What’s sustaining the strength in US refinery runs?

US refinery utilisation is near multi-year seasonal highs (~90%), supported by light maintenance activity and wider heavy sour crude differentials. Improved heavy feedstock economics are incentivising higher run rates. While absolute refinery runs may ease later in 2026 due to planned closures and maintenance cycles, favourable margins should keep operating rates elevated.

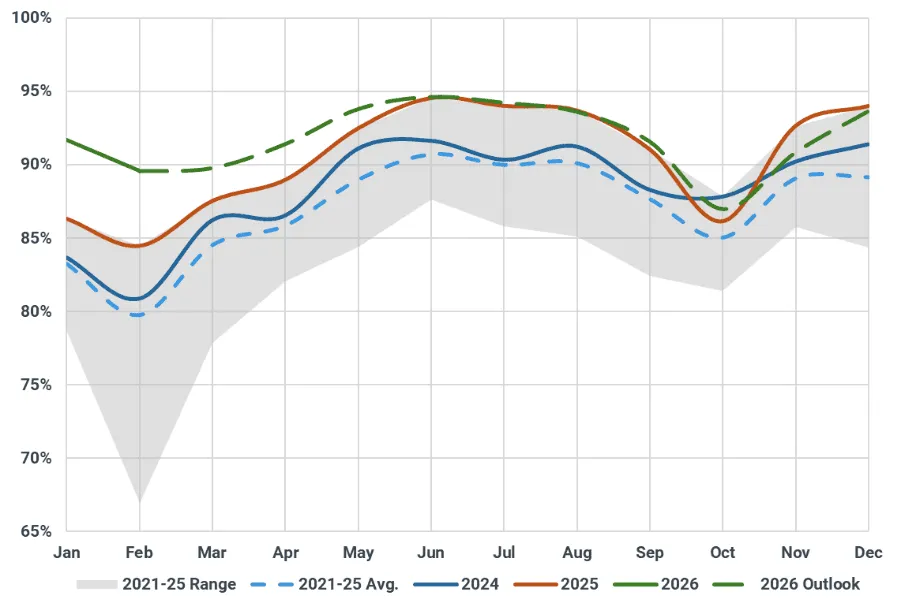

U.S. refineries are running at near peak capacity, with utilisation tracking at multi-year seasonal highs despite the closure of two major facilities last year. As per the latest EIA weekly data for Jan-26 and early Feb-26, US refinery capacity utilisation stood close to 90%, roughly 5 pp above typical seasonal averages, even after weather-related disruptions during the late-January cold snap.

US Refinery Runs Utilisation:

Source: Kpler

US refinery runs averaged 16.67 mbd in January, underpinned by light maintenance activity and generally stable operating conditions. The U.S. Gulf Coast has remained at the centre of this momentum, as reduced turnaround activity compared with prior years allowed refiners to sustain elevated run rates. Although Winter Storm Fern triggered a series of unplanned outages toward the end of Jan-26, causing a temporary dip in refinery runs, utilisation levels remained above historical averages. Favourable margins and disciplined operations have kept units running beyond seasonal norms.

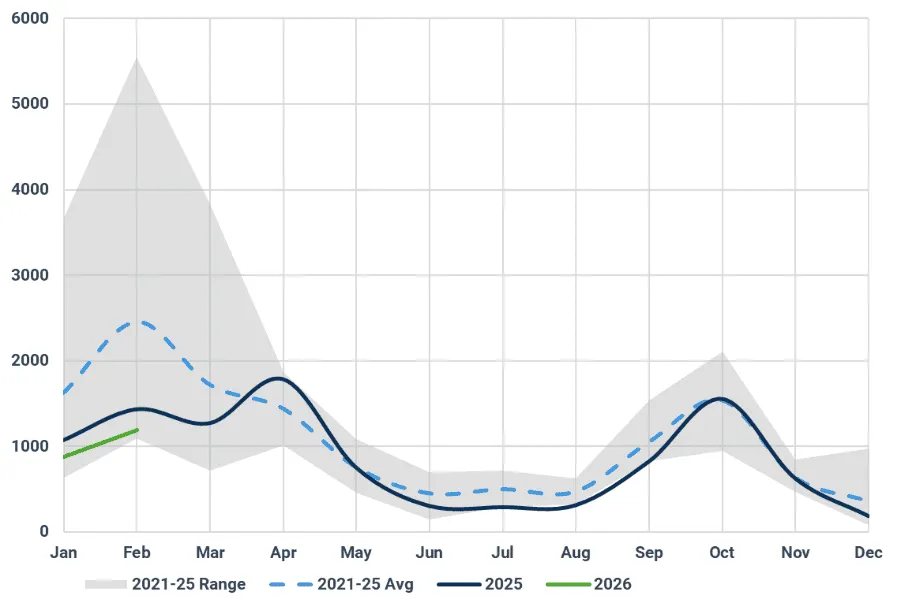

US Refinery maintenance Cycle in kbd:

Source: IIR

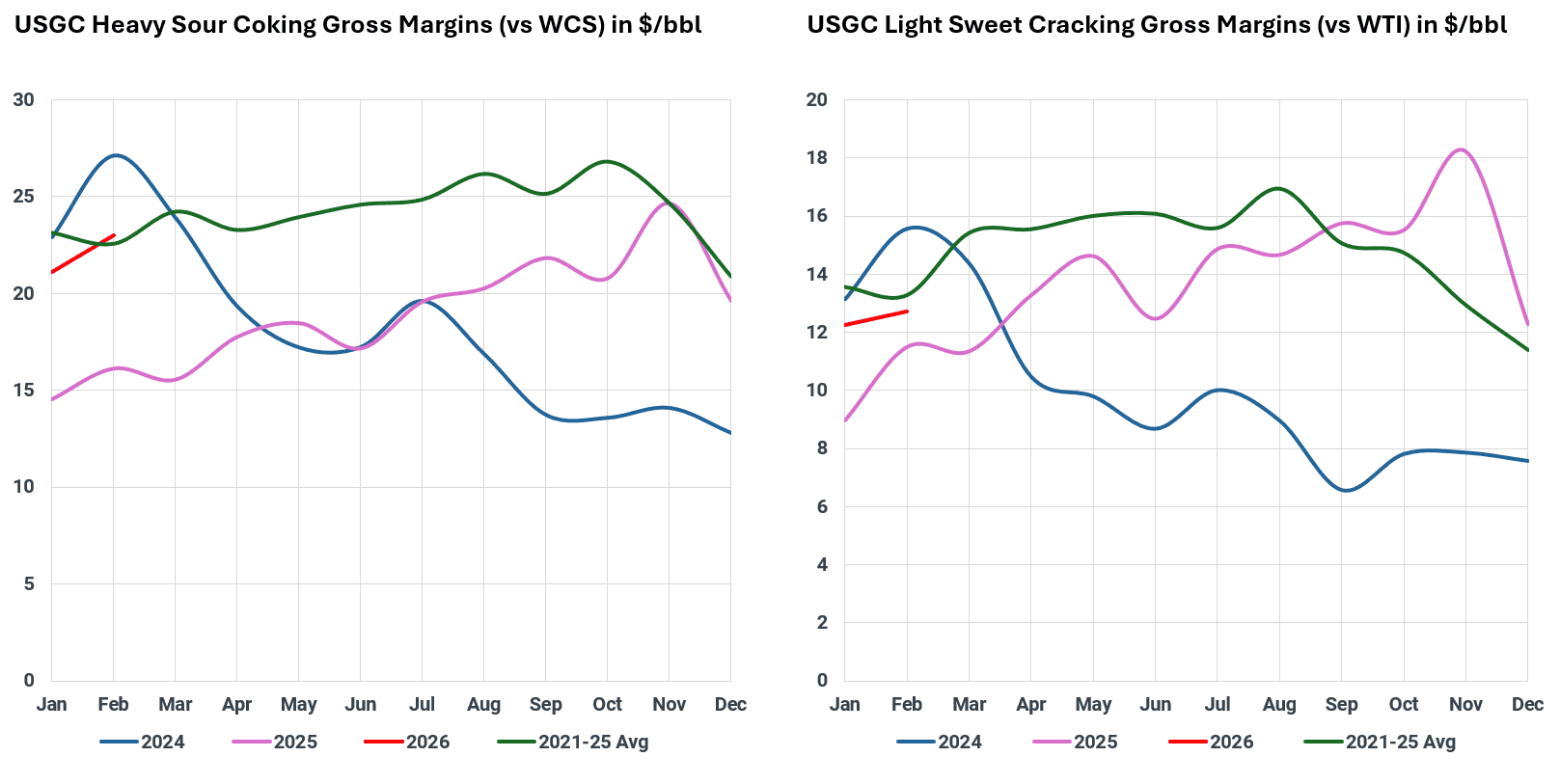

A second and equally important driver has been the movement in heavy sour crude differentials. Following geopolitical shifts and the return of Venezuelan crude into the open market, heavy sour grades have remained under pressure relative to light sweet benchmarks. Softer heavy sour crude pricing has materially improved feedstock economics for complex Gulf Coast refiners, whose coking configurations are designed to process heavier, heavy high-sulfur barrels. As a result, sour coking margins (vs WCS) have expanded to around $20/bbl in Q1-26 (QTD), compared with roughly $15/bbl during the same period last year, reinforcing incentives to maximise crude runs. Incremental Venezuelan heavy barrels have further supported this dynamic, with additional volumes increasingly directed toward complex USGC refining systems.

USGC Refinery Gross Margins in $/bbl:

Source: Margins are based on LP optimisation using Argus Pricing

The combination of lighter maintenance schedules and supportive heavy sour crude pricing has created a favourable operating environment, particularly for refiners with high conversion capacity. Even with reduced system capacity following recent closures, strong utilisation across the remaining assets has largely offset the loss of nameplate volumes.

Looking ahead, we expect US refinery runs in 2026 to ease modestly after Q1, partly due to the planned closure of Valero’s Benicia refinery. Further downside may emerge in H2 2026 as the industry enters its next maintenance cycle, following the heavy turnaround wave past seen in 2021–2023, with major refinery overhauls typically occurring every 4–5 years. This increases the likelihood of additional outages through H2 2026–2027. However, sustained desired feedstock (heavy sour crude) availability and Gulf Coast configuration advantages should support firm operating rates. With refining margins expected to remain healthy, utilisation level is likely to stay elevated even if absolute run volumes decline y/y.

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you to track critical crude oil market developments for your own analysis. Our precise forecasting empowers smarter trading and risk management decisions.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

.jpg)