Value of crude, product, LNG and LPG trapped in the Mideast Gulf rises to $20bn

This article estimates the market value of liquids currently stranded in the Mideast Gulf.

Over the past two weeks, markets have swung between hopes of a US-backed reopening of Hormuz and renewed military escalation. Yet the key indicator, actual Mideast Gulf (MEG) exports via Hormuz, remains near a trickle . Total liquids exports via Hormuz fell from around 20 mbd pre-conflict to roughly 1 mbd in April, forcing global markets to rebalance through supply losses, refinery run cuts, and demand destruction.

Persistently subdued outflows, combined with rising MEG commodities-on-water (COW) volumes since late April, pushed the value of crude, CPP, DPP, LNG, LPG, and ammonia stranded inside the Gulf to around $19.9bn (see Methodology).

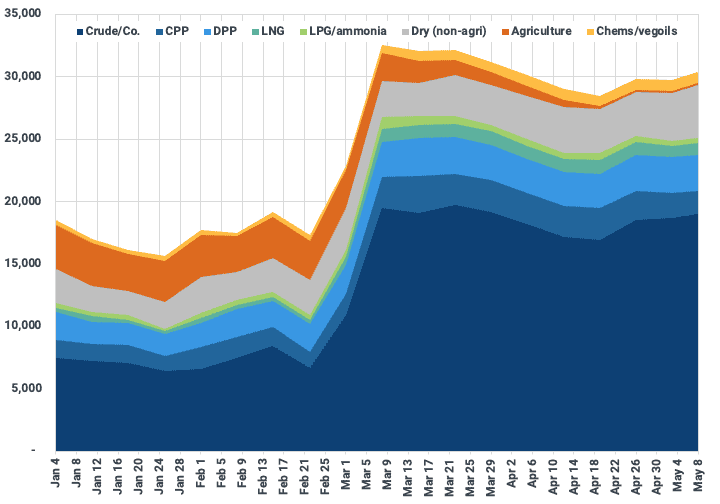

Chart 1: Mideast Gulf - Commodities-on-Water (excluding containers) [kt]

Source: Kpler

The increase in MEG COW volumes was driven primarily by a rise in Iranian crude floating storage, as the US blockade forced Iran to use remaining ballast tankers in the Gulf to absorb excess supply. Spare capacity is rapidly diminishing, pointing to further production shut-ins in the coming weeks. Cumulative Middle Eastern crude supply losses reached 782 mbbl by May 8 and are approaching 1,000 mbbl by late May.

Methodology – Commodities-on-water market value

- Volumes: Commodities-on-water as of May 7

- Prices: Spot/front-month as of May 7, applied across all cargoes, including term volumes

- Scope: Crude, clean products, dirty products, LNG, LPG, ammonia

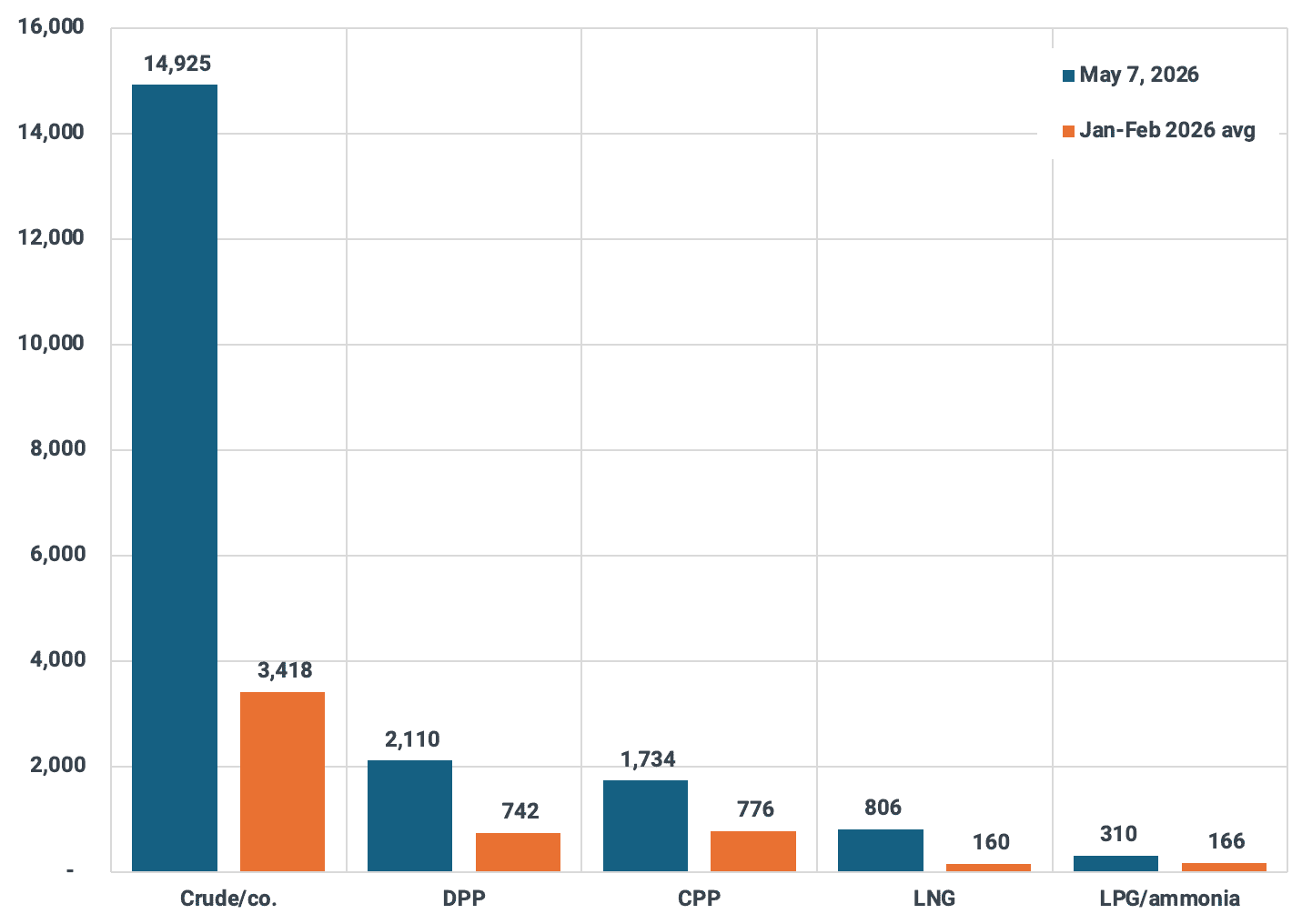

Kpler estimates the market value of crude, CPP, DPP, LNG, LPG, and ammonia currently on the water in the MEG at around $19.9bn. Crude accounts for roughly 75% of total value, followed by DPP (11%), CPP (9%), LNG (4%), and LPG/ammonia (1.6%).

Compared with the January-February 2026 pre-war average, the largest overhang remains LNG, where the current value is around 5x higher, followed by crude (4.4x) and DPP (2.8x).

Chart 2: Mideast Gulf - Commodities-on-Water [million USD]

Source: Kpler (volumes), Argus Media (pricing)

See why the most successful traders and shipping experts use Kpler