China LNG demand downgraded as weaker Q4 industrial activity weighs on outlook

Kpler Insight has lowered its 2026 China LNG demand forecast by 0.2 mt to 63.5 mt, reflecting a weaker outlook for industrial gas demand in Q4. While industrial activity is expected to remain broadly stable through July-August, lower geopolitical risk premiums are expected to improve Middle East methanol availability into China, loosening the domestic methanol market. At the same time, weak downstream petrochemical demand, China's property downturn and persistent solar-sector overcapacity are expected to weigh on methanol- and glass-related gas consumption later in the year. As a result, Asian spot LNG prices are expected to remain broadly rangebound through Q3, supported by restocking demand and stable near-term industrial activity, before softening in Q4 as industrial LNG consumption weakens.

Market & Trading Calls

- China 2026 LNG Demand: Slight decrease, as China LNG demand forecast is lowered by 0.2 mt to 63.5 mt, reflecting weaker petrochemical- and property-related industrial gas demand in Q4, partially offset by broadly stable industrial activity during July-August.

- Asian LNG Prices: Rangebound for prompt prices, as stable industrial demand and continued restocking support prompt prices. Turn more bearish in Q4, as weaker petrochemical, glass and property-linked gas demand reduces industrial LNG consumption.

China's gas demand continued to weaken in April, with the National Development and Reform Commission (NDRC) reporting apparent consumption of 34.98 bcm, down 4% y/y and below expectations. Elevated Asian LNG prices following supply concerns around the Strait of Hormuz continued to pressure industrial gas consumption, and we estimate that May industrial gas demand declined by approximately 1.9 bcm y/y.

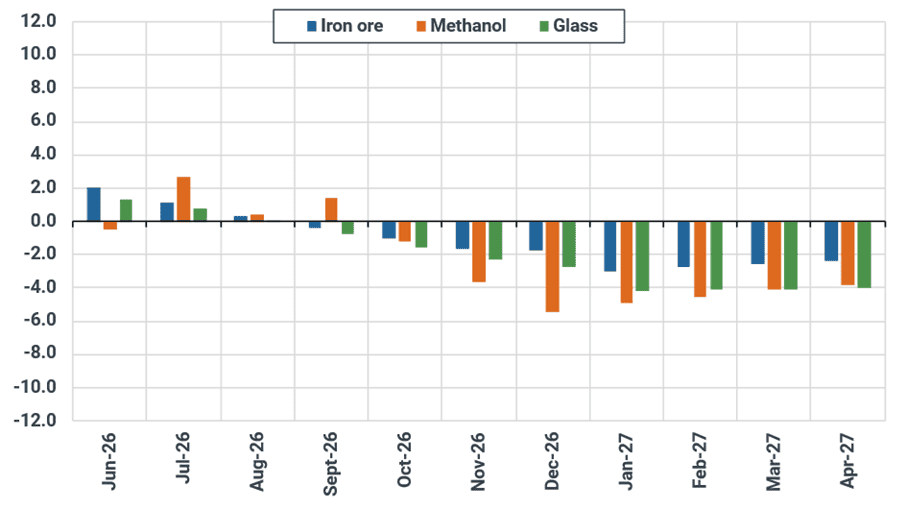

Kpler Insight's latest industrial tracker continues to point to broadly stable industrial activity through July-August before weakening in Q4 2026, driven by softer methanol- and glass-related activity. The latest tracker update, as of 26 June 2026, reflects deteriorating fundamentals across China's petrochemical, building materials and property sectors.

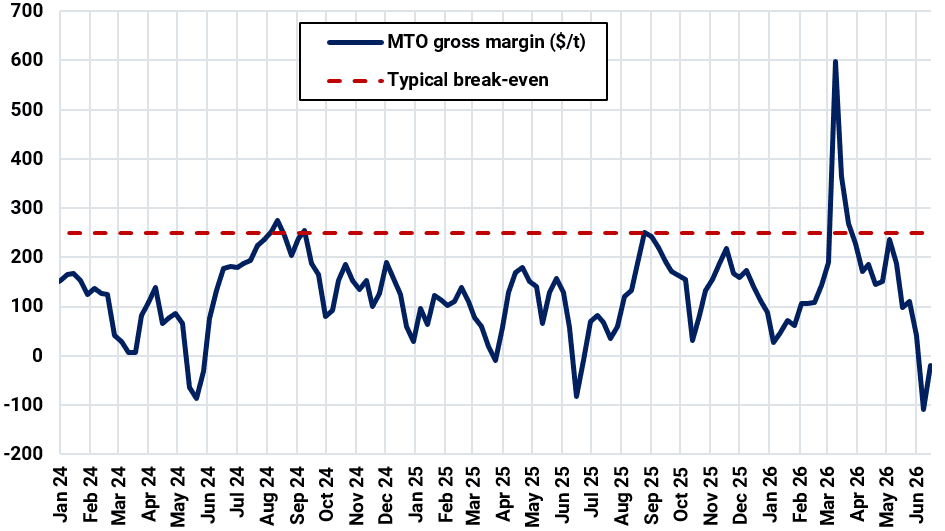

Methanol-linked activity is expected to remain broadly stable over July-August as methanol-to-olefin (MTO) economics have improved modestly after gross margins fell to -$108/t in early June. However, we expect this recovery to provide only limited support to domestic gas demand.

Lower geopolitical risk premiums following the US-Iran peace deal are expected to increase Middle East methanol availability into China, loosening the domestic methanol balance and weighing on local methanol production. At the same time, weak downstream petrochemical demand is likely to limit any further improvement in MTO margins, reducing incentives for higher operating rates and limiting additional gas demand from the sector.

Glass-related gas demand is expected to weaken in Q4 as China's property downturn and persistent overcapacity across the solar supply chain continue to reduce production incentives. Together, these trends are expected to weaken industrial gas demand later in the year, led by weaker petrochemical, property-related and solar-linked activity.

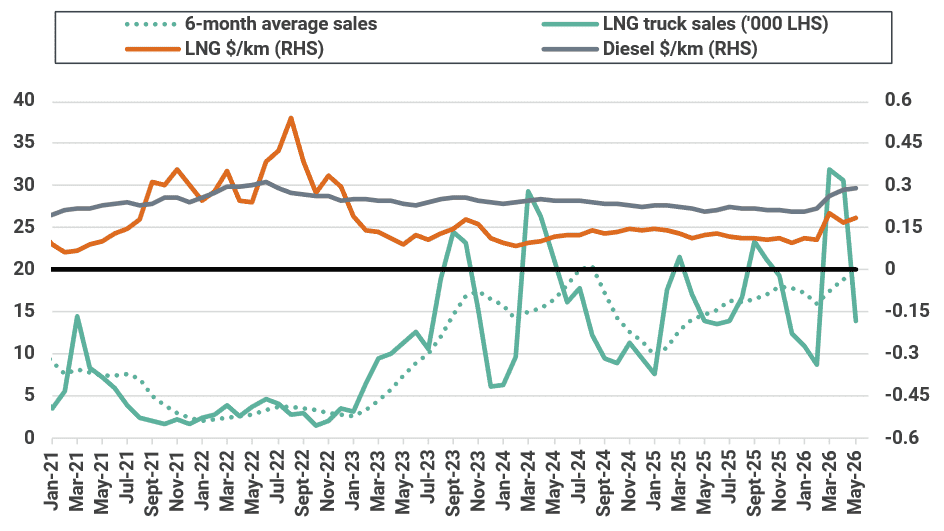

Transport-sector LNG demand has also begun to soften broadly in line with expectations. LNG truck sales fell to 13,900 units in May, broadly flat y/y but remaining above the five-year average. Although LNG retains a fuel-cost advantage over diesel, prices remain elevated in absolute terms, while electric heavy trucks continue to improve their cost competitiveness. We continue to expect LNG truck freight volumes and logistics intensity to decline into Q4, with slower LNG truck sales and lower fleet utilisation adding further downside pressure to China's LNG demand outlook.

Overall, Kpler Insight lowers its 2026 China LNG demand forecast by 0.2 mt to 63.5 mt. Asian LNG prices are expected to remain broadly rangebound through Q3 as continued restocking demand "offsets broadly stable industrial demand, before turning more bearish in Q4 as weaker petrochemical-, methanol- and glass-related LNG consumption weighs on prices.

Net change in industrial activity index between 1 June and 26 June 2026

Source: Kpler Insight. Note: Each sectoral industrial index is normalized to 100 as of 1 January 2024. Index values reflect relative activity trends, but the impact on gas demand varies by sector and is not directly proportional to index magnitude.

Chinese Methanol-to-Olefins gross margins ($/ton)

Source: Argus, Kpler Insight.

China monthly LNG truck sales (thousand trucks)

Source: CVWorld, Kpler Insight

China LNG heavy truck sales (LHS, ‘000 vehicles) and sensitivity to domestic diesel-LNG fuel economy spread ($/km)

Source: Eastmoney, Kpler Insight. Note: Diesel prices refer to domestic guidelines.

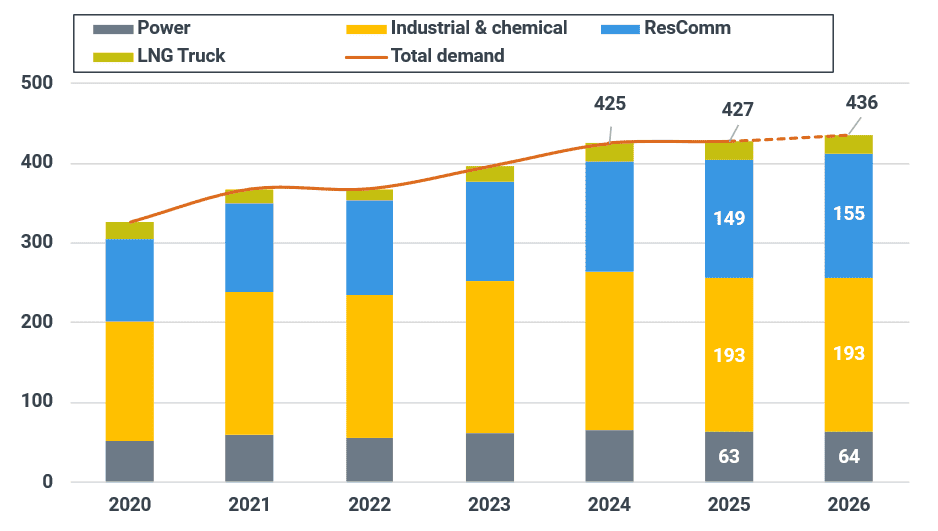

China’s monthly gas demand by sector (Bcm)

Source: NDRC, NBS, NEA, CEC, Kpler Insight

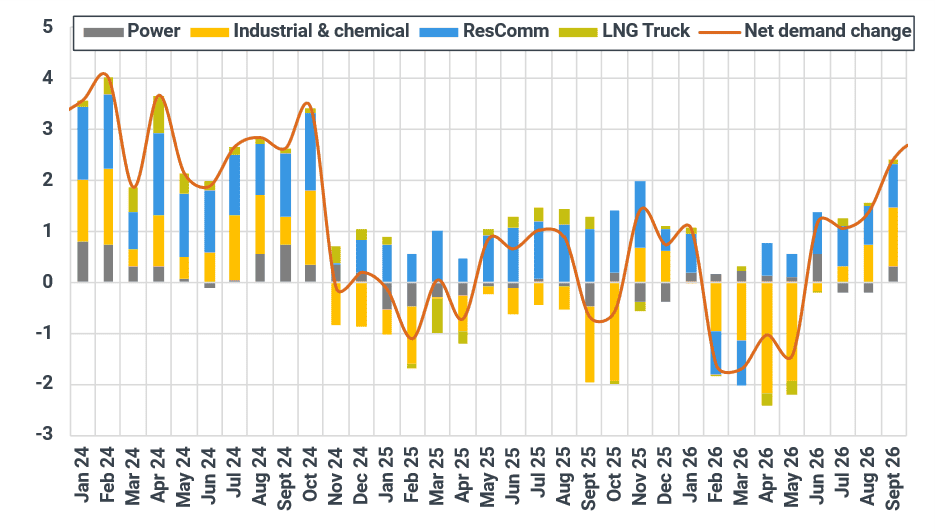

Year-on-year changes in China’s implied monthly gas demand by sector (Bcm)

Source: NDRC, NBS, NEA, CEC, Kpler Insight. Note: Historical and projected data are all in-house estimates.

See why the most successful traders and shipping experts use Kpler