Russian waivers reshape crude flows regardless of time limits | The Arb View

Middle Eastern supply disruptions have become clearer, with roughly 8 mbd offline and exports dropping to 6.8 mbd last week versus ~19 mbd pre-conflict, though Russian waivers and reserve releases are cushioning the prompt market. Continued Indian demand for discounted Urals should limit replacement buying of Atlantic Basin barrels, keeping the Brent–Dubai EFS biased softer despite geopolitical risks. Meanwhile, tighter Mediterranean sour balances and stronger European refining demand are supporting CPC and select Atlantic Basin grades, while competitive Midland arbs continue to pull U.S. barrels into Asia.

Executive Summary

Arbitrage Values (16/03/2026 07:30 UTC)

Source: Kpler

Trading Calls

- Neutral to softer Brent–Dubai EFS. As Indian refiners are likely to secure cheaper prompt barrels, regardless of the time-bound waiver, limiting the demand for Atlantic Basin barrels.

- Bullish CPC diffs. Recent strengthening of the Caspian grade could see further upside as European and Asian demand picks up due to locked up Middle Eastern barrels.

Middle East and Asia: EFS Could Ease Further Despite Time-Bound Russian Waiver

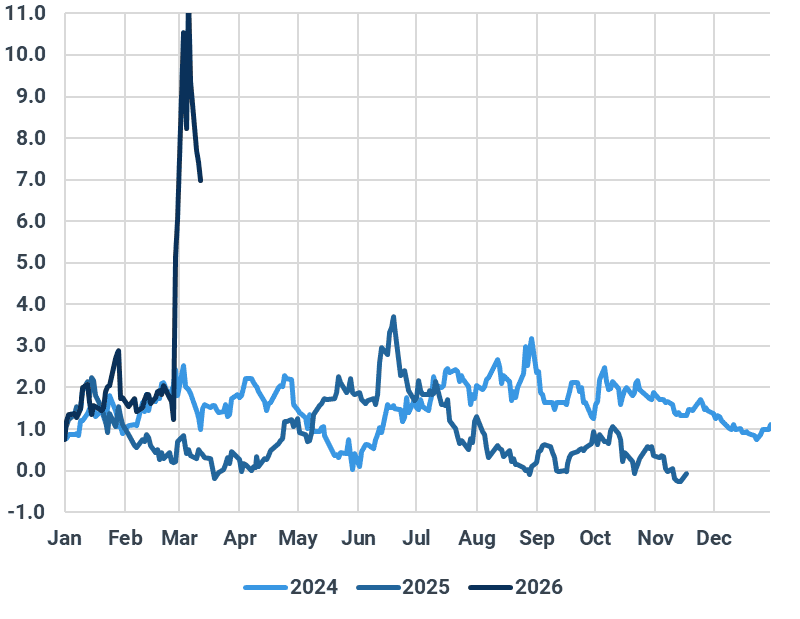

Tanker attacks and port facility explosions kept flat price extremely volatile throughout last week, with ICE Brent May Futures settling around $103.14 last Friday. Renewed threats around Kharg have also kept nerves high, and as long as infrastructure and vessels remain exposed, volatility should stay elevated in the coming weeks as the market continues trading headlines.

That said, the physical supply disruption has become much clearer. Kpler’s latest supply data now point to an 8mbd outage of crude supply across the Middle East, potentially rising toward 10 mbd if outages persist. Export data also show that only about 6.8 mbd of crude (2.6mbd Yanbu, 2.4mbd Fujairah, 1mbd Kharg and 0.8 mbd Muscat) was lifted out of the region last week, against an average of roughly 19 mbd prior to the conflict. Despite this, the EFS has eased to around $7/bbl after trading above $10/bbl, and we expect the spread to trend lower this week. Russian crude waivers, SPR releases, and record Chinese inventories are cushioning the prompt market, although that buffer may tighten if the war extends.

A key part of that cushion is the reopening of Russian flows into India following the latest US waiver. Indian refiners are likely to continue favouring Urals, which on our arb dashboard is landing roughly $18/bbl below the Dubai swap and more than $30/bbl below most Atlantic Basin replacements. As long as supply of Russian crude remains stable, India is likely to remain heavily reliant on these barrels regardless of the time-bound waiver, reducing the urgency to compete for alternative supply. There are also early signs that some cargo traffic may still be moving through the Strait. LPG tankers have transited the strait, indicating India’s strong relationship with Iran, which could offer an early signal of a limited reopening if crude vessels begin to follow. Together with reserve releases from Japan and South Korea, these factors should help temper replacement buying and keep pressure on the EFS.

Freight will likely be the next key signal for arbitrage flows. TD15 has dropped to around WS 162 from the peak near WS 285 earlier this month, which is beginning to improve the economics for long-haul Atlantic Basin cargoes into Asia. Angolan grades such as Dalia and Hungo are starting to look more workable on forward programmes into Asia, and flows could begin to emerge if freight continues to ease.

Brent-Dubai EFS

Atlantic Basin: CPC leads the strength as Europe locks in barrels

Diffs for Atlantic Basin grades, particularly WAF and MED assessments have barely reacted to the Middle Eastern conflict mainly due to lower European demand, high freight rates and increased volatility which have made long-hauls risky for Asian refiners. We think that picture could start to shift, with CPC continuing to lead the move. In our previous report, we noted that CPC assessments were too low given how well it works for both Europe and Asia, and that correction is now clearly underway. Liftings reached around 1.9mbd last week, the highest of the year, with most barrels heading into Europe. As refiners return from maintenance, CPC is likely to be one of the first grades they secure, especially given how economical it is, with April deliveries landing at about 60c/bbl lower than Dated Swap.

The European refining backdrop is also providing strong support. Product margins remain firm given the disrupted supply from the Middle East, giving refiners every incentive to maximise runs and pay up for feedstocks that fit well. At the same time, Europe has lost roughly 600 kbd of Iraqi crude, tightening Mediterranean sour balances almost immediately. This should continue supporting CPC while also lifting the value of nearby alternatives such as Es Sider and Azeri Light.

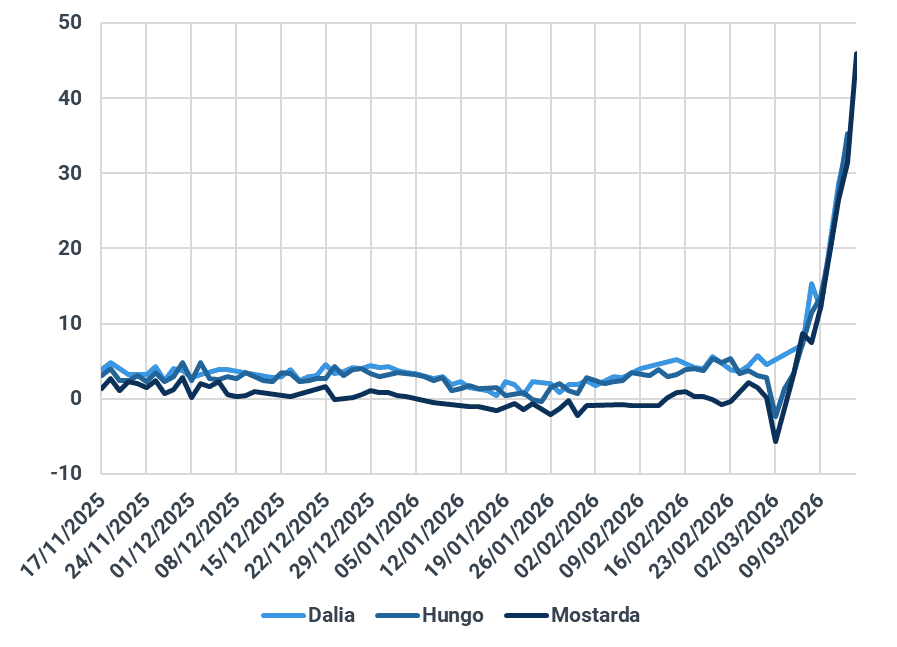

WAF has been slower to respond, but we expect demand to start picking up in the coming weeks. The wide Brent–Dubai EFS and the earlier spike in freight had priced Brent-linked barrels out of Asia, pushing Nigerian differentials lower and forcing NNPC to reduce OSPs. That dynamic is now beginning to shift. Freight has eased, the EFS has pulled back from the highs, and the economics for some WAF sour grades are starting to look more competitive. LatAm grades should also continue attracting demand. Brazil and Guyana have already been repriced higher on replacement demand, and spot availability from Guyana appears tight enough to keep those barrels supported.

WAF Sour Arbs to East

Source : Kpler

Americas: Midland Arbs Keep US Barrels Flowing East

Midland remains competitively attractive into Asia against Murban given how constrained Gulf supply remains, and that matters even more as buyers look beyond prompt coverage into May and June runs. Japanese refiners have already stepped up purchases of US barrels, with roughly 3 mmbbl of Midland fixed for April loading, while reserve releases from Japan and South Korea should help cover near-term shortages rather than eliminate the need for imports altogether. On our arb dashboard, Midland eastbound margins are now around $4/bbl for June deliveries, reinforcing the economics for additional flows toward Asia.

If Hormuz is not reopened soon, more US crude should start clearing into Asia, especially from May loadings onward, helped by the recent pullback in TD22 freight rates. Europe is less straightforward. Lower freight does improve the case for some prompt WTI into NWE, but European refiners still appear more inclined to favour CPC and nearby Mediterranean grades. Meanwhile, recent strength in Midland differentials has effectively shut the arb to NWE, making it roughly $3/bbl less competitive relative to Ekofisk.

On the sour side, strong jet and diesel cracks are keeping US refinery demand healthy, so prompt tightness in grades like Mars is unlikely to ease much. We could still see occasional flows as Asian refiners, particularly in Japan and South Korea, seek alternatives to Middle Eastern barrels. ANS, for example, has recently re-entered South Korea after nearly a one-year hiatus. For now, however, light sweet barrels remain better placed for export than the broader US sour complex.

Arb Values for Selected U.S grades to Eastern Asia

Source : Kpler

Kpler Arbitrage

Kpler’s Arbitrage platform turns complex freight, quality, and benchmark data into simple, actionable arbitrage insights so you can discover value windows, rank opportunities, and build scenarios confidently. With Arbitrage you can:

- Compare delivered crude values by region and freight cost

- Quantify refining margins and route profitability

- Spot open arbitrage opportunities quickly

- Breakdown value drivers like FOB differentials, spreads, and freight

- Model scenarios with custom market inputs

See why the most successful traders and shipping experts use Kpler