The unsanctioned supply paradox – what could lie ahead for crude markets

The global crude oil market is currently fixated on the acute supply shock driven by the US-Israeli military campaign against Iran and the de facto closure of the Strait of Hormuz, which pushed Brent prices consistently above $100/bbl. However, this crisis is also increasing the likelihood of a curious shift. The world could end 2026 with Venezuelan, Iranian and Russian oil all either unsanctioned (or subject to loose enforcement), a prospect that seemed unthinkable at the start of this year.

Key Takeaways

- Geopolitical normalization could trigger a synchronized release of Venezuelan, Iranian, and Russian crude into an already structurally oversupplied market by 2027.

- Venezuelan output is aggressively recovering, targeting near 600kbd growth on the year to 1.3 Mbd

- An estimated 55 Mbbls of Iranian oil currently in floating storage could flood the physical market immediately upon sanctions relief

- Repeated US waivers have permanently eroded secondary sanctions barriers, expanding the Asian buyer base for discounted Russian crude.

- Trade Recommendation: Building a shorter position into H1 2027 (or buying put options) to plan for a retrace towards pre-war structural price around $60/bbl

Before the Iranian conflict, the market was forecast to face a surplus of near 2 Mbd, the largest since the Covid-19 pandemic. The geopolitical realities from January (Maduro capture) and the prospect of a Memorandum of Understanding between the US and Iran could lay the path materially lower again for price. This piece examines the three ‘sanctioned’ entities.

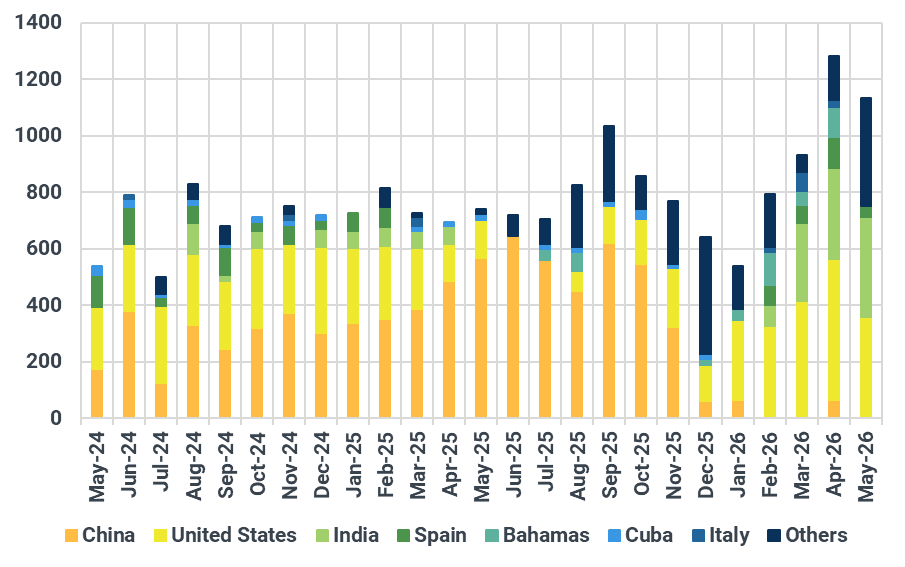

Venezuela: Venezuela’s crude output recovery is no longer speculative. Production recovered swiftly after the capture of President Maduro and the US naval blocked, and reached roughly 1.25 Mbd this month. Following political shifts in Washington and the issuance of new operating licenses, output has responded quickly, especially in the face of the war, and is trending toward 1.5 Mbd by 2027. Crucially, this extra-heavy, high-sulphur crude competes directly with Iranian and Russian barrels for Asian and US Gulf Coast refinery demand, applying severe downward pressure on heavy-sour differentials.

Venezuela crude exports by destination country, kbd

Source: Kpler

Iran: The current Brent premium contains the indefinite removal of Iranian barrels. As the conflict drags on, further pressuring the US, the move towards a memorandum of understanding (MoU) is increasing. With it brings a growing likelihood of sanctions relief on Iranian oil. The immediate bearish catalyst is the estimated 150 Mbbls of Iranian oil on water. A waiver would release this massive inventory in a compressed window, driving intense deflationary pressure on spot prices and the forward curve. Furthermore, a quick influx of money into the country could support oil production, which could move back towards the 4 Mbd mark next year as well (currently sitting at 2.7 Mbd due to the US naval blockade).

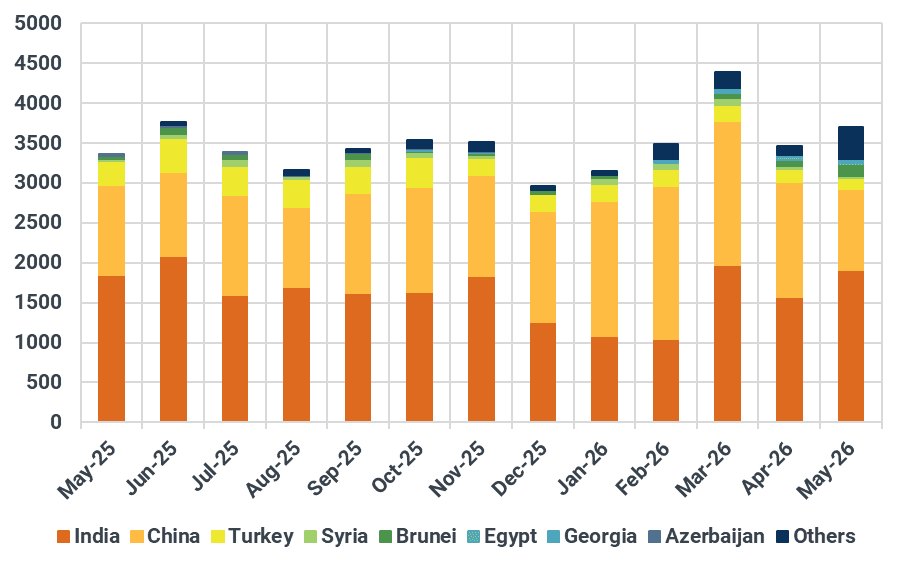

Russia: While Russia has not been formally unsanctioned, repeated US Treasury waivers issued in early 2026 to ease market tightness have permanently altered buyer behaviour. By effectively overriding the G7 price cap, these waivers have validated Russia's shadow fleet and eliminated the psychological and compliance barriers for Asian buyers. Russian crude is now flowing freely to a broader buyer base, including new entrants like Indonesia and the Philippines, securing a larger addressable market even if official waivers lapse. Russian exports have held steady at around 3.5 Mbd even in the face of Ukrainian drone attacks.

Imports of Russian crude by country, kbd

Source: Kpler

However, there are significant and very plausible scenarios that disrupt this bear case, including the damage to Iranian infrastructure and how elusive a robust deal with Iran might be.

Iranian South Pars condensate output has been cut by Israeli strikes, and full restoration of supply requires significant capital.

Perhaps more crucially, finding a robust deal that the market can trust is perhaps the biggest challenge to the bear case. The White House has today said any information about an MoU is a ‘complete fabrication’, suggesting that the collapse of any talks prolongs the wider tightness linked to the closure of the Strait of Hormuz.

Market insights you can trust

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler