Renewed US-Iran conflict drives up prices

Iron ore prices held steady despite Hormuz volatility and mounting Australian supply risk, from a possible BHP strike to CMRG's export restrictions. Coal prices rebounded as renewed US-Iran tensions lifted fuel-switching dynamics. China built on its US soybean purchases, with COFCO reportedly booking cargoes ahead of a planned Trump-Xi meeting in September. Middle East hostilities also lifted aluminium prices and threaten renewed tightness in urea and sulphur supply. In freight, war-risk premiums are set to return toward pre-MOU levels as insurers reassess Middle East coverage.

Iron Ore & Steel: Prices hold steady as supply risks offset bearish fundamentals

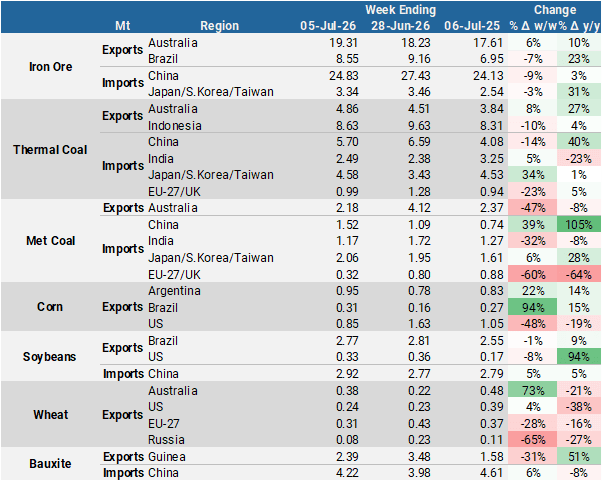

- Iron ore prices remained largely unchanged w/w despite supply disruption concerns from Australia and renewed volatility around the Strait of Hormuz. The DCE contract, September 2026 rose 0.7% w/w to close at 745.5 yuan/t on 9 July while the SGX 61% Fe August contract was trading up 0.5% w/w at $98.70/t at the time of writing. The Strait of Hormuz situation remains fluid, with fresh attacks stoking global concerns. The direct read-through to iron ore is limited, but the volatility is keeping Middle East-bound iron ore volumes subdued while adding broader risk to freight rates.

- Australia’s elevated supply is now exposed to disruption risk just as Brazil gains ground. A possible strike involving one-third of ~450 workers at BHP’s Port Hedland terminal has raised concerns, despite BHP closing a separate deal last week at South Flank/Mining Area C (a guaranteed 16% pay rise over four years plus higher allowances) has raised supply disruption concerns. BHP ships typically 0.5-0.8Mt/day from Finucane Island and Nelson Point installations. A single eight-hour stoppage will have little effect given elevated Chinese port inventories, but a longer disruption could tighten Australian supply in the seaborne market. Kpler data indicates BHP shipped 291.53Mt of iron ore from its Port Hedland operations in 2025, with around 86% of this volume bound for China. Combined with CMRG's restriction on FMG's Super Special Fines and Fortune Fines, this reinforces the narrative of tightening Australian supply into China.

- Global seaborne iron ore exports rose 7% y/y to 34.19Mt in the week ending 5 July, well above the five-year average of 30.2Mt, but roughly flat w/w. Australian shipments stood at 19.19Mt, up 10% y/y on a surge in exports to China, a run-rate current strike and CMRG risks could interrupt. Brazilian shipments eased w/w to 8.55Mt but held 23% y/y higher, gaining ground in China. Shipments to the Middle East stayed subdued on Hormuz constraints.

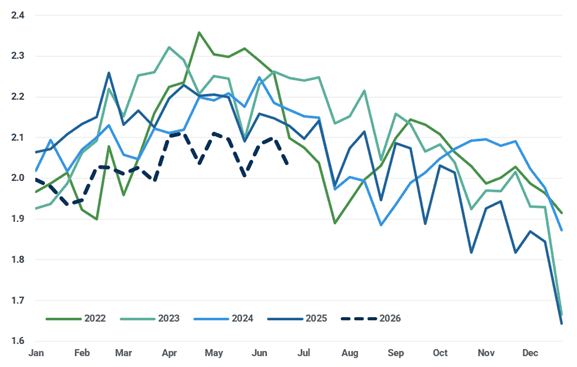

- On the demand side, Chinese seaborne iron ore imports increase 4% y/y at 25.19Mt in the week ending 5 July despite broader slowdown. BHP and Vale shipments rose 23-24% w/w, while FMG and Rio Tinto exports fell 17% and 35% w/w respectively. Yet structural headwinds continue to weigh on domestic steel fundamentals. Crude steel production by CISA member mills averaged 2.02Mt in the ten days between 20 and 30 June, off 5% y/y from 2.13Mt seen last year. Overall, June saw average daily output drop 4% y/y to 2.07Mt. Combined with ample Chinese port inventories, downside pressures outweigh the upside, keeping prices just under $100/t through H2 2026. A sustained recovery above $100/t would likely require a meaningful improvement in Chinese manufacturing and construction activity, a slower Simandou ramp-up, or a prolonged supply disruption. Hormuz remains a key monitorable from a freight perspective.

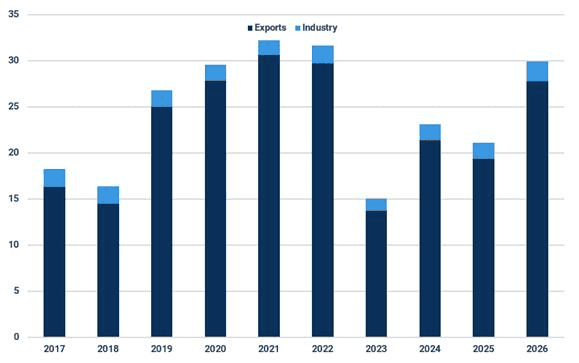

Daily crude steel production by CISA member mills (Mt)

Source: CISA

Coal: Coal prices rebound with renewed US-Iran tensions

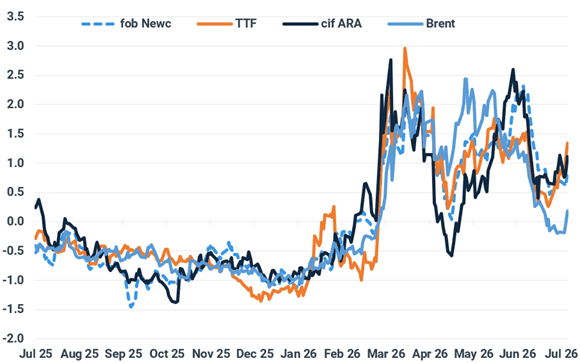

- Cif ARA and fob Newcastle paper coal prices rebounded by around $3/t this week as tensions between Iran and the US increased, with conflict reescalating once more. Gas prices are rising, and this pushes coal prices higher where fuel switching dynamics are relevant, such as cif ARA and fob Newcastle. FOB Indonesia prices trended lower in response to prolonged rainfall's cooling effect and higher hydro output in China.

Energy commodities month-ahead paper contracts (Standardised values)

Source: Enverus

- Typhoon Maysak brought heavy to torrential rain across China’s southern regions, western Guangdong, Hainan Island and Yunnan in early July. Fangchenggang and Qinzhou in Guangxi recorded localised extremely heavy rain, with hourly rates of 30 to 80mm and some areas exceeding 100mm. Coal burn potential eases as cloudier conditions reduce air conditioning driven power demand, while the added rainfall lifts hydropower output. Air conditioning demand should rise once the rain clears and the rainy season ends, as high summer heat returns. Hydropower's relative contribution should ease at the same time, driving coal burn higher again through peak summer.

- Temperatures in Japan were below seasonal norms since June and will remain mild until the end of this week, which is also reducing the call on coal generation in the country. The meteorological agency forecasts temperatures will rise above seasonal normals after 11 July, which will increase coal and gas burn.

- China's safety inspections continue to weigh on domestic coking coal prices, which increases the competitiveness of imported material. The inspections are set to continue after another accident took place in early July, which will again compress coking coal supply.

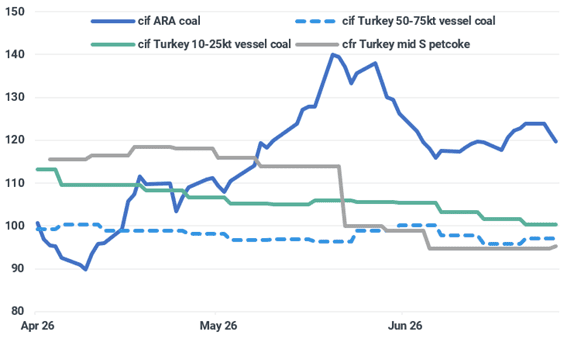

- Petcoke prices found a bottom in the US Gulf in recent weeks, as petcoke gained competitiveness against coal in India, with some fuel switching taking place. Coal still retains competitiveness against petcoke in Turkey, but utilities are burning more coal now, and Russian coal prices have room to rise, which might erode coal's price discount, now at around 5% for cement sector buyers.

Turkey & EU delivered coal and petcoke prices (NAR 6,000kcal/kg basis, $/t)

Source: Argus

Grains & Oilseeds: China builds on US soybean purchase commitment

- After 0.2 Mt of US soybean sales to China had been reported for the week ending 18 June, sales for the week ending 25 June did not show any further purchases. However, following newswires suggesting that COFCO bought at least six cargoes of US soybeans for September and October delivery. The USDA subsequently reported that a further 0.5 mt of soybeans had been sold to China. President Trump has stated that he expects to host President Xi in the US around 24 September, encouraging hopes that current Chinese buying could continue.

- The meeting should also bring clarity and re-confirmation of China’s $17 bn purchase commitment of US agricultural products, not including soybeans. China has not bought any US corn this year, and it will not be able to meet the commitment without buying corn, even when pro-rated for the rest of this year.

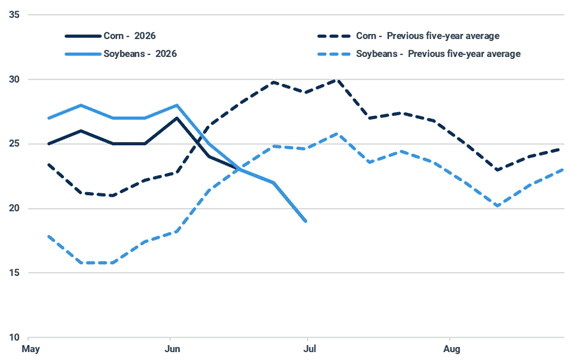

- Warmer temperatures and lighter rainfall forecast across the US Midwest over the next two weeks are raising the weather premium priced into the US grains market. While such conditions may not be optimal for the development of the corn and soybean crops, neither is currently facing significant drought. Crop condition is slightly more favourable than the historical average. By 30 June, only 19% of the US corn and soybean crop was in drought condition as rains during June were mostly average to above average. July is usually the most influential month for US corn yield potential, due to the crop’s development stage at the time, whereas for soybeans it is usually August.

US crop area in moderate or more intensive drought (%)

Source: USDA

- In contrast, the EU corn crop is facing more intensive pressure following a consecutive heatwave in short succession. The French crop rated in good or excellent condition dropped 18 percentage points w/w to 56%, the lowest rating since at least 2015. This coincides with the crop’s pollination stage, so the adverse conditions are likely to result in a yield penalty. Front-month MATIF corn has been trading at a high not seen since August 2023 and is pricing at a strong premium to MATIF milling wheat.

- Harvest of Brazil’s safrinha corn crop is underway at 29% complete by 3 July, with progress slightly lagging the five-year average. Though less than a third complete, harvest results have been reportedly positive for Mato Grosso, but less favourable yields are expected for some smaller corn-producing states due to adverse weather conditions. With showers forecast across much of southern Brazil for the short-term, this may offer little respite to the harvest delays seen in the region. Exports lineup for July have been building but are still short of last year’s level.

- Harvest of Argentina’s corn crop reached over halfway complete by 1 July, with harvest of the early crop 79% complete and the late crop 25% complete. The arrival of showers during June has slowed harvest progress as crop moisture levels remain high, but pace is still in line with the historical average. As Argentine export sales continue to exceed the pace of last year, the outlook of a stronger export campaign y/y remains likely. With corn profitably appearing relatively attractive, anticipation of a similar planted area y/y could drive export sales further given the supply outlook. Exports had dropped for June but are expected to rebound in July.

Argentine corn sales by end of June (Mt)

Source: Argentine government

- Russia has banned diesel exports until 31 July following tighter domestic supply amid Ukrainian drone attacks on refineries. Russian farmers were reportedly struggling to buy diesel, raising concerns that areas of land could be left unharvested. Harvest of the Russian wheat crop should begin later this month, and FOB offers have continued to slide lower w/w, now closer to $225/t (12.5% protein). Though the spring wheat crop had faced adverse conditions during planting, the condition of the crop appears broadly favourable across the Central and Volga districts.

Minor Bulks: Aluminium, Sulphur, and Urea operations all to be hit by fresh fighting in the Middle East

- With fewer ships in the Middle East Gulf, opportunities this time around to stockpile urea and wait for a ceasefire-enabled reopening of the Strait of Hormuz are reduced. Urea-laden vessels waiting in the Middle East Gulf hit a record high during May, then unwound fast once the Strait reopened. An extended closure could therefore be harder for producers to navigate this time without hitting output. An extended closure will also bring to an end the downturn in urea prices observed since traffic through the Strait picked up.

- The backlog of sulphur-carrying bulkers in the Middle East Gulf has also been cleared out. However, there has not been a suitable flow of vessels into the region to take the next set of cargoes. The shipping pipeline has been emptied out without replenishment. After the brief sugar rush of previously trapped Gulf cargoes hitting the market clears, we could see further sulphur supply tightness in the coming weeks.

- War-related disruption to aluminium production in the Middle East continues to reverberate along the supply chain. In addition to price spikes, competition between the US and Europe for Canadian supply has increased, while Chinese and Indonesian refineries are looking to maximise output. China increased production and exported more. Domestic aluminium output was on track to breach a self-imposed 45Mtpa capacity cap before the government stepped in with measures to curb some operations.

- The reescalation of fighting in the Middle East brought an end to the downward trend in the aluminium price. The three-month aluminium contract climbed by 1.82% net w/w to $3,132/t on 8 July, although upward momentum has slowed in recent days. Gulf smelters were able to use the recent easing in hostilities to restock aluminium-making raw materials however, an extended interruption to seaborne traffic through the Strait would see supply fears reemerge and a renewed upturn in alumina and bauxite cargoes into Fujairah and Sohar.

- Guinean bauxite exports dropped to a multi-month low of 2.39Mt in the week commencing 29 June as seasonally lower export availability curbed exports. Further falls in shipments are likely in the coming weeks as August typically represents the trough for monthly exports. Nevertheless, they should still be higher y/y. By contrast, Australian bauxite exports, primarily destined for China, climbed to an 11-week high of 1.16Mt, up by 0.38Mt y/y. Although this barely makes a mark on the seasonal drop in Guinean volumes. Despite repeated signalling, there is still no formal announcement of bauxite export restrictions by the Guinean government.

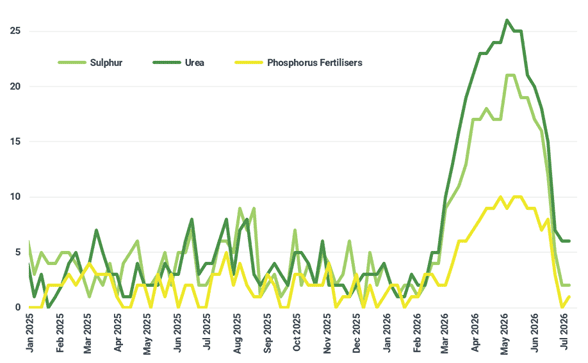

Count of fertiliser-carrying bulkers in the Middle East Gulf plunges is now sharply down on its war-time peak (Count)

Source: Kpler

Dry Bulk Freight: Middle East trade set for more war-driven disruption

- The fresh outbreak of fighting between the US and Iran will see all insurers reassessing their coverage of shipping in the Middle East, and maritime companies reconsidering their position on trading in the region. Insurance coverage will still be available however, war-risk premiums will likely return to around the 4-6% being quoted before the Memorandum of Understanding was signed.

- Even with the escalation in hostilities, it was a busy week for dry bulk carrier transits through the Strait of Hormuz with 25 ships entering the Middle East Gulf and 25 exiting in the seven days to 8 July (inclusive). Around two-thirds of these ships were laden. However, the overall trend has been for a net outflow of tonnage from the region. At 138, the number of bulkers in the MEG is down from a late February peak of more than 300 ships and a typical pre-war level of around 225 ships. As such, opportunities for floating storage of fertilisers and other commodities will be sharply reduced should there be another extended closure.

- Bunker prices are expected to rise in the coming days as war-driven oil price increases are transmitted down the supply chain. The price of 0.5% VLSFO in Singapore had dropped to the lowest level since 2 March at $636/t on 7 July, although still up by more than $100/t on the pre-war end of February level.

- Capesize earnings started the week climbing before some softness in the Pacific slowed upward momentum. Nevertheless, the 5 TC average still closed the week up by a net $5,871/day w/w at $41,434/day. The Atlantic is likely to lead further growth as Brazilian iron ore exports ramp up, pulling in a flow of ballasters from the Pacific.

- North Atlantic Panamax demand benefited from robust US East Coast-India thermal coal chartering activity. Combined with fronthaul grains chartering out of East Coast South America, this has bolstered Atlantic earnings and reduced vessel supply in the basin. From a recent peak of more than 450 ships, the number of Panamax (68,000-99,999 dwt) ballasters in the Atlantic has fallen to around 350 vessels. The Atlantic round-voyage rate climbed by $1,037/day w/w to $23,127/day, but the upward momentum slowed towards the end of the week. A similar trend is observable in the Supramax market, where a rising ballaster count in the Pacific has put earnings in the basin under pressure. However, a short-term spike in Chinese port congestion caused by recent cyclone activity should tie up some tonnage. By contrast, US Gulf earnings continue to firm, helping the 11 TC average edge up by $322/day w/w to $21,490/day.

- In contrast, the Handysize 7 TC average dropped by $484/day w/w to $16,506/day as falls across all Pacific routes and west to east Atlantic trades pulled the index lower. Supply is outpacing demand in both basins as the ballaster count climbs. However, a short-term acceleration in Latin American grain loadings, notably corn and soybean meal from Argentina, should provide some support.

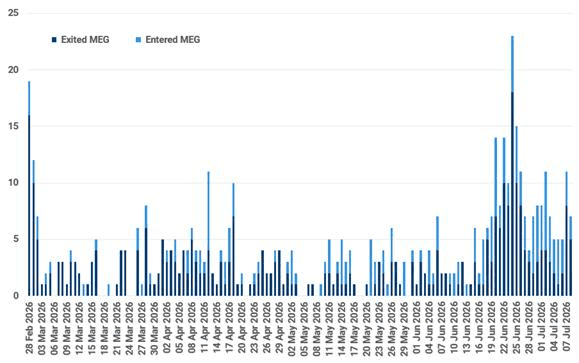

Dry bulk carrier transits through the Strait of Hormuz by direction (Count)

Source: Kpler

Key Dry Bulk Market Developments

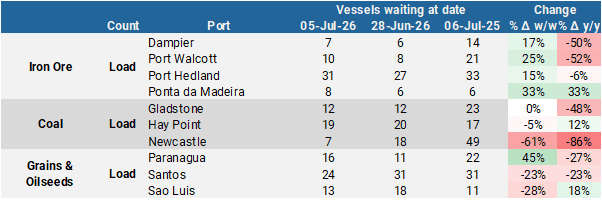

Dry Bulk Commodity Flows

Source: Kpler

Dry Bulk Port Congestion

Source: Kpler

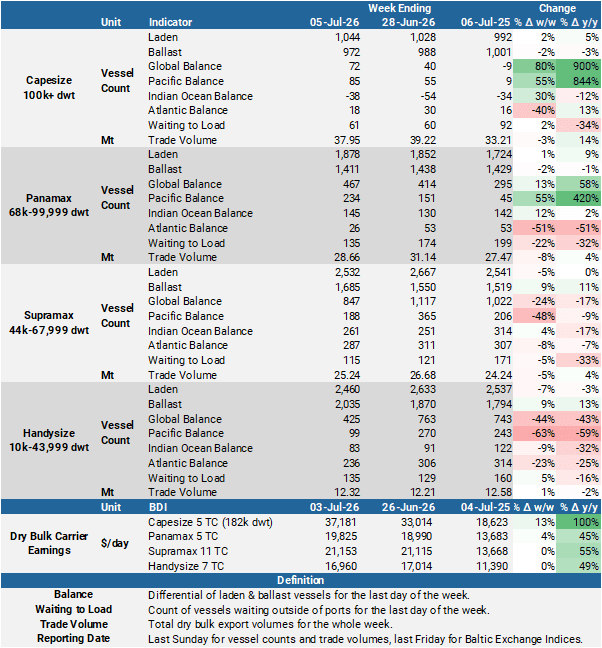

Dry Bulk Freight Metrics

Source: Kpler, Baltic Exchange

See why the most successful traders and shipping experts use Kpler

Request a demo