China’s ethane demand back on track, but upside to US prices capped

Despite no official announcement from the government, following reports that China has exempted US ethane from tariffs, we have revised our demand forecast largely inline with our pre-tariff estimates. It remains unclear if China will also grant US polyethylene or LPG exemptions but with China looking to become self-sufficient in base chemical and plastics production and alternative non-US propane available (for a premium), both products are less likely to receive exemptions the immediate future.

Market & Trading Calls:

- Bullish Chinese ethane demand, imports going forward with US-origin ethane returning to the top of the petchem feedstock pecking order

- Bullish USGC ethane ratios, spreads to Henry Hub m/m in May as largest import market returns to the fold

- However, current tariffs weighing on petchem demand, no word yet on US polyethylene imports and rising field output means US ethane ratios to natural gas will remain capped through May

- Early indications in China of slowing plastic production and finished goods orders combined with meagre government stimulus measures will weigh on petchem demand growth through Q2

We have revised our Chinese ethane demand forecast upward since last month, as our base case now anticipates China will officially exempt US-origin ethane from its 125% tariff regime, following reports earlier in the week that multiple ethane-cracking operators reliant on imports were informed by officials that ethane would be exempted.

Our previous view anticipated that China would scale back tariffs on US imports by H2 July. As such, our most significant revisions relate to May-July time frame, as China’s higher tariff rate was due to kick-in from mid-May and Chinese buyers had stockpiled barrels in March.

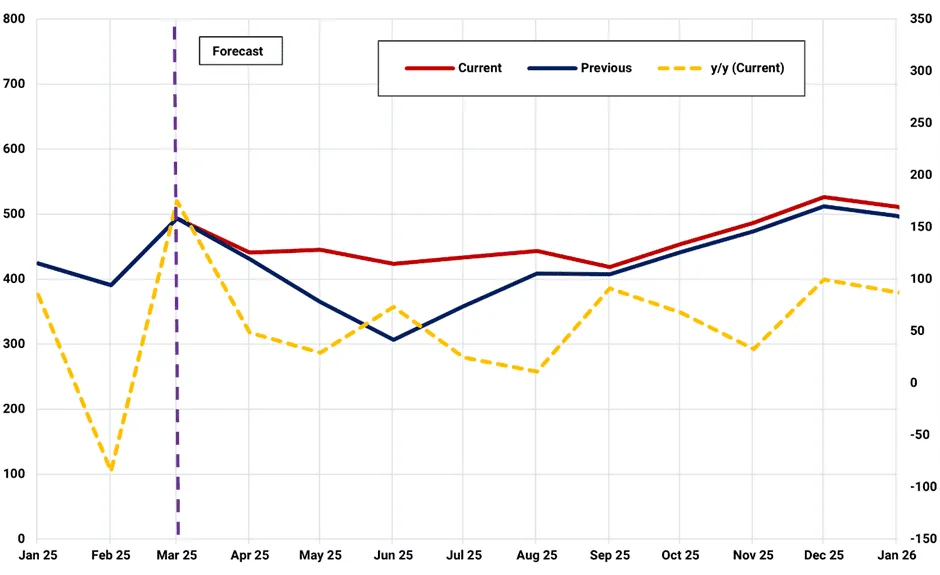

We now expect China’s ethane demand will rise by 43 kbd y/y in May-July to 434 kbd, a 91 kbd upward revision from our H1 April estimates. China’s ethane demand will grow by 55 kbd y/y to 448 kbd in 2025 with two new flexi-crackers and one conversion of a propane cracker doing the heavy lifting y/y, especially from September onward once new plants reach full-rates and additional VLECs are delivered allowing more US ethane to be imported.

Chinese ethane demand (kbd)

Source: Kpler derived data

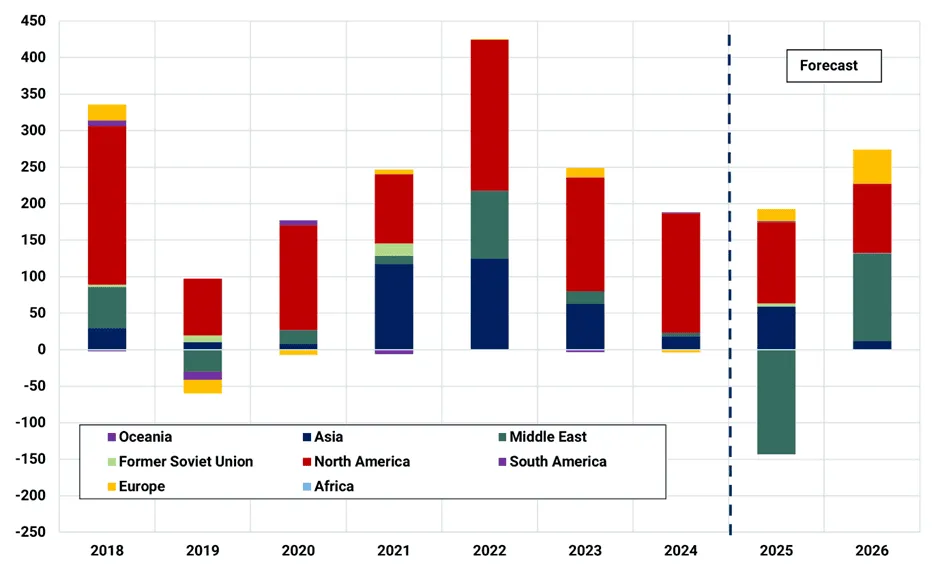

Ethane demand by region, y/y (kbd)

Source: Kpler derived data

By exempting ethane, China will weaken spot naphtha demand as prior to the likely exemption, we expected flexi-crackers in the country to maximise naphtha to avoid costly propane and ethane and to help fill the olefins gap left by ethane crackers and PDH plants lowering runs.

However, with propane less likely to receive an exemption in the immediate future, this still leaves tightening propylene markets (until late-Q2) from lower PDH runs supportive of domestic naphtha cracking, albeit much less than previously anticipated, especially in light of falling manufacturing data in China for April as US goods orders dry up. Meanwhile, outside of China, we maintain our view that flexi-crackers will favour LPG as dislocated US barrels are forced to clear into alternative markets.

Northeast Asian gross complex steam cracking margins per ton of ethylene ($/t)

Source: Kpler calculations using Argus Media prices

Reports of easing tariffs on US ethane has helped to lift prices in the US this week after they fell significantly m/m in April due to China’s position as the largest importer of waterborne ethane, falling back inline with the five-year average.

Ethane Mont Belvieu Enterprise average monthly spot price ($/t)

Source: Kpler calculations using Argus Media prices

However, China is net short ethylene and key grades of polyethylene (PE), of which the US is also net long. With so much additional steam cracking capacity ramping up in China (and Indonesia) this year and tariffs weighing on plastics consumption (reducing Asia’s net short ethylene and PE position), if China refuses to exempt PE imports, US sellers will struggle to place ethylene and derivatives into alternative markets, weighing on USGC cracking margins and demand. This, and our expectation that US ethane output will continue to grow through the rest of Q2, will help stop US ethane prices from moving above the five-year average for May.

Select Asian steam cracking capacity additions, 2024-2025

Although Europe is the natural alternative market to adsorb surplus US output in the short term, especially amid cracker closures in the region, local plants in Europe will be able to better compete with imports amid cheaper US LPG over the coming weeks combined with buyers being put off purchases in recent months by higher ratios of ethane in US-origin ethylene cargoes (Argus).

USGC gross complex steam cracking margins ton of ethylene ($/t)

Source: Kpler calculations using Argus Media prices

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts. Our precise forecasting empowers smarter trading and risk management decisions - backed by the most accurate oil price predictions two years running.

Unbiased. Data-driven. Essential.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Expert research & analysis driven by proprietary data

.jpg)