July 9, 2025

Dry bulk earnings diverge as Capesize weakens and smaller segments hit multi-month highs

Iron Ore & Steel: Iron ore prices pick up despite supply increases and steel sector softness

- Global seaborne iron ore exports climbed to a 12-month high of 149.20 Mt in June, following a typical seasonal pattern despite supply disruptions from smaller exporters such as Peru and Iran. The surge was driven by record shipments from Australia, where BHP loadings posted all-time highs. Other miners also increased output ahead of quarter-end, bringing total Australian exports to 88.60 Mt. However, following the June loading rush, global exports will decline to multi-week lows in early July.

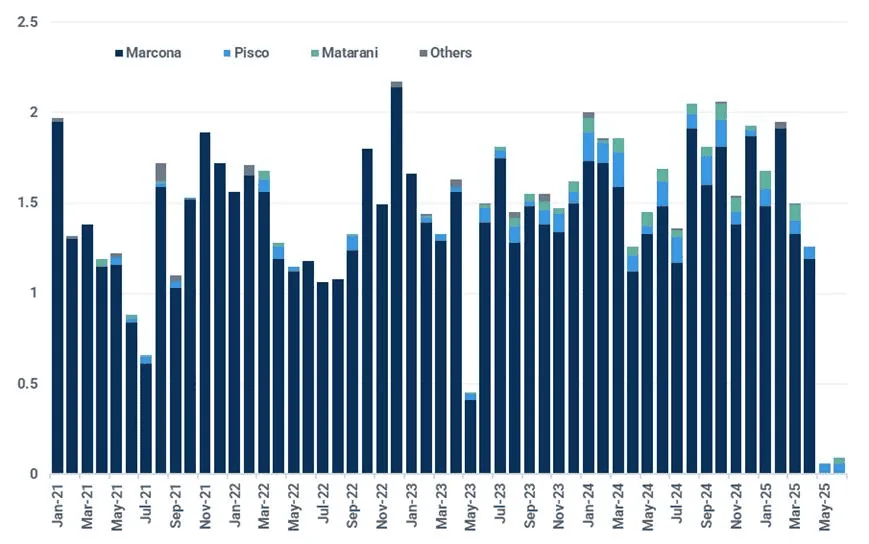

- On 28 June, Shoughan Hierro Peru (SHP) confirmed the completion of the repair of the shiploader at Marcona port, 96 days ahead of schedule. Before the announcement, Kpler had already reported that a much earlier than expected restart could happen in the Weekly and Monthly Reports after identifying vessels on route to Marcona. This week, we confirmed the Glovis Advance, currently berthed at Marcona, will soon depart for China’s Caofeidian carrying 170,000 tonnes of iron ore, suggesting a full resumption of operations may not be far.

- On the demand front, Chinese seaborne iron ore imports totalled 25.20 Mt in the week ending 29 June, down from a seven-month high of 26.70 Mt in the previous week but well above the five-year average of 23 Mt. Nonetheless, rising imports in July are occurring alongside mounting pressure on steel output, potentially result in higher stock levels.

- The China Iron and Steel Association (CISA) has urged Beijing to curtail the export of steel billets, a semi-finished product whose shipments rose by 306% y/y to 4.72 million tonnes in the first five months of the year. CISA criticised the trend as a “waste of China’s steel processing capacity”, “intensifying low-level competition” and “helping to push up the iron ore prices”.

- Iron ore prices rose in line with steel after a high-level policy meeting on 2 July in China boosted sentiment. President Xi called for measures to “regulate disorderly low-price competition” and “promote the orderly exit of outdated production capacity”—comments interpreted as signalling further output cuts. The SGX TSI 62% Fe second-month contract rose 2.60% w/w to a three-week high of $95.15/t on 2 July, while the most traded September 2025 contract on DCE closed 2.85% higher w/w at 722.50 yuan/t ($100.83/t). Nonetheless, underlying fundamentals do not support a sustained rally; supply is increasing while demand softens.

Iron ore exports from Peru’s Marcona are set to resume in July (Mt)

Source: Kpler

Key Dry Bulk Market Developments

Source: Kpler

Dry Bulk Port Congestion

Source: Kpler

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts. The full report is available within Insight and contains:

- Iron Ore & Steel: Iron ore prices pick up despite supply increases and steel sector softness

- Coal: The Thermal market remains in a trough, met coal recovery continues

- Grains & Oilseeds: Bargain buying, weather and deal anticipation lifts grain markets from recent lows

- Minor Bulks: Guinea announces new measures to tighten control on its bauxite sector

- Dry Bulk Freight: Stronger grains chartering puts sub-Capesizes in brighter spot

- Key Dry Bulk Market Developments

Unbiased. Data-driven. Essential.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Request a demo

Expert research & analysis driven by proprietary data

Request access

.jpg)