The US downstream system running in max-output mode

US downstream operations are running at full throttle, with utilisation at multi-year highs as global markets scramble for refined products and the US increasingly acts as the key marginal supplier. Strong refining margins and lighter maintenance schedules have supported elevated throughput, while run cuts across the East of Suez have increased reliance on Atlantic Basin refiners. Refined product exports have surged to record levels, tightening domestic balances and pushing major product stocks to five-year lows.

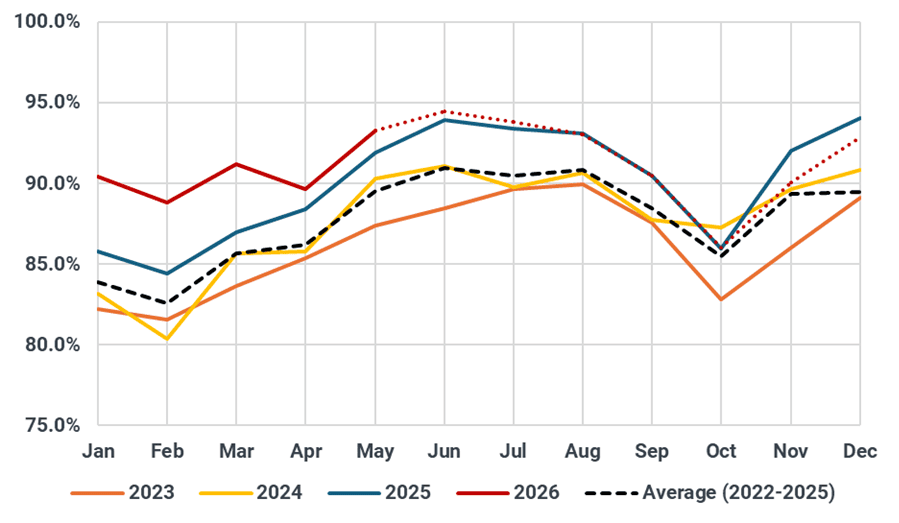

US downstream operations are running in full max-output mode, with refinery utilisation at multi-year highs, refiners maximising distillate yields, and refined product exports reaching record levels amid tightening global product balances. Refinery utilisation has climbed to near-record seasonal highs, with the latest EIA weekly data showing utilisation averaging close to 93% in the first week of May, around 4 percentage points above seasonal averages despite a modest uptick in unplanned maintenance activity. We expect refinery runs to remain above 16.5 Mbd during May, with Q2–Q3 averages projected around 16.5–16.7 Mbd, supported by lighter turnaround schedules and relatively stable operating conditions. Although some unplanned outages have emerged since April, disruptions have largely remained within historical operating ranges and have not materially impacted overall throughput.

US Refinery Runs Utilisation (%)

Source: Kpler

Reduced spare refining capacity across the Atlantic Basin has tightened the system following refinery closures across Europe and parts of the US in recent years. At the same time, refinery run cuts across the East of Suez have increased reliance on Atlantic Basin refiners to maximise available capacity. The US, alongside Nigeria’s Dangote refinery, has therefore emerged as a key balancing hub for global product markets. However, prolonged high utilisation is also increasing operational strain across the refining system, raising the risk of further unplanned outages and operational incidents during the peak summer period, similar to the recent disruptions and maintenance events seen at BP Whiting refinery, Valero Port Arthur, and Exxon’s Baytown refinery.

Strong refining margins continue to support elevated throughput. Diesel and jet cracks remain structurally strong, while gasoline margins have improved ahead of the summer driving season. Gulf Coast refiners, particularly those with high conversion capacity and strong distillate yields, remain well positioned to capture both domestic and export demand. With US gasoline and Atlantic Basin middle distillate balances remaining structurally tight, the market has limited flexibility outside of maintaining high refinery utilisation rates.

Elevated refinery runs have also been supported by growing flexibility to process lighter domestic crude grades. Since 2015, the weighted average API gravity of crude processed in US refineries has risen by around 2.2 points as shale production increasingly shifts toward lighter barrels. This evolution has allowed refiners to rely more heavily on domestic crude supply and sustain high throughput levels despite tighter global heavy crude availability and disruptions to heavier crude flows.

US Major product stocks hit five-year lows as exports surge

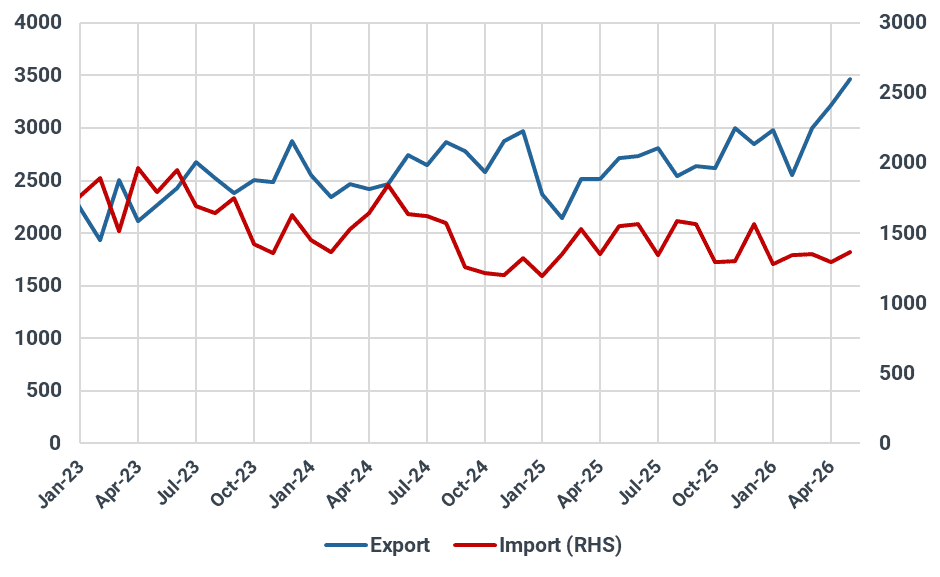

US refined product exports have surged to record levels as the country increasingly acts as the key marginal supplier amid ongoing Strait of Hormuz disruptions. Favourable export arbitrage economics, declining imports, and reduced refinery activity across Asia and the Middle East have increased global reliance on Atlantic Basin barrels. This has driven stronger demand from Europe, Latin America, Africa, and Asia as buyers work to replace lost Middle Eastern supply and stabilise inventories. US clean product exports have averaged around 3.3 Mbd since March, compared with roughly 2.8 Mbd during the first two months of 2026 and a 2025 average of around 2.6 Mbd, highlighting the sharp acceleration in export demand following the disruption.

US Refined product exports (Kbd)

Source: Kpler

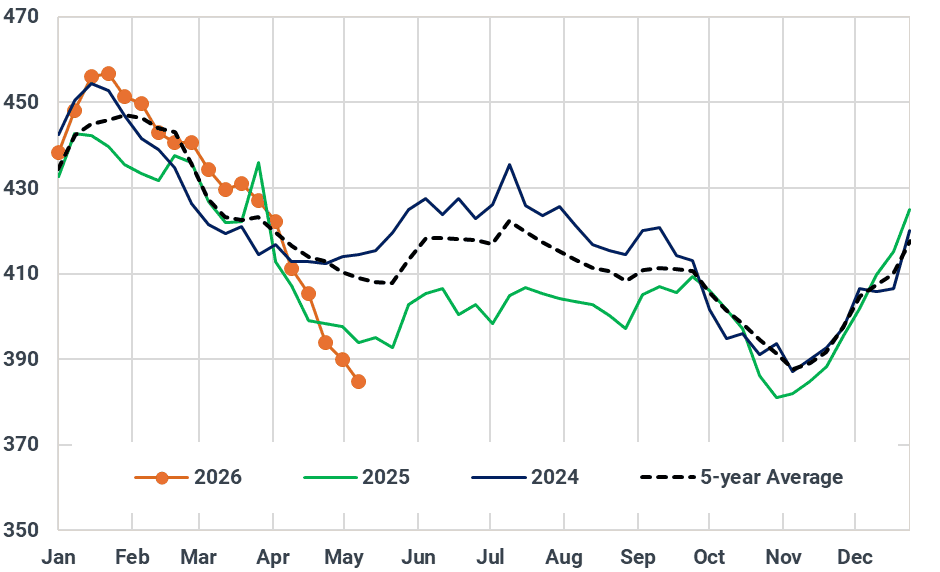

The rise in exports has significantly tightened domestic product balances and inventories, with gasoline, diesel, jet fuel, and fuel oil stocks falling to five-year lows. Since the start of the conflict, total major product stocks have declined from around 440 million barrels (on 3rd March) to roughly 385 million barrels as of 9 May. The nearly 55-million-barrel draw over the past ten weeks marks the largest decline in year(s), leaving balances considerably tighter heading into peak summer demand.

US major product stocks (mbbls)

Source: Kpler

Note: Stocks of Gasoline, Jet, Gasoil and Fuel Oil

Conclusion

US refinery runs are expected to remain elevated through the coming months as strong product cracks, tightening global balances, and robust export demand continue to support high utilisation rates despite lower operable refining capacity. Downside risks also remain elevated as sustained high utilisation increases operational strain across the refining system, raising the likelihood of further unplanned outages during the peak summer period. With global product markets structurally tight, the US is increasingly acting as the primary balancing supplier to global product markets. As the summer driving season approaches, refiners are expected to continue maximising gasoline and distillate production to meet both domestic and export demand, with higher refinery runs remaining the key balancing lever for the market. With inventories already at multi-year lows, any additional refinery disruption could tighten Atlantic Basin product balances even further.

Market insights you can trust

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler