Refining margins to remain supported through H2 as product supply lags crude flows

As crude markets continue to normalise, the focus is increasingly shifting toward refined products. While crude availability is expected to improve over the coming months, refined product supply is likely to recover more slowly, leaving refining margins healthy through H2

Several structural factors underpin this view.

1. Product supply is likely to recover more slowly than crude supply

While crude availability is expected to improve over the coming months, refined product supply is likely to respond with a meaningful lag.

Several factors support this view:

- The Middle Eastern refinery ramp-up will take time. Although refining capacity is coming back online, reaching stable operating rates and establishing export flows is unlikely to happen immediately. We expect the ramp-up in refined product exports to take another 3–4 months, and potentially longer for some assets.

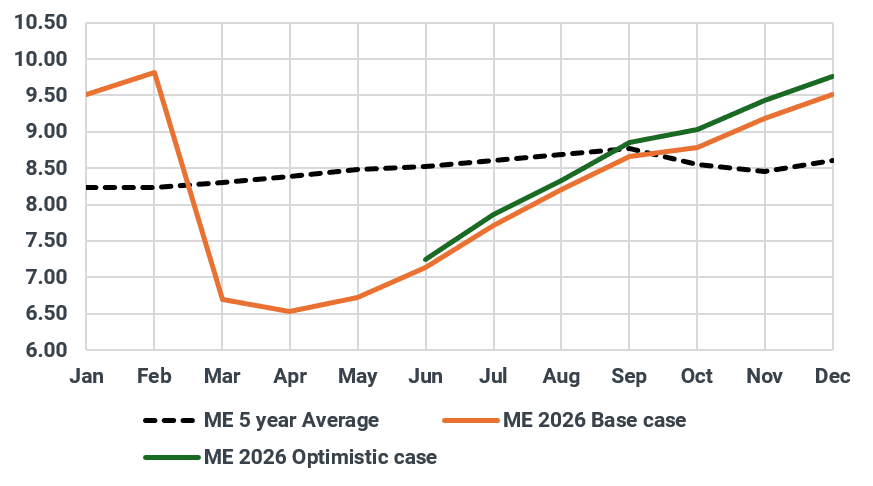

Middle East refinery runs (kbd)

Source: Kpler

- Russian downstream remains structurally constrained. Russian refinery runs have fallen to multi-year lows at 4.1 Mbd in June and are expected to be running around 4.4-5.0 Mbd over July-September, following repeated infrastructure attacks and extended repair work (particularly the recent Moscow refinery attack, where repair works are said to last six months). Even if attacks moderate, residual maintenance requirements are expected to keep refinery throughput markedly below historical levels through H2, limiting incremental product supply.

- China is unlikely to act as the swing supplier. Chinese refinery runs remain subdued at least until August, based on existing programs, with crude imports near decade lows and refined product export quotas continuing to constrain export growth and keep refinery runs in check.

- Autumn maintenance will further tighten supply. Refiners across the US, Europe and India deferred or minimised spring maintenance to maximise utilisation. This points to a heavier-than-normal turnaround season during Q4, reducing refinery throughput just as seasonal maintenance peaks.

- Product inventories. Refined product inventories across the main hubs, including the US (gasoline and diesel), Singapore, Fujairah and ARA, remain relatively low. Limited inventory buffers reduce the market's ability to absorb refinery outages, weather disruptions, unexpected outages, or demand strength, increasing the likelihood of stronger price responses to supply shocks.

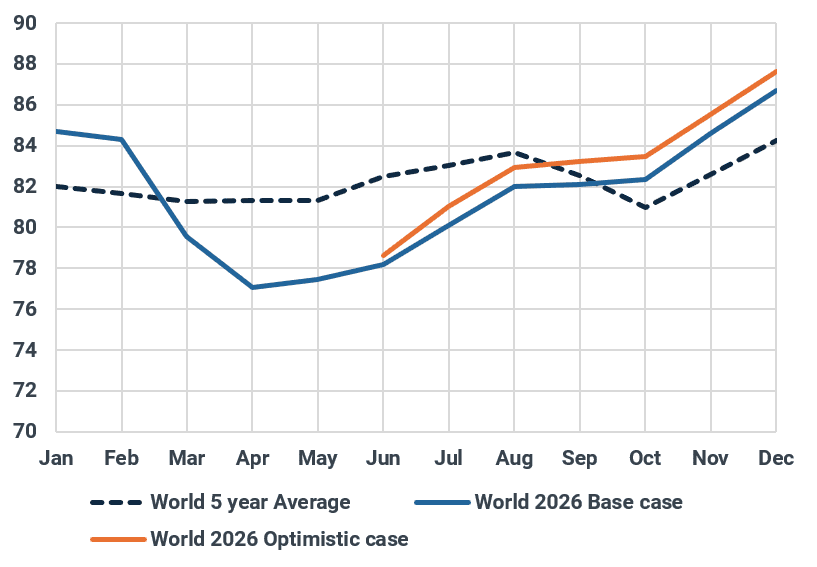

- Refinery runs creep. Our current base case assumes global refinery runs average around 81.5 mbd in Q3, rising to around 84.5 mbd in Q4 as crude availability improves and seasonal maintenance winds down. There is, however, an upside to this outlook. Healthy refining margins should encourage refiners with operational flexibility to maximize utilisation. In our optimistic case, capacity creep and higher utilization at existing refineries—particularly in the US, India and parts of Asia—could add a further 700–900 kbd of global refinery runs above our base case.

Taken together, these factors suggest crude markets are likely to normalise faster than refined product markets. While additional crude barrels become available, the supply response in diesel, jet fuel and gasoline is expected to lag, supporting healthy refining margins through H2.

Global Refinery runs (kbd)

Source: Kpler

2. Refinery optimization becomes increasingly important through H2

The outlook for refining margins will not be determined solely by refinery utilization, but also by how refiners choose to optimize their product slate.

During Q2, exceptionally strong middle distillate cracks and the comparison to gasoline encouraged many refiners, particularly in the US and Europe, to maximise jet fuel and diesel production at the expense of gasoline. As we move into Q3, refinery optimization becomes more balanced. Gasoline balances, particularly in the US, have tightened considerably following strong seasonal demand, while the middle distillate premium has moderated from the exceptional levels seen during March and Q2. The mid-September shift to winter-grade gasoline should modestly improve gasoline supply by increasing blending flexibility and yields.

However, we do not expect this to materially alter the broader H2 outlook. Russian refinery disruptions continue to constrain diesel exports, Middle Eastern refinery ramp-ups will take time to materially increase middle distillate exports, and the heavier turnaround season across the US, Europe and Asia during Q4 is likely to further limit middle distillate supply growth. As a result, refinery optimisation is likely to become more balanced through Q3 before the market once again tilts in favour of middle distillates during Q4.

3. Russian export policy remains an upside risk for middle distillate margins

Russian refinery runs remain near multi-year lows, limiting middle distillate production and exports. Russia has already demonstrated a willingness to intervene in product markets through export restrictions to protect domestic supply. While a prolonged blanket ban on diesel exports appears unlikely given logistical constraints, any tightening of export policy or operational disruptions that reduce diesel exports would further tighten middle distillate balances. Although this is not our base case, it remains an important upside risk for diesel cracks through H2.

Market implication

The normalisation of crude markets does not imply a similar normalisation in refined products cracks and refining margins. Lower crude prices, delayed product supply growth, elevated turnaround risks, constrained Russian refinery operations, resilient transportation fuel demand and relatively low product inventories all point toward a constructive refining margin environment through H2.

While margins are unlikely to revisit the extreme highs observed during previous supply shocks, we expect them to remain healthy through Q3 and Q4 as refinery maintenance peaks and middle distillate balances tighten. Indeed, in our base case, transportation fuel (gasoline, jet/kero, and gasoil) balances average around -400 kbd in Q3, compared with a surplus of roughly +700 kbd in Q3 last year. The deficit is expected to widen to around -500 kbd during October–November before gradually recovering in December. This reflects refinery run growth that remains constrained relative to the expected increase in global crude supply availability.

Note: Refined product balances are scheduled to be updated in the Terminal on 7 July based on our latest base-case assumptions

Market insights you can trust

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler