El Niño to modestly lift China's wind generation, offsetting hydro weakness and capping LNG demand

China's latest renewable installation data showed slower renewable capacity additions following the introduction of market-based renewable power pricing. For 2026, LNG demand is driven more by renewable utilization than by installed capacity. Kpler Insight has lowered its 2026 wind and solar installation assumptions but still expects China to comfortably exceed the 15th Five-Year Plan (FYP) New Energy System Plan target of at least 2,700 GW of combined wind and solar capacity by 2030. Separately, the transition from La Niña to El Niño is expected to bring drier and breezier conditions during July-August, improving wind utilization factors before weaker rainfall feeds through to hydropower later in August-September. Stronger wind generation is expected to largely offset softer late-summer hydropower, reducing gas-for-power demand and prompting a marginal 0.1 mt downward revision to China's 2026 LNG demand forecast to 63.7 mt. The adjustment is too small to materially alter regional balances, leaving the outlook for prompt spot Asian LNG prices broadly neutral.

Market & Trading Calls

- China LNG demand forecast: Slight decrease, as stronger wind generation during July-August is expected to offset weaker late-summer hydropower, reducing gas-for-power demand and lowering Kpler Insight's 2026 LNG demand forecast by 0.1 mt to 63.7 mt.

- Asian LNG price: Stable in the prompt, as the 0.1 mt downward revision to China's LNG demand is insufficient to materially affect regional balances, leaving a broadly neutral impact on prompt prices.

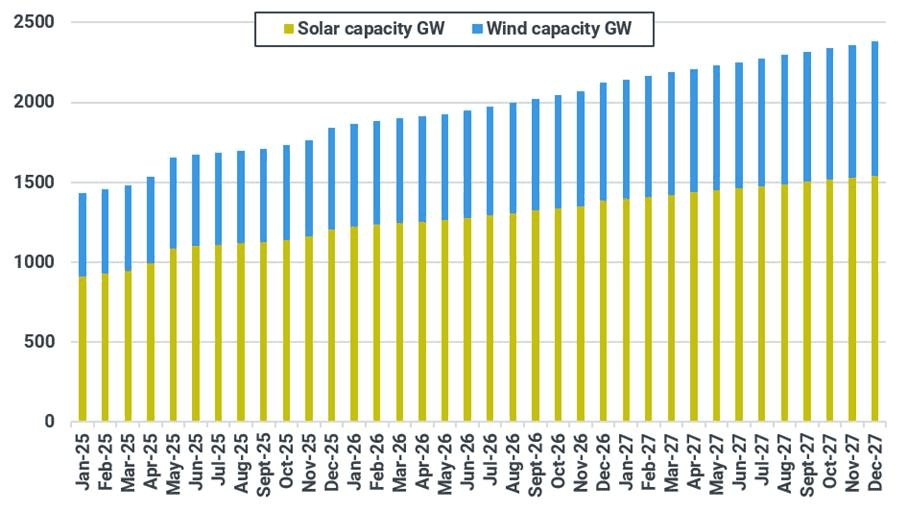

China's National Energy Administration (NEA) May 2026 data showed slowing momentum in renewable capacity additions. Solar capacity increased by 178 GW y/y (+16%) to 1,262 GW, while wind capacity rose by 97 GW y/y (+17%) to 665 GW, with solar's annual growth rate slowing to its weakest pace since November 2021. Hydropower capacity also increased by 14 GW y/y (+3.1%) to 452 GW. Meanwhile, total power generation rose by 56 TWh y/y to 866 TWh, supported by continued electrification across industry, commercial activity, and transport.

The slower pace of renewable installations reflects more cautious project development following the introduction of market-based renewable power pricing this year. In line with the weaker installation trend, Kpler Insight has lowered its 2026 solar installation forecast from 200 GW to 150 GW and its wind installation forecast from 120 GW to 90 GW. Despite these revisions, combined wind and solar capacity is still expected to increase by 240 GW y/y to 1,927 GW by end-2026.

The recently released 15th Five-Year Plan (FYP) New Energy System Plan targets total installed power capacity of 5,400 GW by 2030, with wind and solar accounting for more than 50% of total capacity. This implies at least 2,700 GW of combined wind and solar capacity by 2030. Even under our revised installation assumptions, China remains on track to reach nearly 2,900 GW by 2030, comfortably above the policy target.

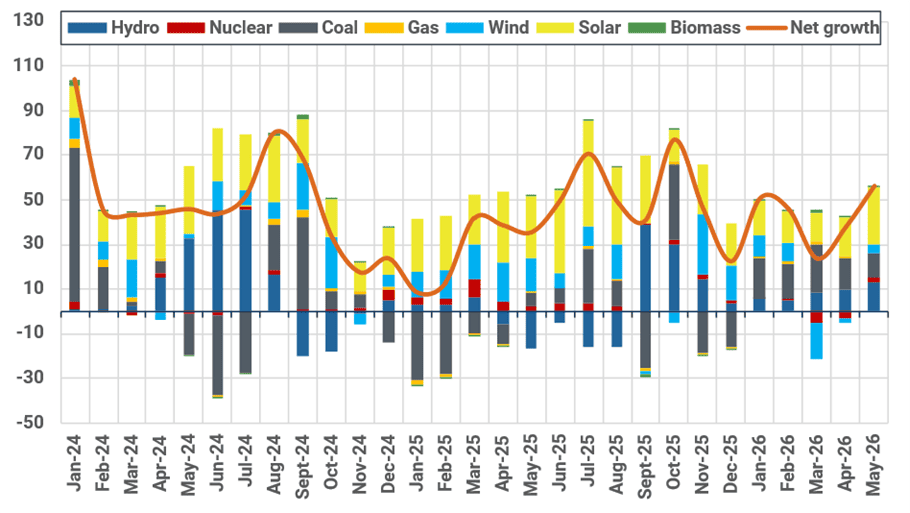

Within the generation mix, solar, wind, and hydro output increased by 25.4 TWh, 4.1 TWh, and 13.3 TWh y/y, respectively, continuing to displace thermal generation and leaving gas-fired generation only marginally higher at +0.6 TWh y/y. Looking ahead, CMA and ECMWF forecasts indicate drier and breezier conditions during July-August as La Niña fades and El Niño develops. Although July-August is typically China's seasonal low-wind period, ENSO-linked wind anomalies should modestly improve wind utilization factors in parts of North, Northeast, Southwest and South China. Hydropower weakness is expected to emerge later, with July generation still benefiting from strong May-June rainfall, while reduced precipitation is more likely to weigh on hydro output during August-September. Overall, stronger wind generation should largely offset softer late-summer hydropower, limiting peak-summer baseload gas-for-power demand.

The reduction in renewable installation forecasts has only a limited impact on 2026 LNG demand, as power balances this year are driven primarily by renewable utilization rather than incremental capacity additions. The slower pace of renewable deployment is therefore more likely to weigh on 2027 LNG demand than on 2026 balances. Reflecting stronger wind generation offsetting weaker late-summer hydropower, Kpler Insight has lowered China's 2026 LNG demand forecast by just 0.1 mt to 63.7 mt. The revision is too small to materially alter regional LNG balances, leaving the outlook for prompt spot Asian LNG prices broadly neutral. Upside risk remains limited unless wind generation materially underperforms forecasts or late-summer drought significantly deepens hydropower losses.

Historical power generation by fuel in China (TWh)

Source: NEA, NBS, Kpler Insight

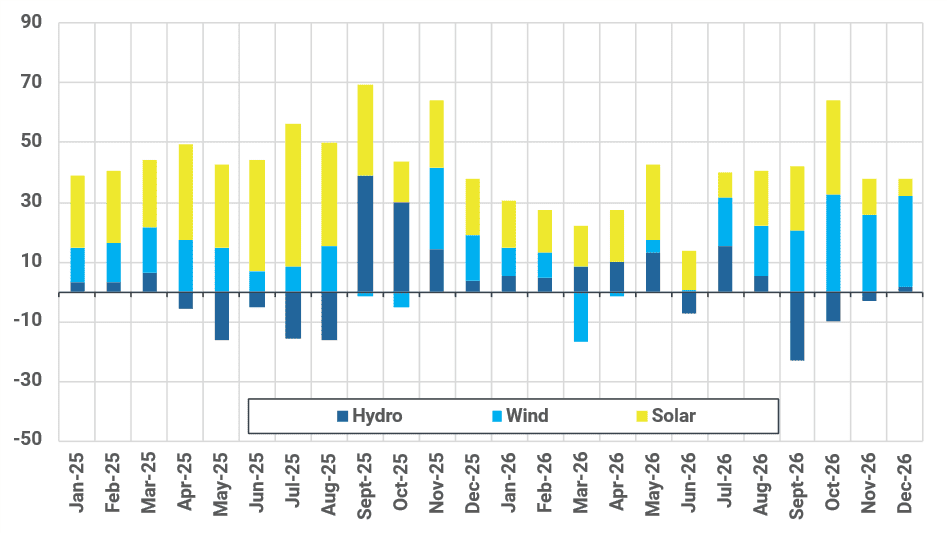

Year-on-year changes in monthly renewables generation by type (TWh)

Source: Kpler Insight. Note: Forecast period starts from June 2026.

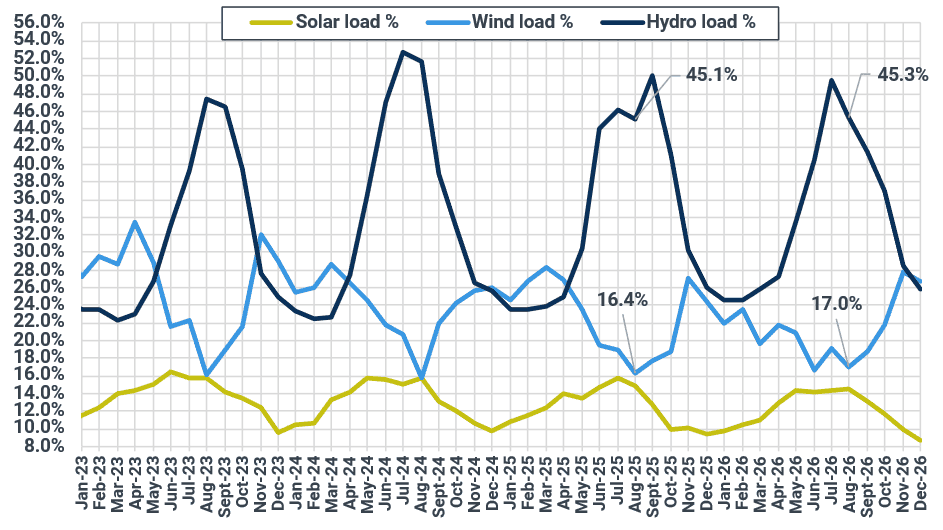

China’s monthly renewable power utilization factor by type (%)

Source: NBS, NEA, Kpler Insight. Note: Forecast period starts from June 2026.

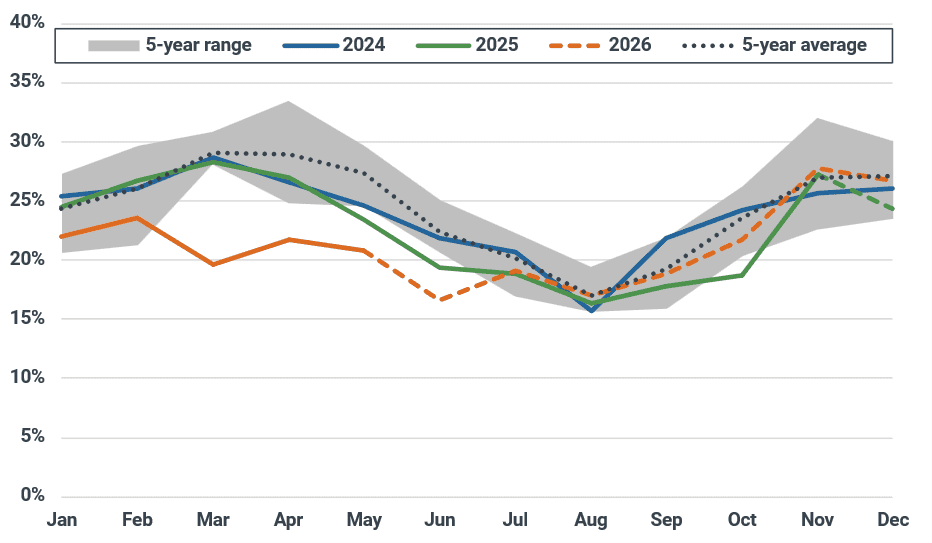

China’s historical and forecast monthly wind utilization factor (%)

Source: NBS, NEA, Kpler Insight. Note: Forecast period starts from June 2026.

China’s solar and wind installed capacity (GW)

Source: NEA, Kpler Insight

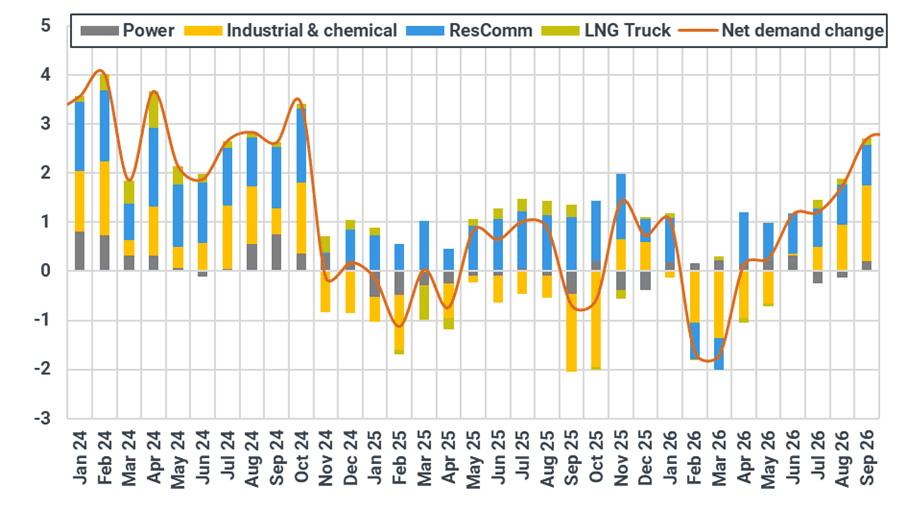

Year-on-year changes in China’s monthly sectoral gas demand (Bcm)

Source: Kpler Insight

See why the most successful traders and shipping experts use Kpler