Hormuz shock reprices crude but storage constraints force a fast resolution

The US-Iran war has sharply repriced crude differentials across regions and qualities, but storage limits, elevated inventories and shifting arbitrage flows are containing the broader price response.

Market & Trading calls

Heavy crude differentials: Bullish as demand for heavier barrels is set to remain robust amid Middle Eastern outages, with steadily rising US crude demand, and Alberta's spring field maintenance keeping Americas heavy sour crude markets tighter.

Medium crude differentials: Bullish across regions as refiners seek alternative supplies to cover prompt requirements and anticipated restocking demand.

Light crude differentials: Bullish for light crude in the EoS and WoS as the US-Israel-Iran war squeezes deliveries out of the MEG, leaving buyers to scramble for supply.

Price forecast:

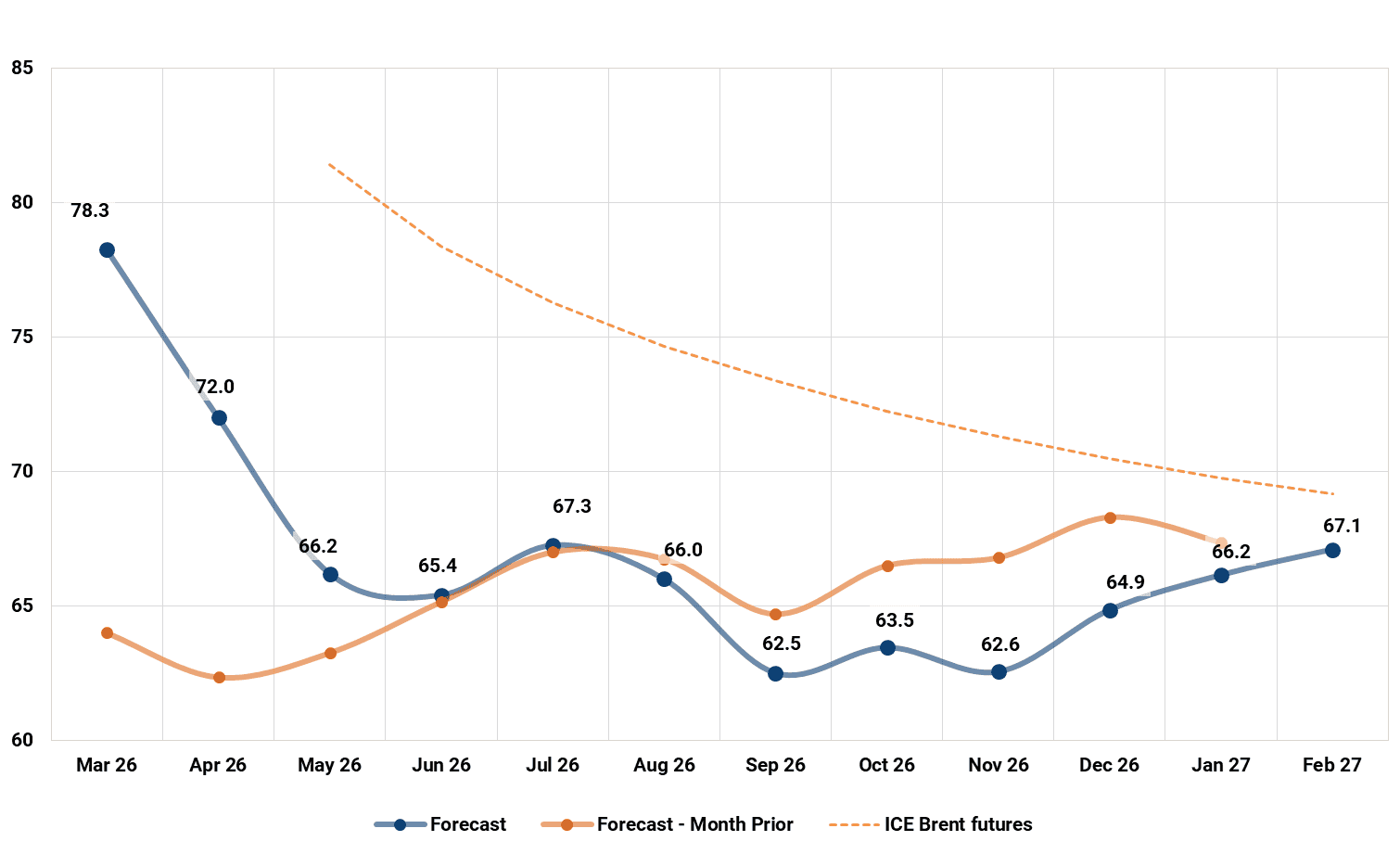

North Sea Dated averaged $71/bbl in Feb., $4.5/bbl above our forecast, as geopolitical tensions tightened market structure. Front-month Dated traded in a narrow $69–72/bbl range before breaking higher after the US and Israel formally entered into conflict with Iran. The escalation prompted us to revise our near-term outlook upward, especially for the near-term. Our updated 12-month forecast for NSD is $66.8/bbl, up from $65.7/bbl previously.

Flat prices have risen ~13% since the outbreak of war, broadly in line with our expected magnitude of reaction. The move has been relatively contained, reflecting a risk premium that had already built through Jan.–Feb., approaching $20/bbl in our model versus a normal baseline. Elevated Chinese inventories and high crude-on-water levels, particularly in Asia-Pacific, have also dampened panic buying.

Our base case assumes the conflict remains contained and relatively short-lived. The US-Israel coalition military superiority, Iran’s finite missile capacity, and the strategic importance of the Strait of Hormuz for global energy flows reduce the likelihood of prolonged disruption. With the US offering military support and insurance to the maritime industry, transit will gradually normalise starting from the end of this week. Prices will see the bulk of the risk premium fade as clarity emerges that the war is nearing its end, potentially by late March or mid-April at the latest. Symbolically, the US and Israel may also be looking to end the war by Nowruz, the Iranian New Year, on 21st March.

Prices should ease from current levels once tensions subside, though volatility will remain elevated through March. Seasonal refinery demand, healthy margins, and residual uncertainty around Iran’s political transition should provide a floor into Q2. OPEC+ supply hikes are unlikely to weigh materially before September due to rising domestic demand. However, we turn more bearish in H2, as higher OPEC+ output and resilient US supply, supported by producer hedging, loosen balances.

Nevertheless, risks this month are skewed to the upside in the short term. A deeper escalation, such as sustained disruption in the Strait of Hormuz or direct targeting of regional energy infrastructure, could push prices above $100/bbl, with extreme scenarios reaching $150/bbl if transit remains blocked for more than four weeks. Conversely, a rapid political agreement between Washington and Tehran would likely compress the risk premium quickly, potentially driving Brent back under $60/bbl.

North Sea Dated Price Forecast, $/bbl

Source: Kpler, ICE

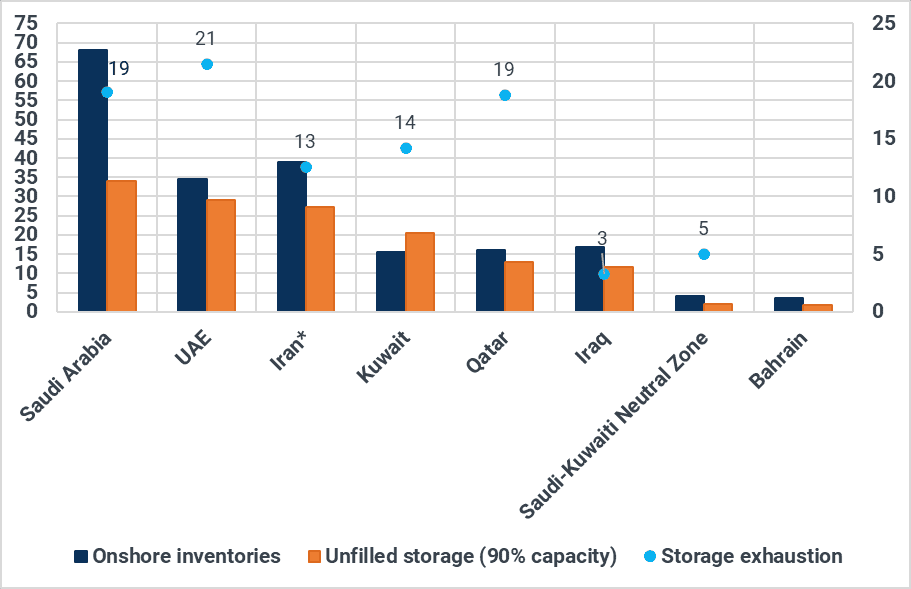

Chart of the Month: Export coverage (days) reveals Iraq’s acute exposure

The effective closure of the Strait of Hormuz is unevenly impacting Mideast Gulf countries. While Saudi Arabia, the UAE and Iran retain partial bypass options, Iraq, Kuwait, Qatar and Bahrain do not. Aramco can technically export up to 5.1 Mbd via Yanbu on the Red Sea (with total capacity of 7 Mbd), and ADNOC can ship 1.5–1.8 Mbd from Fujairah. Iran can utilise Jask, although its own tankers continue limited passage through the Strait.

By contrast, Iraq, Kuwait, Qatar, and Bahrain lack bypass capacity. Iraq is the most exposed. Around 94% of its 4.2 Mbd of crude output originates from the south and cannot be redirected north to Ceyhan, aside from negligible trucking volumes (~40 kbd at best).

Kpler satellite revisits from 28 Feb.–2 Mar. (UTC) indicate roughly 8.7 Mb of conservative working headroom remaining across five key southern installations feeding the Basrah export chain. Applying a 90% working-capacity ceiling and assuming net builds of ~2,900 kbd (based on 3,300 kbd inflows minus ~400 kbd domestic draws) implies less than three days before storage saturation if tanker access remains constrained. This explains why Iraq was the first to implement shut-ins, with partial curtailments reported at Rumaila and West Qurna 2, which together produce 1.6 Mbd.

Other regional producers would likely be forced into cuts within two to three weeks. Even Saudi Arabia and the UAE, which are able to partly bypass the Strait, would approach storage limits within roughly three weeks, excluding underground capacity not captured in our model.

Meanwhile, ballast vessel availability in the Mideast Gulf has fallen sharply, from an average of 55 in Jan.–Feb. to 37 currently, limiting rapid export normalisation. Taken together, these storage dynamics reinforce our view that a reopening of transit routes is more likely to materialise within days rather than weeks, as sustained closure would rapidly force widespread production shut-ins.

Mideast Gulf countries oil storage (mbbls, LHS) and storage exhaution (days, RHS)

Source: Kpler. Iran will likely continue to load and export crude as normal even if the Strait of Hormuz remains effectively closed although the lower number of Chinese vessels will impact its loadings too.

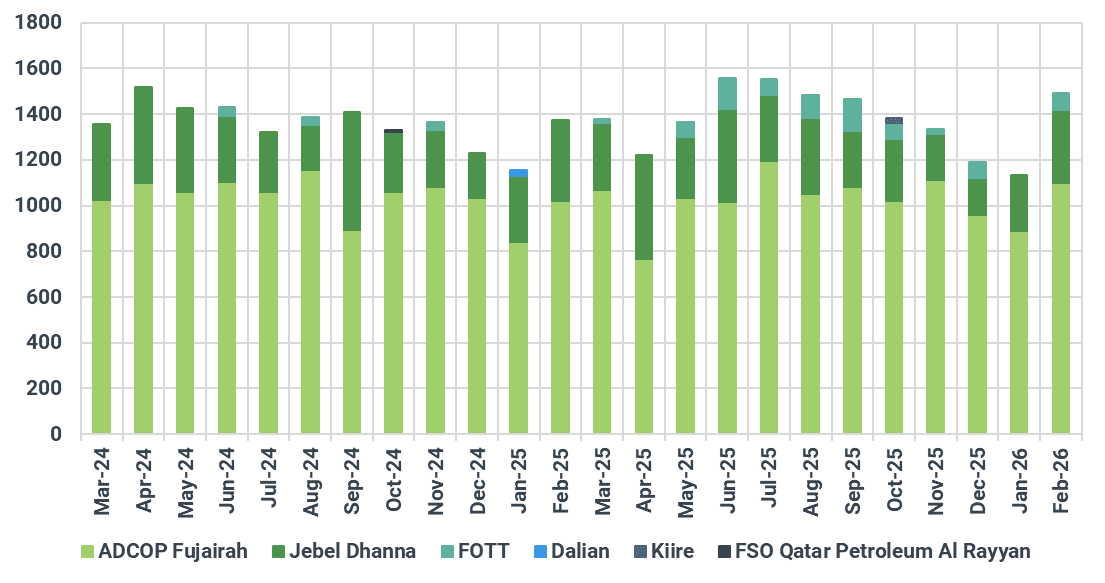

Light crude: Light sour Murban amongst the first grades in the light complex to benefit from US-Israel-Iran war

Light sour Murban differentials surge to multi-year highs, with strength likely to persist near term

Escalating tensions in the Middle East have significantly boosted Murban crude differentials. A major supportive factor is that most Murban exports are shipped via ADNOC’s ADCOP terminal in Fujairah, which bypasses the Strait of Hormuz and enables direct loadings into the Gulf of Oman. The ADCOP pipeline links the Habshan onshore pumping station in Abu Dhabi to Fujairah and has a nameplate capacity of 1.5mn b/d, with potential for a modest short-term uplift through operational optimisation. We estimate current utilisation at roughly two-thirds of capacity. In early March, Murban futures surged to a $6.70/bl premium to May Dubai swaps — the widest since November 2022 (Argus Media). With Murban now trading at elevated premiums, Asian refiners may increasingly turn to alternative light sweet grades such as US WTI, potentially diverting barrels from Europe and lifting WTI differentials. This would, in turn, tighten the European light sweet market — including North Sea and Mediterranean grades — given that around 15% of Europe’s crude imports are sourced from US WTI. A shift in flows could also open eastbound arbitrage opportunities for Atlantic Basin crudes, supporting differentials for grades such as CPC Blend, BTC Blend, Forties and Johan Sverdrup. Beyond geopolitical risk, Murban prices may find additional support from tighter supply. After exports rebounded to 1.49 Mbd in February (from 1.35 Mbd in January), ADNOC has reduced its May export forecast to 1.46 Mbd due to scheduled maintenance, pointing to more constrained availability in the near term.

Murban crude exports, kbd

Source: Kpler

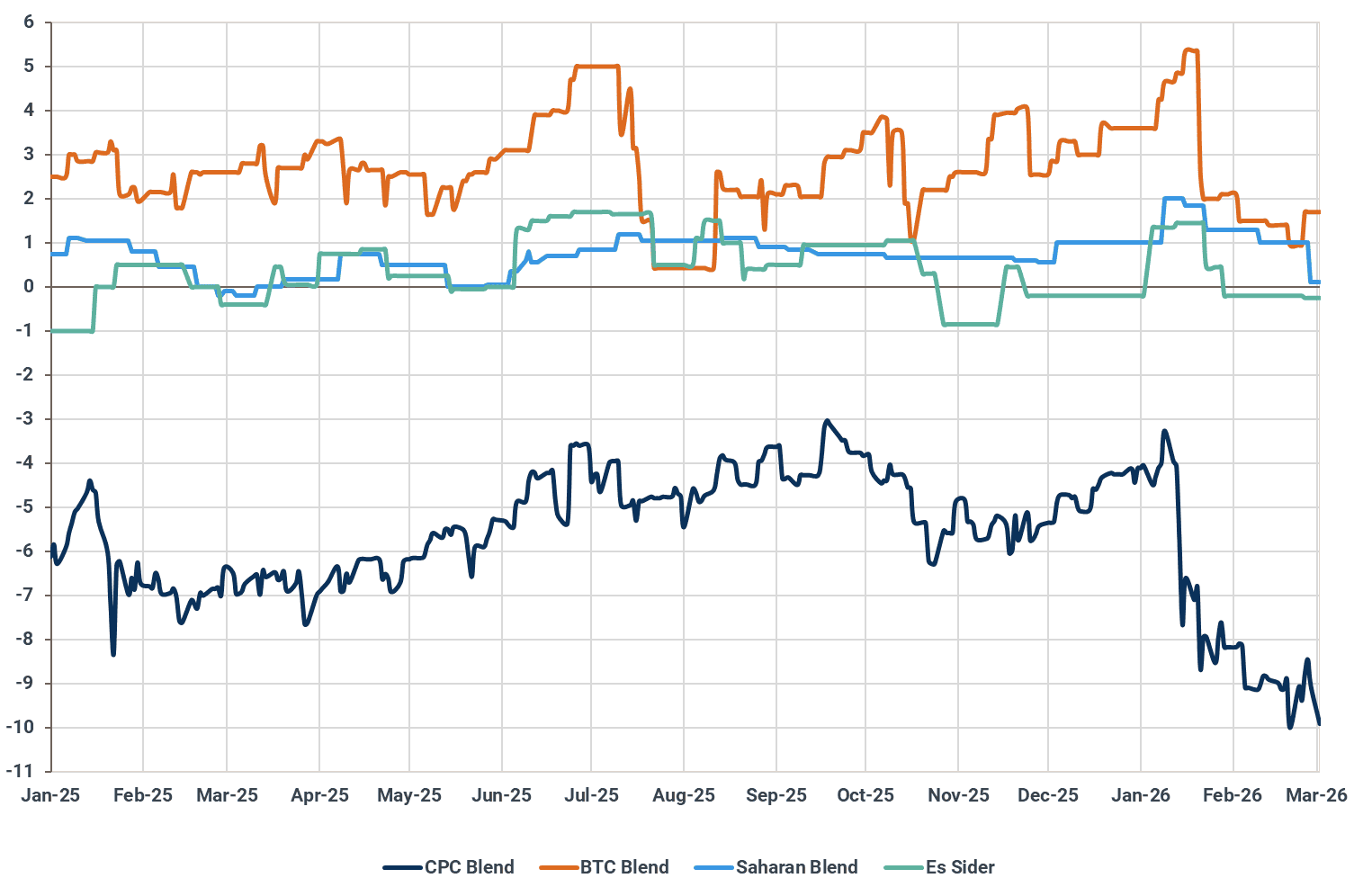

Drone strike at Novorossiysk unlikely to disrupt CPC terminal, but uncertainty pressures CPC Blend differentials

Following severe disruptions in January — when crude exports from the CPC terminal dropped to 850 kbd — loadings have faced renewed pressure. Weather-related delays over the past week slowed crude arrivals through the CPC system and disrupted scheduled liftings. Exports recovered to around 1 Mbd in February, but this remains well below the roughly 1.5 Mbd average seen in H2 2025. Kpler data show weekly loadings fell sharply in late February, contributing to a build in CPC terminal inventories to multi-year highs above 4 Mbbls. The most recent departures from the terminal were the Kazakh CPC-laden Suezmaxes Llevant, Seagrace and Delta Ios on 27 February. A Ukrainian drone attack on 2 March targeting the Sheskharis oil terminal briefly raised concerns over potential disruptions to Black Sea exports. Despite the lack of physical disruption, heightened buyer uncertainty has weighed on sentiment. The CPC Blend discount to North Sea Dated widened to around -$10/bbl in late February — the weakest level in nearly three years. However, elevated inventories at the CPC terminal could eventually curb upstream flows, providing some support to prices. In addition, improving eastbound arbitrage economics may soon lend support to CPC Blend differentials (see above).

Med light crude differentials, $/bbl

Source: Argus Media

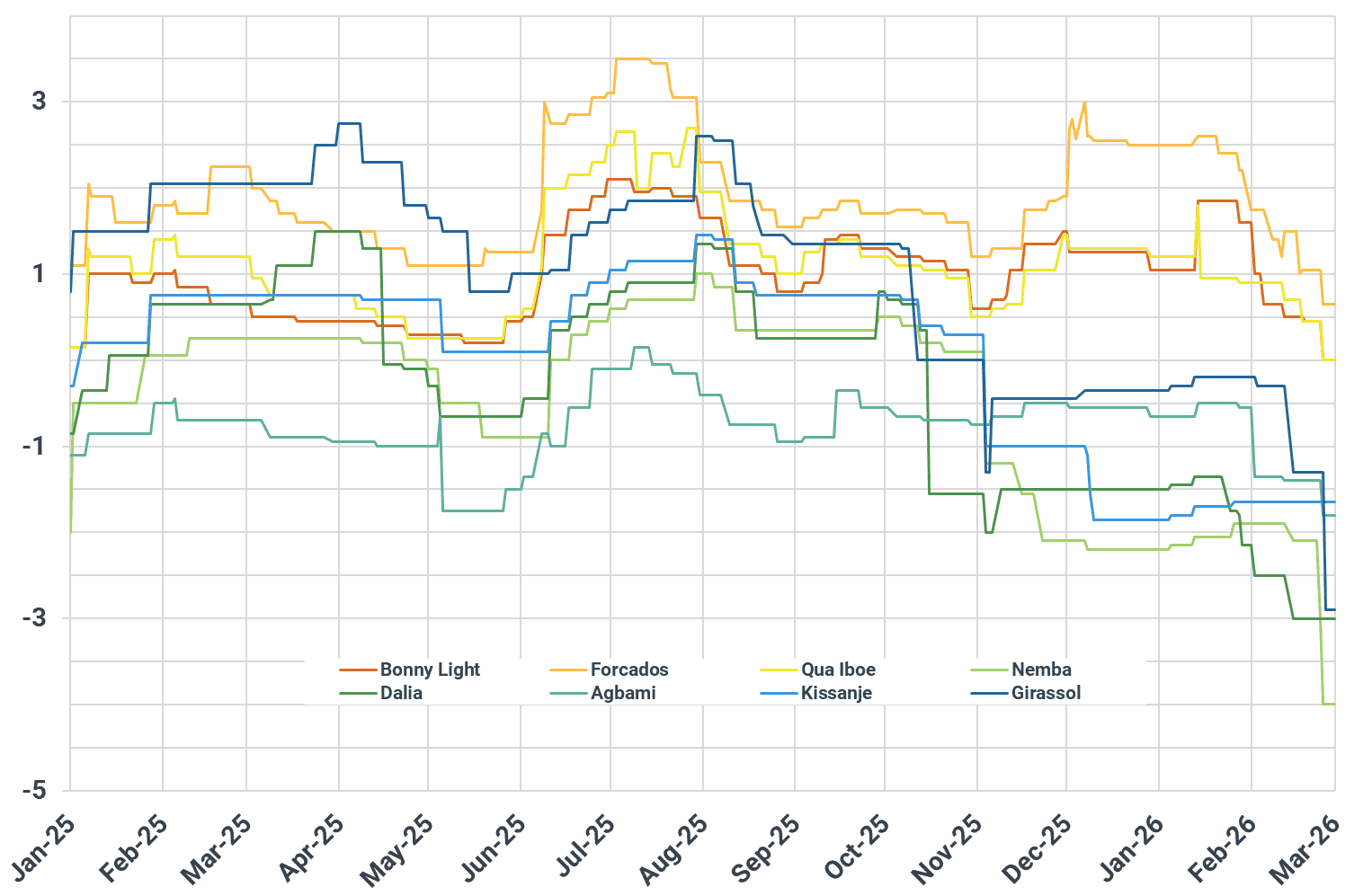

Nigerian crude valuations fall to one-year lows, but recovery signs emerging

West African crude differentials have declined sharply over the past month. Between early February and early March, Forcados and Bonny Light differentials to Dated Brent fell by $1.00–1.60/bbl (Argus Media), pushing valuations to their lowest levels in roughly a year. The weakness reflects softer European demand for light and medium Nigerian grades. EU refineries are entering spring maintenance, further curbing intake. Our supply-demand balances indicate EU-27 crude demand slipping below 9 Mbd in March — around 500 kbd lower m/m. At the same time, ample supply from CPC Blend, US WTI and Libyan grades has kept the Atlantic Basin well supplied. Additional pressure stems from Nigeria introducing a new stream, Cawthorne crude, in March, increasing regional availability. Higher freight rates have also weighed on fob differentials. In response to weaker spot markets, NNPC reduced most March official selling prices (OSPs), cutting the majority of grades by $0.30–0.50/bbl. Qua Iboe saw a larger $0.70/bbl reduction, while Forcados and Escravos were lowered by $0.33/bbl and $0.59/bbl respectively (Argus Media). Looking ahead, some recovery appears likely. Nigerian and Angolan differentials could find support from East-of-Suez refiners seeking alternative light sweet barrels amid disruptions linked to the US–Israel–Iran tensions. In addition, domestic demand for Nigerian crude is set to strengthen, with a sharp rebound in Dangote refinery runs. We estimate intake rising to around 470 kbd this month, up from roughly 350 kbd in February, following the restart of the CDU on 11 February and the RFCC about a week later (IIR).

West African crude differentials, $/bbl

Source: Argus Media

Medium crude: Mideast supply disruptions push buyers toward alternatives

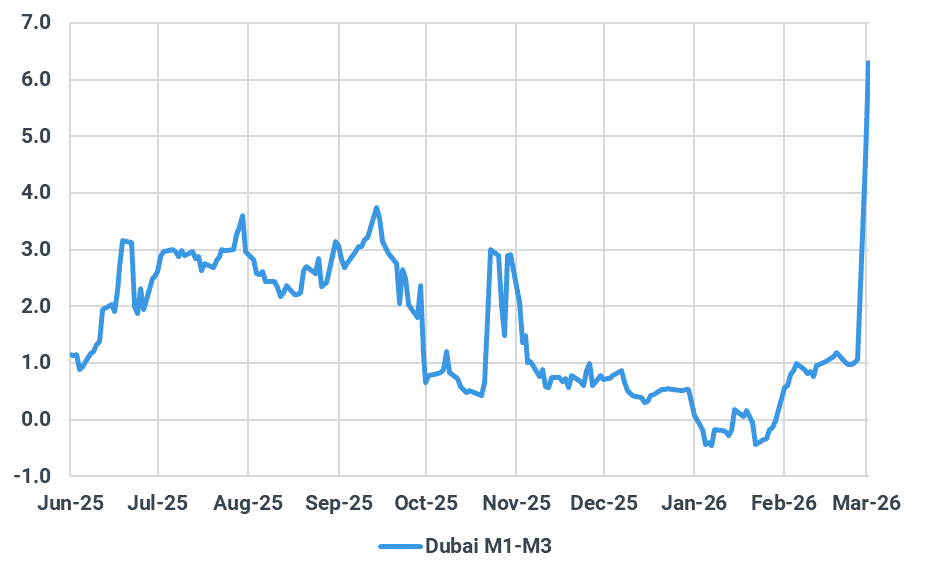

De facto SoH closure triggers sharp rally in Dubai market

Dubai-linked medium sour crude prices have surged over the first two trading days of March, as intensified Iranian strikes on regional energy infrastructure and the de facto closure of the Strait of Hormuz stoked concerns over supply availability. The spread between the prompt and third-month Dubai contracts widened to $6.3/bbl — the strongest level since July 2022, according to Argus Media. This compares with an average of $0.9/bbl in February and -$0.2/bbl in January.

That said, even as Asian refining demand is set to soften with the onset of the spring maintenance season and OPEC+ moves ahead with its planned production quota increase in April, Middle Eastern NOCs may still raise their April OSPs more aggressively than the current Dubai structure would imply.

As the de facto closure of the strait persists, refiners reliant on Middle Eastern crude will be forced to draw down inventories, setting the stage for restocking demand once flows normalize. This dynamic has provided a strong catalyst for physical differentials for the May-loading cargoes. Oman’s premium surged to $5.7/bbl against Dubai swaps — its highest level since October 2022 — while Upper Zakum also climbed to a multi-year high, despite the fact that its cargoes must still transit the Strait of Hormuz to reach the market.

While it remains unclear when tensions in the Middle East will ease and traffic through the Strait resume, Iran’s increasingly aggressive strikes suggest that Middle Eastern crude prices are likely to remain elevated for at least one to two weeks — if not longer — before undergoing a sharp correction.

Dubai M1-M3 spread, $/bbl

Source: Argus Media

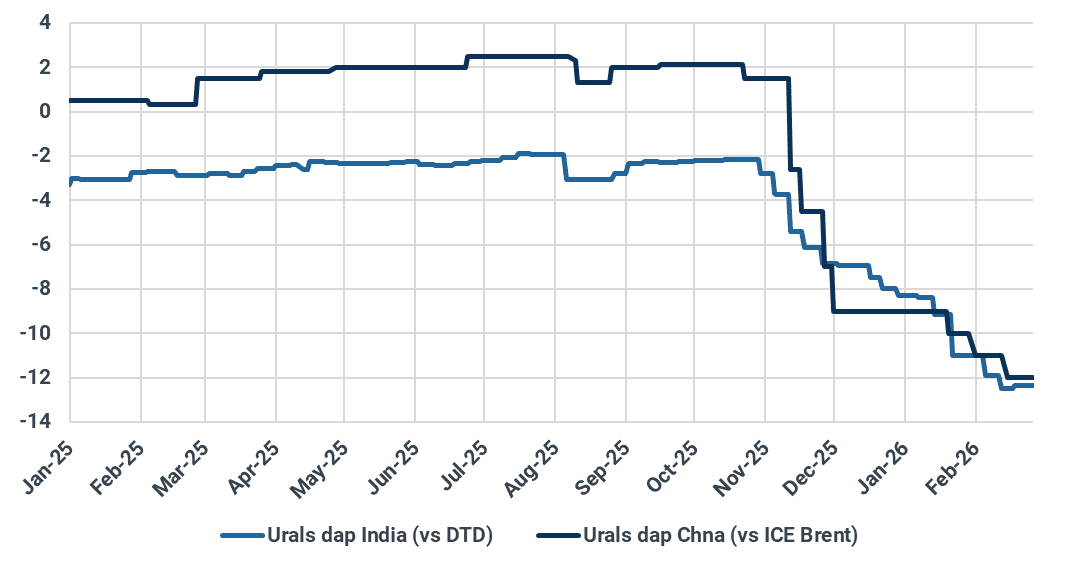

Russian Urals prices gain momentum on renewed Indian demand

Russia’s medium sour Urals crude is poised for a strong rebound after falling to its lowest level in India since April 2023 and potentially to a record low in China in February. As Middle Eastern supplies appear increasingly vulnerable, with vessels reluctant to transit the Strait of Hormuz, Indian refiners have begun seeking prompt Urals cargoes to meet near-term demand. India currently holds around 102 mb of onshore crude inventories — equivalent to roughly 20 days of its total imports and about 45 days of its Middle Eastern crude intake.

The renewed buying interest are expected to lift Urals prices from -$12.35/bbl against Dated Brent last week, according to Argus Media. At the same time, offers into China already firmed to -$8.5 to -$10/bbl against ICE Brent, up from around -$12/bbl previously, market participants told Kpler.

While India’s incremental demand for Russian crude is likely to be short-lived — driven primarily by the Middle Eastern supply shock — it will nonetheless help clear the sizable volumes of Russian crude currently on the water and ease downward pressure on pricing, even after the war subsides.

That said, Russian barrels could gain even stronger upward momentum if Washington were to allow Iranian crude to return to the mainstream commercial market in the aftermath of the war, similar to the Venezuelan precedent. In such a scenario, Chinese teapots would have few viable alternatives to Iranian crude other than Russian barrels.

Urals diffs in India and China, $/bbl

Source: Argus Media

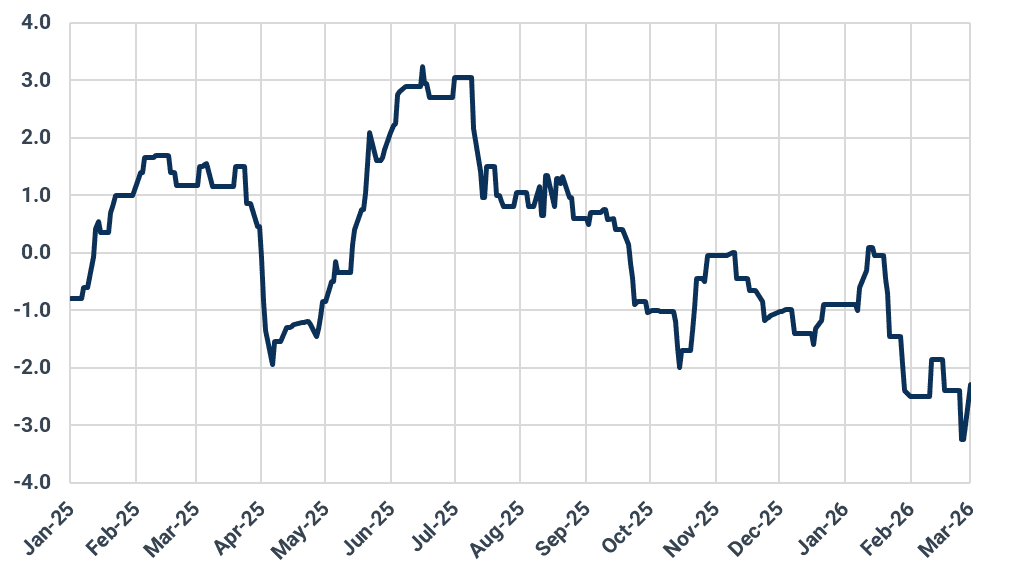

Expected drop in westbound Middle Eastern flows lift Johan Sverdrup prices

European medium sour grades are also poised to rebound from multi-month lows in response to the latest US–Iran conflict. Norway’s Johan Sverdrup differential strengthened to -$2.3/bbl against Dated Brent on an FOB Mongstad basis on Monday, up from a near two-year low of -$3.25/bbl in late February, according to Argus Media data. Grane differentials are likewise expected to firm in the coming days after slipping to a three-month low of -$2.5/bbl last week, when BP failed to secure a buyer for a March-loading cargo it had offered.

The effective closure of the Strait of Hormuz has disrupted crude exports from the Middle East Gulf and forced some Iraqi oilfields — including Rumaila and West Qurna — to curb output due to limited storage capacity. As a result, European refiners are likely to see sharply reduced, if not virtually halted, Middle Eastern crude arrivals in April.

At the same time, rising freight rates have enhanced the competitiveness of European grades relative to Latin American supplies, drawing stronger buying interest from regional refiners. On a delivered basis into Europe, Johan Sverdrup is currently estimated to be around $2/bbl cheaper than Guyanese Liza.

That said, the sharp rally in European middle distillate cracks, coupled with the gradual easing of spring refinery maintenance in the region, is set to lend further support to medium sour crude across the broader Atlantic Basin in the near term.

Johan Sverdrup diffs against Dated Brent on the FOB basis, $/bbl

Source: Argus Media

Heavy crude: Middle East outages bolster Americas heavy sour complex

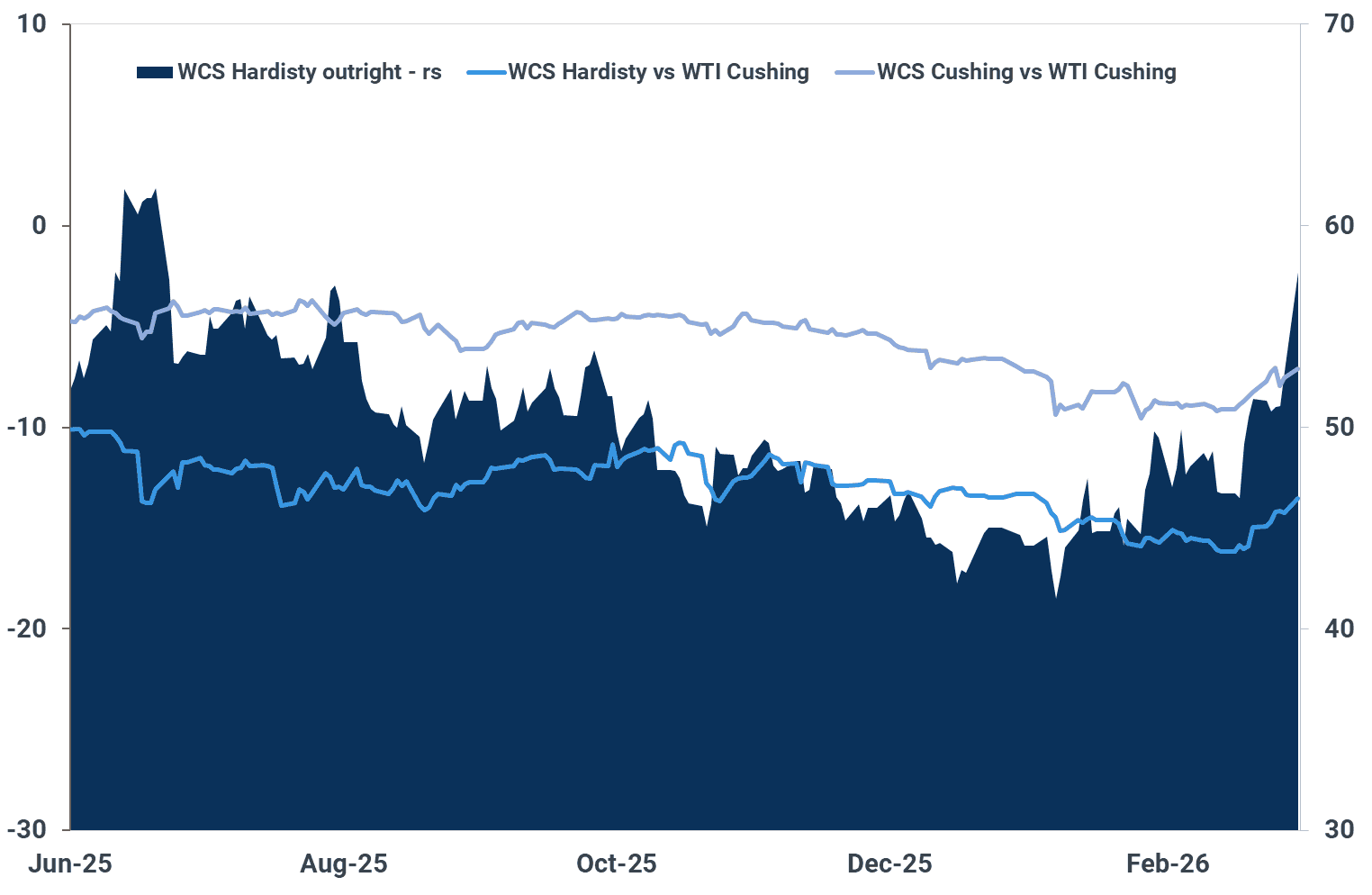

WCS Hardisty to find fresh support as tailwinds align

The closure of the Strait of Hormuz—paired with escalating operational disruptions across the Gulf— along with Iraq recently cutting output from important fields, including West Qurna and Rumaila, is set to abruptly tighten Atlantic Basin sour availability and inject a fresh geopolitical premium into Americas heavy sour crudes.

If Middle East medium sours are curtailed, complex US Gulf refiners—optimized for sour feed—typically bid up alternative medium and heavy sours; WCS is heavier than Saudi grades, but it can still backfill sour needs and support coker utilization, lifting its relative value. Saudi Arabia exported ~300 kbd to the US Gulf over the last two months, the highest level since August 2022, with 90% of these volumes departing from Ras Tanura.

Rising product cracks are adding a second tailwind, improving heavy-sour netbacks and keeping complex refiners incentivized to maximize runs, with middle distillate cracks (jet cracks surpassed $40/bbl this week) now hovering at multi-month highs.

Against this backdrop, our base case expects US crude intake to rise from April onwards (+200 kbd month-on-month to 16.3 Mbd), building through spring and into peak summer demand, which will keep demand for heavier grades supported. At the same time, spring field maintenance across Alberta’s oil sands should tighten regional supply and reduce pipeline flexibility.

The combination—stronger refinery pull, a supportive sour-barrel complex, and seasonally constrained Canadian output—tilts risks toward stronger WCS Hardisty differentials (a narrower discount) into late spring, with the heavy sour benchmark currently hovering at multi-month highs of -$13.50/bbl versus WTI. A near-term retest of levels below $12/bbl is likely in the weeks ahead.

While a prolonged closure of the Strait of Hormuz could provide additional support amid a stronger pull from Asia for Canadian heavy sour barrels via the Westridge terminal in Vancouver, elevated freight rates and a recent increase in flat prices are likely to keep a partial lid on overall demand, particularly from China, where inventories remain elevated and at record highs.

WCS Hardisty crude differentials, $/bbl

Source: Argus Media

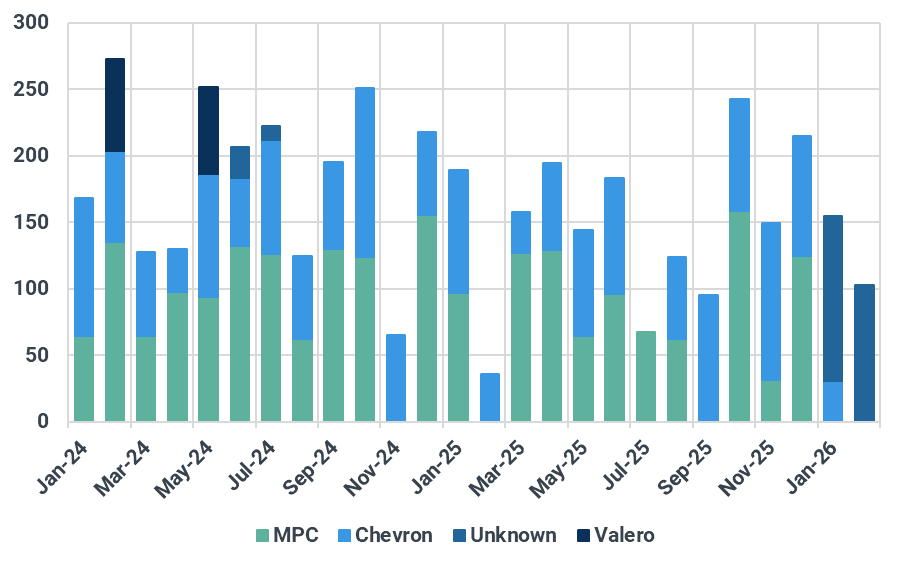

Iraqi disruptions could lift Napo demand in PADD 5

A Strait of Hormuz closure—and any resulting outages—would likely force PADD 5 refiners to adjust their average crude slate slightly, given that Iraq typically exports roughly 200 kbd to the US West Coast each month. Iraqi disruptions would also support WCS Hardisty differentials, especially if West Coast refiners increase imports via the Westridge terminal on Canada’s West Coast. Historically, PADD 5 refiners have leaned heavily on Napo at times when Middle Eastern barrels have been constrained.

Napo volumes into US West Coast refineries have slipped to around 30 kbd in recent months, with all of those barrels going to Chevron’s El Segundo. By contrast, Marathon Los Angeles and Chevron Richmond each import roughly 70-80 kbd of Basrah Medium. If Iraqi flows come under pressure—either through shut-ins or as a direct consequence of a Strait of Hormuz closure—these refiners are likely to partially turn to Napo to fill the gap, alongside medium sour grades from Latin America, including Guyanese and Brazilian crudes.

This would keep Napo pricing supported: the grade is trading at steeper discounts and can serve as an alternative feedstock despite its relatively heavy API gravity. Moreover, lower crude availability across Asia could also lift exports to the continent, with around half (70-80 kbd) of the grades total exports typically going to Asian refiners, primarily China, with smaller volumes (20-30 kbd) often departing to Japan.

Iraqi crude exports to PADD 5 by buyer, kbd

Source: Kpler

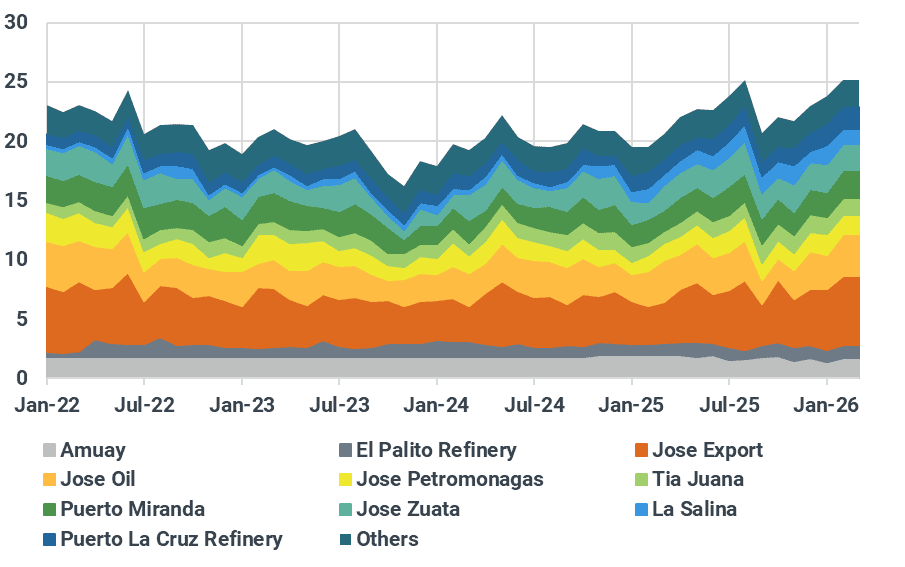

Record Venezuelan stocks cap Merey's upside

The Middle East supply risk is raising the value of dependable heavy sour alternatives. With US policy shifts delivered via OFAC general licenses and waivers, Venezuelan barrels have regained access to a wider pool of buyers in Europe, India, and the US.

As uncertainty around Middle Eastern flows remains high, we expect more European refiners to keep Venezuelan heavy sour grades in their slate to maintain heavier feedstock cover, especially if regional inflows into Europe tighten. 120 kbd of Merey departed towards Europe in February, primarily to Spain, a level that should increase in the months ahead as uncertainty regarding Middle Eastern supply disruptions remains high.

Notably, the backlog of “sanctioned” Merey cargoes loaded before the US waiver was introduced has now reportedly been mostly cleared. Considering this, the headline discount has tightened to around $10/bbl to ICE Brent, from $12–15/bbl in late December to January (Argus Media).

While demand for Merey is set to pick up across both Europe, India, and the US, the near-term ceiling is inventories: onshore Venezuelan crude stocks sit at multi-year highs of 25 Mbbls, and offshore floating storage is hovering at 30 Mbbls, also near record highs. That overhang should keep Merey differentials pressured in the very near term.

The balance turns more constructive if Middle Eastern outages continue over a prologned period. Add firm US crude demand and incremental pull from India, and the rise in Atlantic Basin buying should keep Merey differentials supported, even as the grade competes directly with WCS Hardisty in the US market.

Venezuelan onshore crude stocks by installation, Mbbls

Source: Kpler

Market insights you can actually trust

Kpler delivers unbiased, expert-driven intelligence that helps you to track critical crude oil market developments for your own analysis. Our precise forecasting empowers smarter trading and risk management decisions. In times of conflict and geopolitical uncertainty, our real-time data keeps you ahead of supply disruptions and price volatility.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler