The Fed's undeniable hawkish pivot

The FOMC's June projections shift decisively hawkish as inflation forecasts rise considerably.

Summary

- Hawkish Pivot: The FOMC held the Fed Funds rate at 3.5 – 3.75% as expected. However, the Summary of Economic Projections shifted decisively hawkish, with the median expectation for 2026 headline inflation revised up to 3.6% and core to 3.3%, both up from 2.7% in March. The median dot now implies one hike by year-end, a sharp reversal from March’s projected cut.

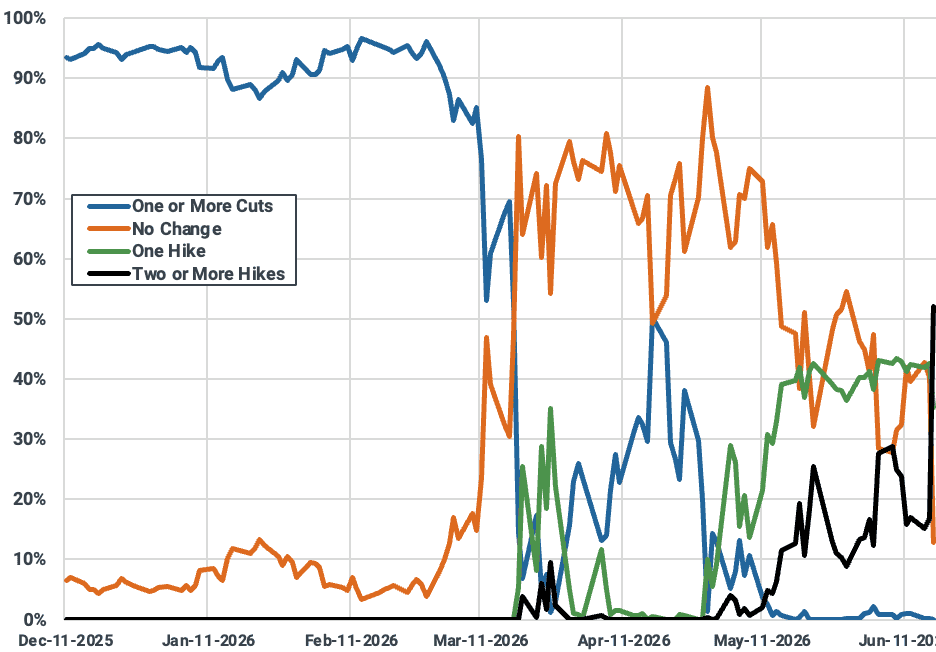

- Warsh Takes a Hard Line: In his first meeting as Chairman, Kevin Warsh reiterated the 2% target and struck a more hawkish tone than expected, stressing the committee’s unanimous commitment to price stability. Markets read the SEP, and Warsh’s statements clearly – the 2y yield surged to a more than 12-month high 2.21%. Futures markets have also lifted the chances of a two-hike outcome by the end of the year to 52%, up from 17% the day prior.

- A New Communication Style: Warsh signaled a leaner approach to Fed communications, shortening the policy statement, cutting back on forward guidance, and excluding himself from the dot plot. He also lans to launch five task forces to reshape the Fed’s approach to communications, the balance sheet, AI productivity, and its inflation framework.

Market Analysis

On June 17, 2026, the FOMC voted to keep the Fed Funds rate steady at 3.5 – 3.75%, in line with market expectations. Kevin Warsh also began his tenure as the next Chairman of the Federal Reserve, replacing Jerome Powell. There were two core takeaways from the meeting. First, the Fed remains committed to dealing with inflation, pivoting towards a more hawkish position. Second, Warsh will say less and forego providing forward guidance.

The Fed’s Summary of Economic Projections (SEP), which provides the FOMC’s median expectation for growth, inflation, the unemployment rate, and the Fed Funds rate clearly shifted towards a more hawkish position. While the median forecast for real GDP growth in 2026 was cut by a limited 20bp to 2.2%, relative to the March 2026 meeting, inflation forecasts were revised higher aggressively. The median committee member now sees 2026 headline inflation at 3.6%, and core inflation at 3.3%, both of which were originally 2.7% as of March. Unemployment was also lowered by a slight 10bp to 4.3%.

The dot plot, which reveals the outlook for the Federal Funds rate, also shifted dramatically, reflecting rising FOMC inflation projections for 2026 and the simultaneous cut in unemployment expectations. The committee now sees the median Fed Funds rate at 3.8% by the end of the year, which equates to roughly one hike. This is a notable change from March, when the FOMC expected a median Fed Funds rate of 3.4%, implying one cut.

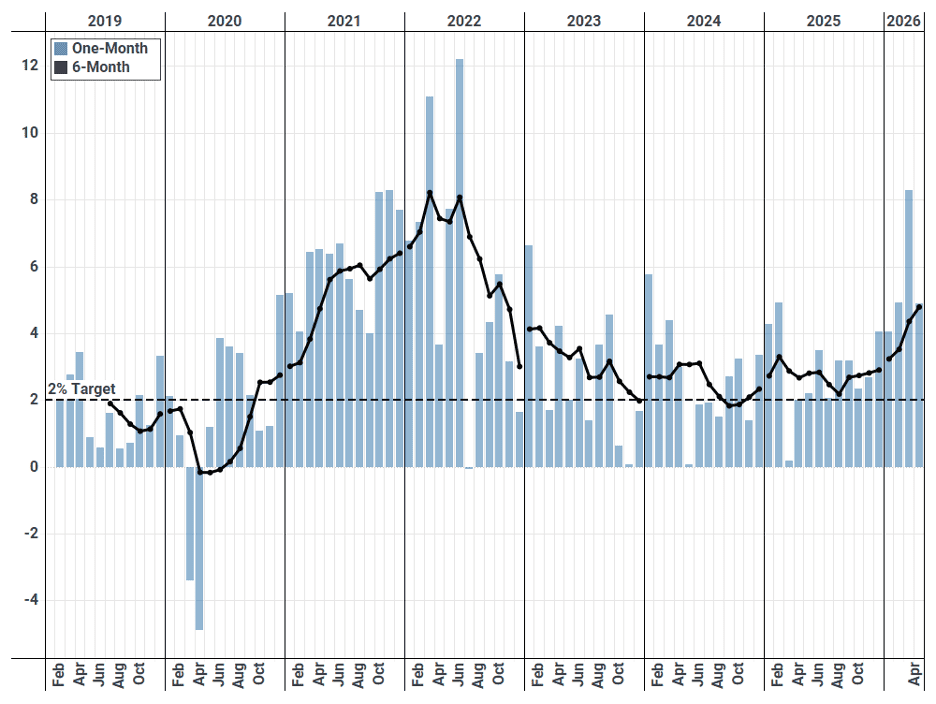

US One- and Six-Month Pace of PCE-Based Headline Inflation (%)

Source: BEA

The Federal Reserve has good reasons to be concerned about inflation. Even before the war in Iran had begun, core PCE-based inflation was running at a six month pace of 3.8% annualized, well off a 2.5% annualized low seen through the summer of 2025. The six-month pace of headline PCE-inflation for April accelerated to a blistering 4.8% annualized as the Iran war raises energy prices. Some of this will eventually pass through to the broader economy and core inflation, even as energy prices decline off recent highs.

Warsh also reiterated the Fed’s 2% target, taking a hard line on the inflation issue. This was quite possibly the biggest open question of the FOMC meeting – how would Warsh come out in his first press conference? Warsh said that inflation has been a problem for years. He later added that “Members of the FOMC are unambiguous and unanimous that this committee will deliver price stability.” In the official policy statement, inflation had the last word “The Committee will deliver price stability.” Warsh was more hawkish than expected.

Probability of Fed Funds Path Through End-2026 (%)

Source: CME

The market clearly interpreted the FOMC statement and press conference as hawkish. The 2y yield surged to 2.21%, marking a fresh all-time high, and narrowing the 2s – 10s spread to 0.29%. This tends to happen when central banks get more hawkish. Fed Funds rate futures raised the possibility of a two rate hike outcome by the end of 2026 to 52%, up from 17% the day prior. After starting the year with a 93% probability, the chances of any rate cut this year has since fallen to zero.

We also learned a bit more about how Warsh will lead the Federal Reserve. Warsh intends to shorten the Fed’s policy statements and cut back on forward guidance. In his first meeting, the existing policy statement was already cut by several paragraphs. Warsh also excluded himself from the dot plot. Warsh also intends to appoint five separate task forces intended to reshape how the Fed approaches communications, economic data, the balance sheet, AI productivity, and inflation frameworks.

See why the most successful traders and shipping experts use Kpler