Dubai still searching for a bottom as Hormuz flows recover

The Dubai market is collapsing, with Middle Eastern crude differentials falling to levels not seen in years as oversupply fears overwhelm the market. But has the market found a floor, or is the worst still ahead?

Key takeaway:

- Backlog clearance for crude stranded in the Persian Gulf has accelerated since the signing of the MoU, leaving only around 23 mb yet to transit the Strait of Hormuz. The remaining backlog is expected to be cleared within the next one to two weeks.

- New loadings from the Persian Gulf also picked up in June and are likely to accelerate further as producers ramp up output and shipowners regain confidence in transiting the Strait of Hormuz.

- An uncertain supply outlook, the collapse in West of Suez crude prices and still-subdued Chinese demand have combined to drive the Dubai market into a sharp sell-off.

- A shift in Asian buying from Atlantic Basin crude toward Middle Eastern barrels may lend some support to Dubai market, but is unlikely to be sufficient to reverse the weakness in the forward curve and crude differentials.

Since the outbreak of the war in late February, it has been difficult to pinpoint the fair value of Middle Eastern crude. The availability of supply has become less a function of producers' output than of geopolitical developments and market participants' risk appetite amid the disruption to Strait of Hormuz traffic.

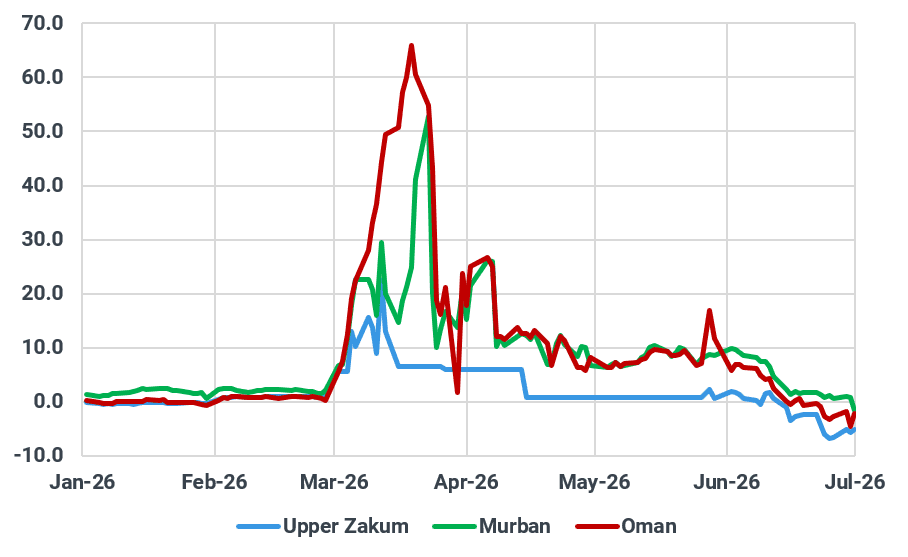

Benchmark Dubai prices soared to as high as $167.6/bbl in mid-March, according to Argus data, fueled by fears of supply disruptions. Just three months later, they plunged to as low as $65.9/bbl as the market swung to the opposite extreme—concerns over oversupply.

Selected Middle Eastern crude diffs vs Dubai, $/bbl

Source: Argus Media

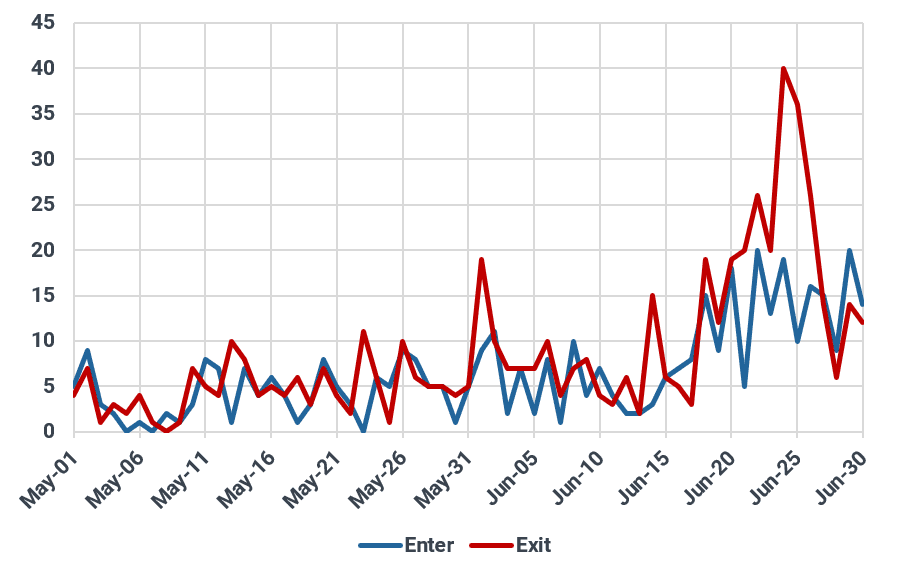

Vessel traffic through the Strait of Hormuz has increased sharply since the US and Iran signed an interim peace agreement on 17 June. Daily transits briefly peaked at 61 before stabilizing at around 30, still more than double the fewer than a dozen vessels recorded prior to the MoU. As previously forecast, laden tankers stranded in the Persian Gulf were among the first to leave the region, accounting for a significant share of oil flows through the Strait of Hormuz during the initial phase of its reopening.

A rough calculation based on Kpler data shows that around 52 mb of non-Iranian crude loaded in the Persian Gulf between 27 February and 31 March transited the Strait of Hormuz in June, on top of the 43 mb that exited the Gulf between March and May. That said, around 23 mb of stranded cargoes remained inside the Persian Gulf at the end of June. As tanker traffic appears to have remained largely unaffected by the back-and-forth rhetoric and brief military exchanges between Tehran and Washington, the remaining backlog is expected to be cleared over the next one to two weeks.

Although many mainstream shipowners remain wary of the geopolitical situation and insurance premiums remain elevated, the number of vessels entering the Strait has recently matched or even exceeded outbound traffic, suggesting that a pickup in new cargo loadings is underway.

Vessels crossing the SoH by direction, count

Source: Kpler

Last month, around 2.6 mbd of June-loading non-Iranian Middle Eastern crude exited the strait, including 1.6 mbd of UAE-origin cargoes, 360 kbd from Iraq, 400 kbd from Kuwait, 233 kbd from Qatar and 67 kbd from Saudi Arabia. In addition, 1.8 mbd was loaded from the Gulf of Oman after conducting STS operations with tankers carrying crude from the Persian Gulf in a less visible manner, making it difficult to determine where the cargoes were originally loaded.

It remains to be seen, however, whether new loadings can accelerate sufficiently to compensate for the fading contribution from backlog clearance and sustain current oil flows.

Yet, the Dubai market is trading at levels as if a full restoration of flows through the Strait of Hormuz were just around the corner. Part of the reason may be that oil producers have accelerated the issuance of spot tenders, offering prompt-loading cargoes on a large scale while also placing volumes through private negotiations. As a result, market participants have limited visibility into the number of cargoes scheduled for loading over the next two months, making it difficult to accurately assess the supply outlook.

In the meantime, rising Middle Eastern supply, largely saturated demand across Asia (excluding China), and the sharp decline in Dubai prices have encouraged traders to redirect cargoes to the West of Suez market, weighing on the Dated Brent benchmark and depressing differentials for Atlantic Basin crude. The resulting cargo overhang and aggressive offers have created a buyers' market, forcing Dubai prices even lower to remain competitive.

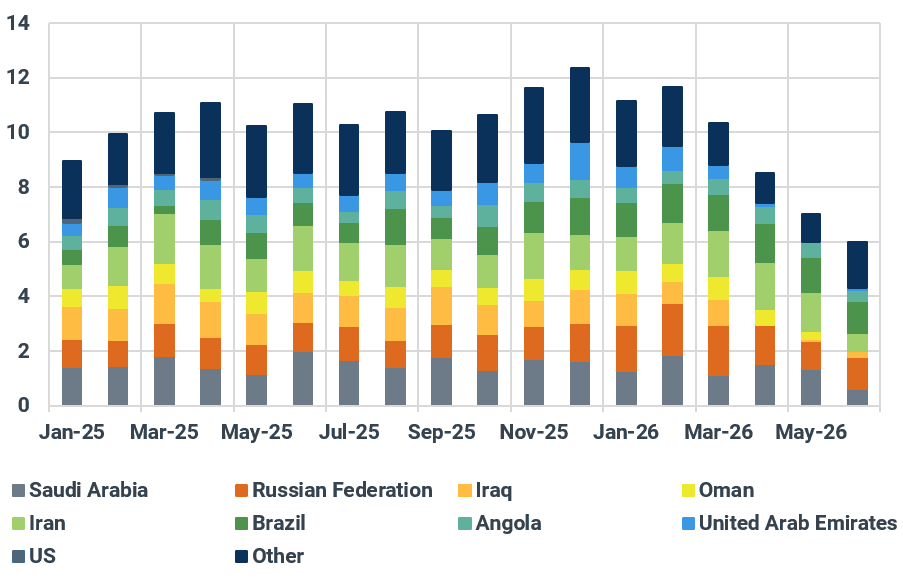

Another key factor shaping the market in recent months has been China's buying behaviour. The country imported just 6 mbd of seaborne crude in June, around 4 mbd below its 2025 average. Whether and how quickly that missing demand returns could ultimately determine whether the global crude market remains oversupplied or swings back into balance. While Chinese state-owned refiners continue to refrain from placing sizeable orders, independent refiners, which have traditionally relied on Iranian and Russian feedstock, are actively purchasing spot Middle Eastern grades such as Al Shaheen, Upper Zakum and Basrah, attracted by their competitive pricing.

At the time of writing, these grades are trading at discounts of around $1–2/bbl to Iranian crude on a delivered basis into China, according to market participants.

China's seaborne crude imports (including via Myanmar) by origin, mbd

Source: Kpler

However, these purchases are more likely to represent opportunistic buying than a strategic shift in feedstock sourcing, as Iranian sellers are expected to lower their offers to remain in line with the broader market, particularly given that the current US sanctions waiver has generated only limited buying interest outside China.

Therefore, unless Chinese crude demand sees a meaningful recovery, the Dubai forward curve is expected to remain in minor contango, while Middle Eastern crude differentials are likely to stay in discount territory, provided the situation in the Strait of Hormuz does not deteriorate.

That said, the July trading cycle may prove more resilient than the weakness seen in late June, as many Asian refiners still need to secure September- and October-arrival cargoes after largely staying on the sidelines in the Atlantic Basin crude market over the past two weeks, lending some support to Dubai-linked crude grades. Yet with producers keen to maximize exports and shipowners gradually regaining confidence in transiting the Strait of Hormuz, there is still considerable upside to Middle Eastern supply, suggesting the Dubai market may have yet to find a bottom.

See why the most successful traders and shipping experts use Kpler