Venezuelan crude fills the feedstock gap left by Middle Eastern disruption

The Strait of Hormuz closure severed a critical supply line for US Gulf Coast refineries — not just of crude oil, but of the heavy residual material their specialist processing units need to maximise diesel output. Venezuelan crude has stepped in to fill both roles, and is likely to remain strategically important even after the Strait reopens.

Key Takeaways

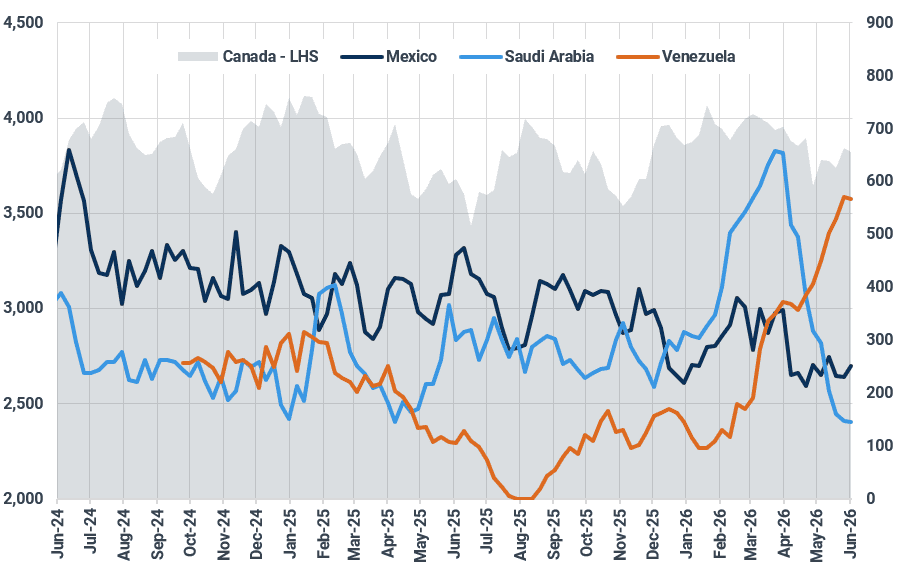

- US crude imports from Venezuela have surged to their highest level since 2017, with Venezuela now the second-largest crude supplier to the US after Canada — accounting for 10% of total imports, up from just 2% a year ago.

- Venezuelan crude produces more of the heavy residual material that large, complex US Gulf Coast refineries need to run their specialist diesel-conversion units at full capacity.

- The economics favour Venezuelan crude over comparable alternatives: Venezuela's Merey grade is priced roughly $4 per barrel below similar Canadian crude, while delivering equivalent or better diesel output for refineries equipped to process it.

- Middle Eastern supply will not quickly return even after the Strait of Hormuz reopens. Low regional inventories, production ramp-up times, and high summer domestic energy demand in the Gulf will limit exports throughout the third quarter of 2026.

US crude oil imports from Venezuela have risen sharply in recent months and are expected to reach a new high in June, returning to levels last seen in 2017. According to the EIA, Venezuela surpassed Saudi Arabia and Mexico in May to become the second-largest crude supplier to the US after Canada. Venezuelan imports now account for 10% of total US crude imports, compared with 2% at the same time last year, while Canadian volumes have increased from 59% to 65%.

US crude imports by countries of origin (kbd)

Source: EIA

The rise in Venezuelan and Canadian crude imports is partly a structural response to the Strait of Hormuz closure in April, which cut off flows of both crude and heavy fuel oil from the Middle East to the US. It also reflects declining volumes from Mexico and Saudi Arabia, and the need for US refineries to maximise production of diesel and jet fuel as domestic inventories remain low.

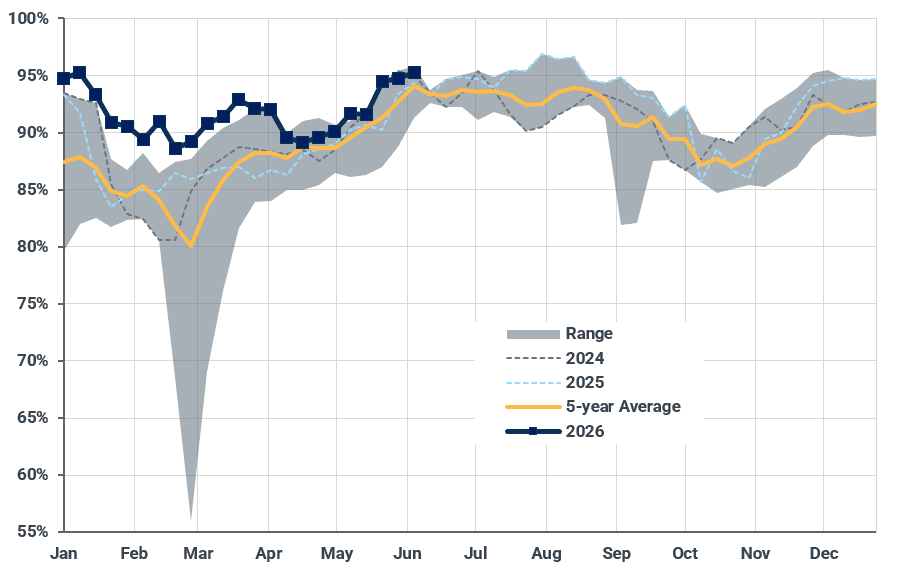

After completing the spring maintenance season in late May, US refinery utilisation rates climbed above 95% in early June and are expected to stay elevated throughout the summer driving season.

US refinery utilization (%)

Source: EIA

For many large US Gulf Coast refineries, the type of crude they process matters as much as the volume. These facilities are built around specialist units called cokers, which process the thick, heavy residual material left over after initial crude distillation — material that would otherwise be difficult to sell — and convert it into higher-value fuels such as diesel and jet fuel. To run these units efficiently, refineries need either heavy fuel oil imported from abroad, or crude grades that naturally produce large quantities of that heavy residual material.

Before the Hormuz closure, Middle Eastern exporters supplied significant volumes of heavy fuel oil to USGC refineries for exactly this purpose. That supply effectively disappeared after April. Venezuelan imports of heavy fuel oil have also increased, but have not made up the shortfall.

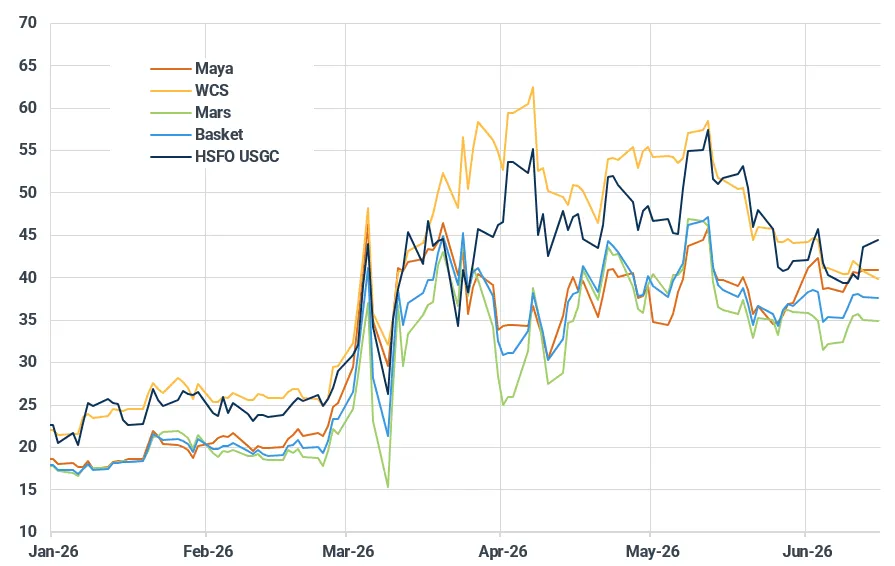

Venezuelan crude, however, addresses the problem differently. Dense, high-sulphur grades such as Merey — Venezuela's main export crude — naturally yield more of the heavy residual material that coker units need than lighter or sweeter alternatives. This means a refinery processing Merey produces more of the coker feedstock internally, reducing its dependence on imported fuel oil. Merey is also priced at a discount of around $4 per barrel to comparable Canadian crude grades, and can deliver similar or better diesel yields for refineries configured to handle it.

USGC conversion/coking margins by feedstock ($bbl)

Source: Kpler calculations based on Argus Media data

The economics of running heavy fuel oil through coking units have remained attractive since April, but refineries cannot capitalise on that opportunity without a reliable feedstock supply. Venezuelan crude provides that supply — and does so at a competitive price.

A Strait of Hormuz reopening will not immediately resolve the broader supply picture. Regional exporters face low inventories, the time required to rebuild throughput, and elevated domestic energy demand through the Gulf summer — all of which constrain how much they can export to the US in the third quarter. Middle distillate markets, meanwhile, will take months to normalise.

With US diesel and jet fuel inventories already low, seasonal gasoline demand rising, and refinery runs expected to stay high, Venezuelan crude will continue to underpin USGC refinery operations and help stabilise the supply of fuels that US Gulf Coast refiners depend on to meet both domestic and export demand

See why the most successful traders and shipping experts use Kpler