Oil prices the glut, metals price the unwind

Crude extended its post-MoU rout as accelerating Hormuz transits and clearing stranded barrels pushed Dubai deeper into contango and Brent into the mid-$70s, with global balances seen tipping toward a Q4 surplus. Base metals suffered a violent systematic unwind — aluminium collapsed and trend funds flipped net short nickel and aluminium — even as a fresh round of semiconductor earnings reinforced the structural copper-demand case from the AI build-out. Precious metals reversed hard on a firm dollar. The week's lonely bids sat in Western refined products on Russian export-ban risk, European power on a heat-and-low-wind spike, and softs on weather-driven tightness, all against China's worst quarter on record. Hormuz normalization is now the dominant bearish force across crude and bulks, overwhelming a still-constructive copper demand narrative. Heat and systematic flows, not fundamentals, set the week's tone.

Market & Trading Calls

Crude — bearish Dubai, narrowing WTI–Brent. Accelerating Hormuz transits, stranded-barrel clearance and recovering Iranian loadings keep Dubai structure and the Brent–Dubai EFS under pressure toward an autumn surplus, with renewed vessel attacks in the MEG the key upside risk. Cushing near decade lows argues for a tighter WTI–Brent even as the wider complex de-rates.

Refined products — bullish middle distillates, neutral light ends. A mooted Russian export ban, ~2.5mbd of drone-driven CDU outages and low Rhine levels at Kaub skew gasoil risk higher, while Western gasoline stays supported by sub-range stocks and Mexican export pull. Naphtha and fuel oil remain capped as Hormuz normalization lengthens Asian balances.

Natural gas/power — bullish CWE, neutral TTF. Heatwave residual demand, weak wind and river-temperature nuclear deratings underpin French and German spot into Week 28, keeping CWE skewed bid. TTF is two-way: bearish fundamentals from high storage and recovering Atlantic LNG against a renewed MEG-attack risk premium.

Metals — bearish bulk and base near-term, constructive copper structurally. Systematic CTA liquidation and China's anti-involution squeeze keep copper, aluminium, nickel and coal pressured, with further sell triggers live below key levels. The semiconductor-led demand story remains the medium-term offset, but spot needs Chinese restocking to stabilize; precious stays vulnerable to the firm dollar despite steady central-bank buying.

Agriculture — bullish softs, bearish grains. Weather-driven tightness keeps cocoa, sugar and coffee bid, while ample supply and harvest pressure weigh on wheat and corn. The soy complex stays heavy on biofuel-policy uncertainty and the crude selloff.

Equities & macro — risk-off, semis the exception. China's record-weak quarter and a firm dollar cap risk appetite, with Bitcoin underperforming and Asian indices soft. Semiconductor strength is the lone structural bid; easing front-end yields offer only marginal relief.

Weekly Performance (Friday to Monday)

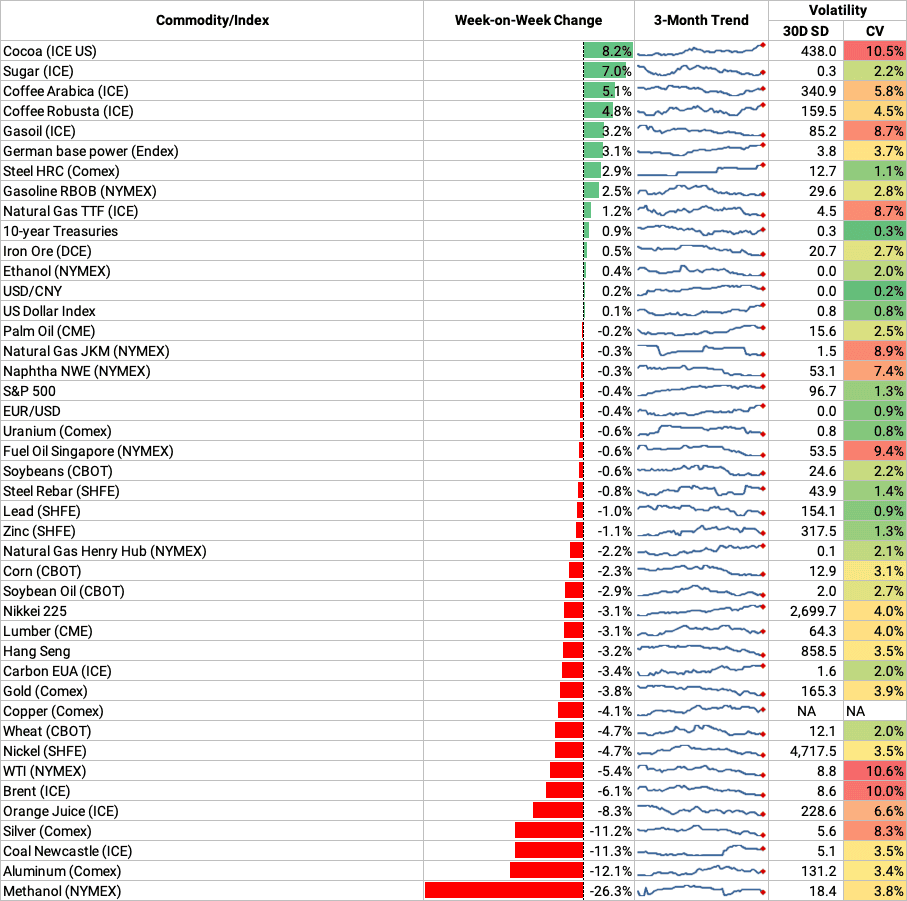

Crude fell hard again, with Brent −6.1% w/w to roughly $75.7/bbl and WTI −5.4%, extending the slide that began with the US–Iran MoU. Transits through the Strait of Hormuz accelerated to the highest daily count since the war began as stranded cargoes cleared the Gulf — non-Iranian crude on water inside the Gulf dropped to 64mb from 82.6mb — while Iranian loadings recovered above 840kbd under the 60-day waiver. The Dubai M1–M3 spread flipped into contango (−$1.12/bbl) from over $4 backwardation pre-deal, and a wide Brent–Dubai EFS (~$7) kept a rare westbound arb open, with Zakum landing in Italy. WTI was the relative exception: Cushing below 19mmbbl (a decade low) and national stocks slipping under the five-year range for the first time this year kept time spreads firmer.

Refined products diverged sharply, with gasoil +3.2% and RBOB +2.5% but naphtha NWE −0.3% and Singapore fuel oil −0.6%. Middle distillates firmed on Atlantic supply risk — Novak flagging a possible Russian export ban, Ukrainian drone strikes pushing ~2.5mbd of CDU capacity offline, low Rhine water at Kaub, and the 30 June fuel-tax expiry. Western gasoline cracks strengthened (USGC +$4.55/bbl, RBOB +$5.30/bbl w/w) on sub-range inventories (~5% below the five-year average) and Mexican pull, while US jet output hit a record 2.2mbd at a record 12.9% yield. Naphtha and fuel oil lagged as Hormuz normalization lengthened Asian balances.

Natural gas and power were led by European power, with German base power +3.1%, TTF +1.2%, JKM −0.3% and Henry Hub −2.2%. CWE spot ran on a heatwave (3–5°C above seasonal), a sharp wind collapse and French nuclear river-temperature deratings, with up to 6.5GW potentially affected across Blayais, Bugey, Golfech, Nogent and Saint-Alban. TTF eked out a gain as renewed MEG vessel attacks revived supply concerns (gas to €42.4/MWh), offsetting bearish fundamentals — storage at 47.2% and recovering Atlantic LNG. JKM softened but stayed underpinned by stronger Korean restocking (forecast lifted 0.6mt to 47.0mt) and weak Chinese domestic output; Henry Hub eased on profit-taking despite the US heat.

Metals were gutted by a systematic unwind: copper −4.1%, aluminium −12.1%, nickel SHFE −4.7%, coal Newcastle −11.3%, with steel HRC +2.9% and iron ore +0.5% the rare green. Trend-following CTAs sold 430kt across base metals on 24 June (after 200kt on the 23rd), copper accounting for two-thirds, and flipped net short LME nickel and aluminium for the first time since late 2025. China's anti-involution drag (manufacturing investment −0.4% y/y, retail sales −1.8% y/y) compounded the selling. The structural counterpoint — record semiconductor earnings and the AI/data-center capex wave deepening copper intensity through electrification, grid and cooling demand — was simply overwhelmed by flows. Precious reversed violently, silver −11.2% and gold −3.8% as the firm dollar and hawkish Fed bit and the deal's relief bid faded.

Agriculture was carried by softs, with cocoa +8.2%, sugar +7.0%, arabica +5.1% and robusta +4.8% all surging on weather-driven supply tightness. Grains slipped on harvest pressure and ample stocks (wheat −4.7%, corn −2.3%), while the soy complex stayed heavy (soybean oil −2.9%) on biofuel-policy uncertainty and the crude selloff. Orange juice −8.3% was the standout loser.

Equities and macro carried a risk-off tone: S&P −0.4%, Nikkei −3.1% and Hang Seng −3.2%, with the dollar broadly stable (DXY +0.1%, EUR/USD −0.4%) and ten-year Treasuries firmer as oil disinflation nudged yields lower. Semiconductor earnings were a structural bright spot, but MSCI China headed for its worst quarter on record versus global benchmarks, weighed by anti-involution, anemic consumption and a strained 4.5% growth target. Bitcoin continued to underperform amid the firmer dollar and broader de-risking.

Weekly Performance

Source: Marketview

See why the most successful traders and shipping experts use Kpler