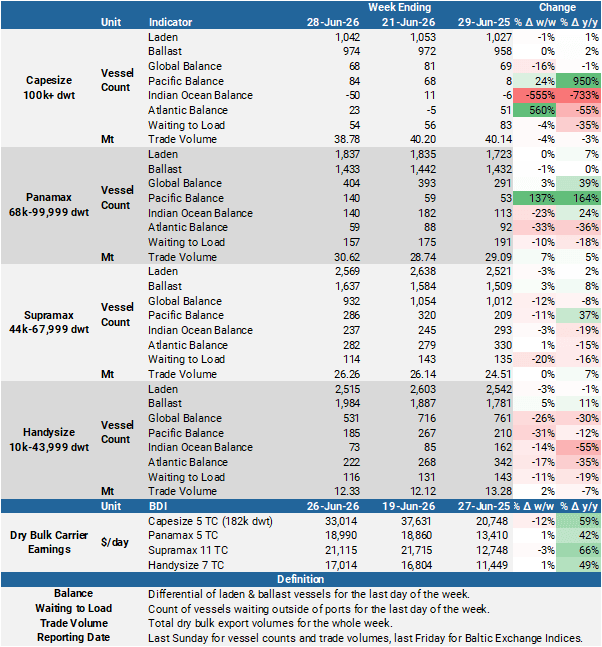

- Sentiment in the dry bulk freight market has diverged, with the outlook for Capesizes and Panamaxes more positive, while Supramaxes and Handysizes lag. This is reflected in the Freight Futures (FFA) market, where the Capesize (182k dwt) forward curve edged higher, but there has been a fall in the equivalent Supramax (63k dwt) forward pricing. Improving

- After starting the week softer, Capesize earnings found a floor and pushed higher in recent days. The bid/offer spread widened as owners adjust their expectations higher, suggesting expectation of further gains to come. The higher Atlantic market is attracting more vessels, leading to a rise in ballasters in the Indian Ocean heading west. This has, in turn, helped to halt the downturn in the Pacific. From a three-month low of $25,314/day on 29 June, the Pacific round-voyage rate climbed to $31,713/day on 2 July. The number of ballasting Capes in the Pacific has stabilised in line with the five-year average. The higher Pacific market was the driver of a $855/day w/w increase in the 5 TC average to $35,563/day.

- Gains across the board lifted average Panamax earnings by $893/day w/w to $19,758/day. High numbers of vessels in the Pacific, both the laden and ballast count are more than 100 ships above the five-year average, is capping the upside for Panamax earnings in the basin. The round-voyage rate is at a discount of almost $6,000/day to the Pacific. Reports suggesting that owners are favouring short-term business in the Pacific imply optimism about the earnings for the basin. Any firming in regional demand will need to be supported by the Pacific coal trade.

- This support has yet to be forthcoming. The Panamax P5 (South China-Indonesia round-voyage) was flat w/w, and the Supramax S8 (Indonesia-East Coast India) and S10 (South China-Indonesia round-voyage) routes dropped by $1,568/day and $1,062/day to $21,843/day and $14,094/day, respectively. Pacific market weakness wiped out US Gulf-focused gains in the Atlantic to leave the Supramax 11 TCs slightly lower w/w at $21,168/day. With an implied Supramax Atlantic round-voyage rate (average of S4A and S4B) higher than the Panamax equivalent and the number of Supramax ballasters in the Atlantic increasing, US Gulf earnings may struggle to maintain upward momentum.

- The Atlantic Handysize market continues to look overtonnaged. Ballasting vessels gather in the East Med and Black Sea, but we have yet to see a matching increase in demand from the region. With demand in the South Atlantic following the expected seasonal pattern and starting to slow, regional earnings are likely to come under pressure. A softening in the 7 TC average, almost unchanged w/w at $16,990/day, is likely.

- Dry bulk carrier transits through the Strait of Hormuz have slowed sharply from the high of 25 transits on 24 June and are expected to remain lower in the short term. Transits averaged nine per day in the week to 1 July. Fresh attacks on shipping in the region and the failure to secure any agreement as to the status of the Strait once the 60-day MOU expires are making owners reluctant to take their vessels into the region. The number of dry bulk carriers in the Middle East Gulf has now dropped below 140 ships, lower than the typical number before the war.

Average dry bulk carrier earnings: Capes and Panamaxes higher w/w, while geared markets struggle ($/day)

Source: Baltic Exchange

Key Dry Bulk Market Developments

Dry Bulk Commodity Flows

Source: Kpler

Dry Bulk Port Congestion

Source: Kpler

Dry Bulk Freight Metrics

Source: Kpler, Baltic Exchange

See why the most successful traders and shipping experts use Kpler