US turns to Iranian oil to cool prices, but barriers remain high

For the third time in two weeks, the US has issued temporary waivers on sanctioned oil in a bid to rein in prices. This time, however—targeting Iranian oil afloat—the move is far more complex than previous rounds.

Key takeaways:

- US waivers on Iranian oil afloat could unlock ~5 mbd of supply within a month, but cannot offset sustained Middle East disruptions.

- Sanctions from other jurisdictions, payment constraints, and shadow fleet risks remain key barriers, limiting immediate uptake.

- Asian buyers—led by India and China’s state-owned refiners—are best positioned to step in, though compliance and pricing will shape the pace.

- Chinese teapots, currently the largest Iranian oil buyers, face a dilemma between accepting higher prices and risking future supply access.

The US issued a 30-day general license on Friday night, allowing countries—including the US, but excluding Cuba, North Korea, and Crimea—to purchase Iranian crude and products loaded before March 20. The waiver follows two similar orders earlier this month that granted the green light for purchases of Russian oil already on the water.

The move is clearly another attempt by the Trump administration to curb surging oil prices, which have been fuelled by intensifying Iranian attacks on energy infrastructure in the Middle East and the prolonged disruption to navigation through the Strait of Hormuz.

Kpler data shows that around 170 mb of Iranian crude is currently on the water, with approximately 154 mb located outside the Middle East Gulf. The volume has eased from a peak of about 185 mb in late February, when Iran accelerated shipments, likely in anticipation of the conflict.

If these cargoes are managed to be taken by refiners within a month as the US waiver requires, it represents 5.1 mbd of additional oil supplies to the global market, or a third of the oil flows through the Strait of Hormuz before the war.

Iranian crude oil on water by current location, mb

Source: Kpler

However, the reality is far more complex. Iranian oil is subject to a dense web of international sanctions imposed by the U.S., EU, and UK, which include strict restrictions on financial settlements and access to the U.S. dollar payment system. Consequently, for many years, China’s independent refiners—the largest buyers of Iranian oil—have adopted complex payment systems involving RMB, other non-dollar currencies, and financial institutions across multiple jurisdictions.

The U.S. General License issued on Friday does not explicitly detail the mechanisms for oil payments—specifically, it remains unclear whether buyers can settle transactions in U.S. dollars via the SWIFT system, or if Iranian sellers will be granted unfettered access to these U.S. dollar accounts.

Then there is the problem with shipment. Iranian oil is typically carried by aged (20+ years), often-sanctioned tankers without proper insurance coverage. These vessels frequently falsify their information to disguise their identity, allowing them to evade potential incidents or liabilities. The environmental risks posed by allowing this shadow fleet to enter territorial waters and dock at ports create an additional layer of concern for potential buyers.

From the oil seller’s perspective, beyond transaction issues, buyers are expected to demand detailed trade and shipment information. Providing this data would expose the entities and vessels involved, potentially creating a trail of evidence and making them targets for future sanctions if the U.S. continues its enforcement against Iran.

Setting these concerns aside, Asian refiners—such as Indian buyers and China’s state-owned firms that have recently stepped up purchases of Russian crude following the US waiver—may be willing to take Iranian cargoes to ease feedstock tightness, given their ready availability and significantly lower pricing compared to compliant barrels in the market.

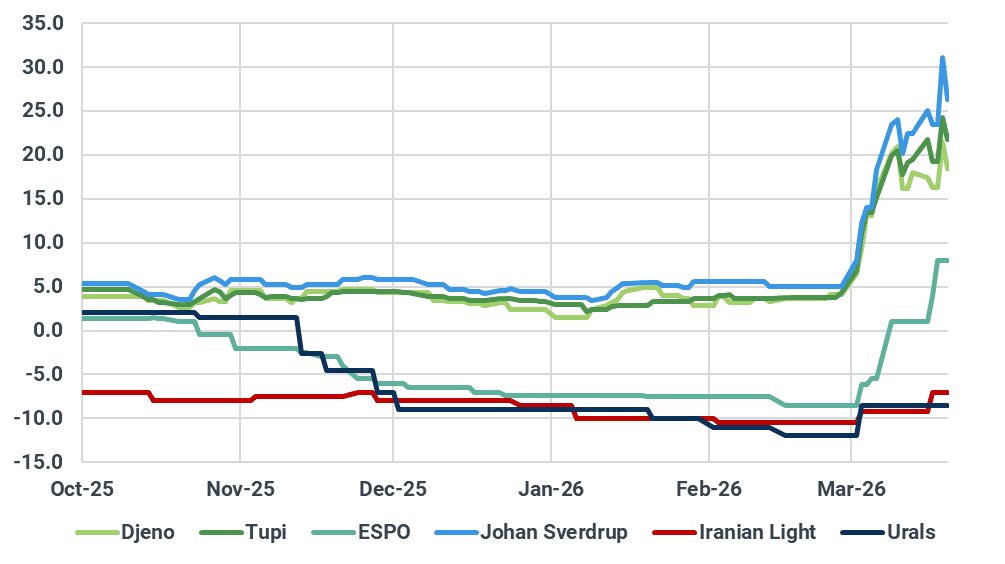

Iranian Light was trading at around ICE Brent -$7/bbl on a delivered basis into China earlier this week, firmer than the -$11/bbl level seen prior to the conflict, but still more than $25/bbl cheaper than Brazilian and West African grades. Some market participants told Kpler that offers for Iranian crude were paused from Thursday after US Treasury Secretary Bessent signalled a potential easing of sanctions in a news interview, as sellers held back in anticipation of stronger demand and higher prices. For context, Russia’s ESPO crude prices have jumped by around $14/bbl since the US granted sanctions waivers.

Selected crude diffs against ICE Brent on DES China basis, $/bbl

Source: Argus Media

That said, China’s independent refiners face a dilemma. According to Oilchem, average refining margins at teapots are below $10/bbl, meaning any sharp increase in Iranian crude prices would erode most of their margins or even push some into losses. However, refiners also worry that the US waiver could be extended—similar to those for Russian oil—or even evolve into a broader lifting of sanctions in a post-war scenario, as seen with Venezuela, potentially pushing Iranian crude prices even higher and limiting their access to supply.

For now, most Chinese teapot refiners hold relatively ample inventories, covering roughly 20–30 days of demand. As such, any near-term supply tightness—if other buyers step in to secure cargoes under the current US license—should not pose a major threat to their operations. The bigger uncertainty, however, is whether the US intends to permanently ease sanctions on Iran, or if this is merely another tactical move to buy time in the conflict.

Among Asian buyers, Indian refiners and China’s state-owned firms are the most likely to move quickly into Iranian oil procurement, while others in Japan, South Korea, and Southeast Asia may take longer to clear internal compliance requirements, judging by their response to the Russian waivers.

From an India perspective, the waiver reintroduces optionality, but the pace of buying will be key. India was historically a major buyer of Iranian crude, accounting for ~10–12% of imports at peak, before flows ceased in 2019. While refiners retain full operational flexibility to process Iranian grades, current sourcing is heavily skewed toward Russian and Middle Eastern barrels. Market sources indicate Indian refiners have already secured a significant volume of Russian crude for April arrival (~1.8–2.0 mbd).

At the same time, Indian refiners are currently running at elevated utilization, partly driven by domestic LPG supply requirements and fuel security, which is keeping overall crude demand firm.

In this context, the availability of Iranian barrels on the water offers additional sourcing flexibility, particularly if disruptions through the Strait of Hormuz persist. Indian buyers may opportunistically secure these cargoes to ensure feedstock availability and diversify supply, potentially up to 1 mbd.

However, pricing and benchmark dynamics will remain key. Historically, India has purchased Iranian crude on Dubai/Oman-linked pricing, but with Middle East benchmarks currently distorted, this could limit attractiveness. As such, preference may tilt toward Brent-linked barrels unless Iranian pricing remains sufficiently competitive.

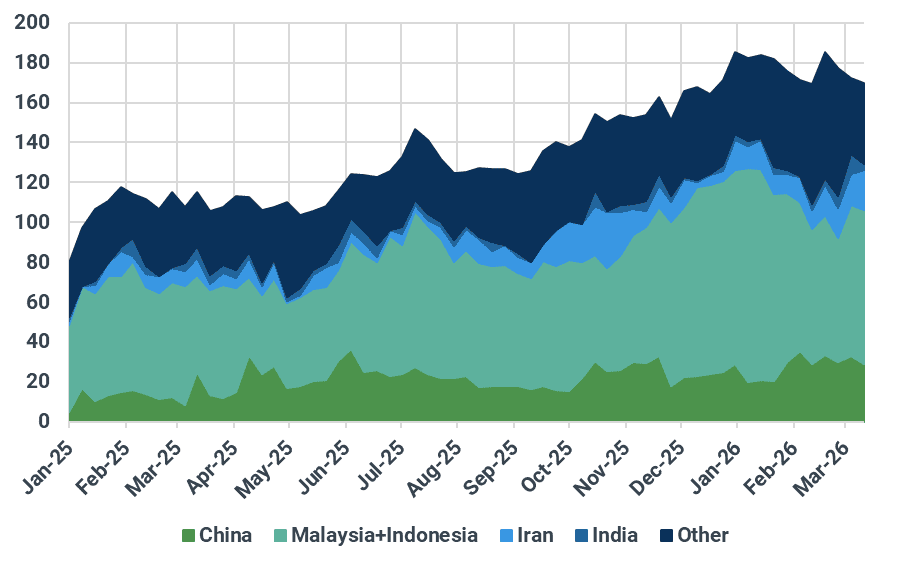

Iran's crude/co exports by destination, kbd

Source: Kpler

Market insights you can actually trust

Kpler delivers unbiased, expert-driven intelligence that helps you to track critical market developments for your own analysis. Our precise forecasting empowers smarter trading and risk management decisions. In times of conflict and geopolitical uncertainty, our real-time data keeps you ahead of supply disruptions and price volatility.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler