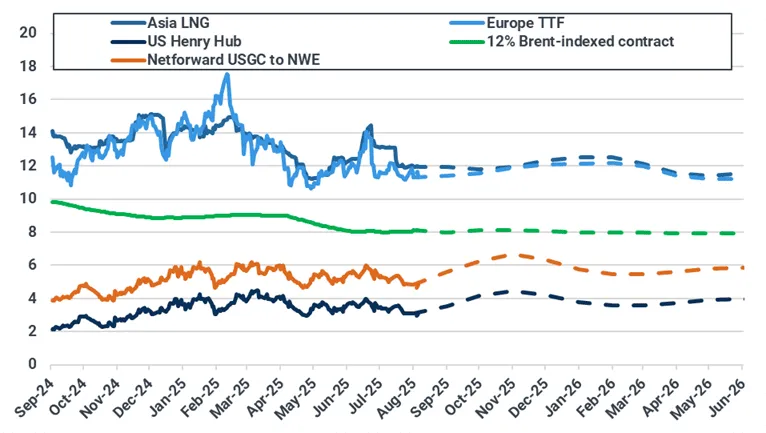

Mixed global gas price signals: bearish sentiment in Asia, stable TTF and Henry Hub

Market & Trading Calls

European TTF front-month price outlook: Stable as ample pipeline supply and average renewable generation are expected to balance increased competition for LNG cargoes with Egypt and higher cooling needs. However, a risk to the outlook is posed by the unlikely possibility of US secondary tariffs on buyers of Russian natural gas and LNG.

Asian LNG front-month price outlook: Slightly bearish on robust Chinese LNG inventories, cooler Northeast Asian temperatures, and stabilized Pacific supply outweighing modest demand upside from Taiwan and South Korea

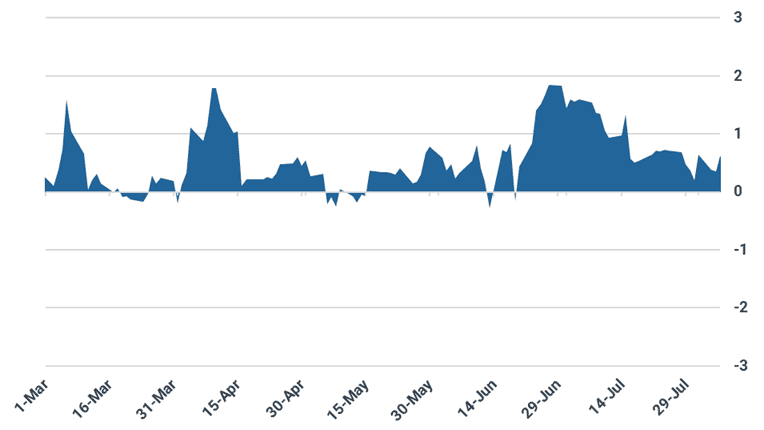

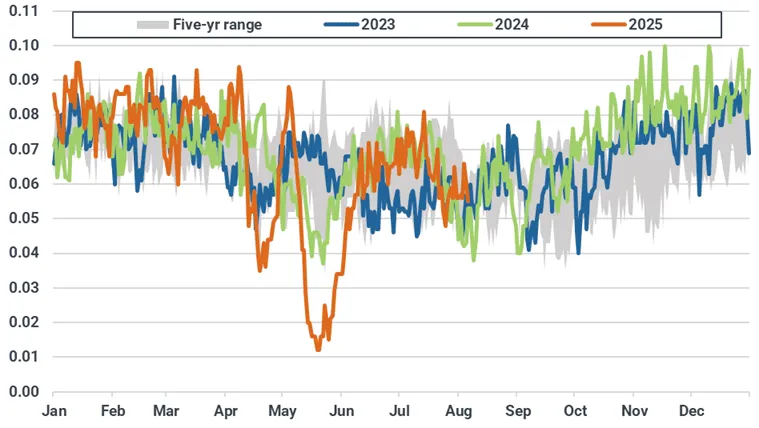

Asian LNG – TTF spread outlook: Slight narrowing as Asian LNG is expected to decline while TTF holds stable. The spread widened to $0.62/MMBtu on 6 August from $0.37/MMBtu on 30 July.

US Henry Hub front-month price outlook: Stable as projections of hot weather in mid-August are overshadowed by strong production and robust storage levels.

Key natural gas and LNG front-month prices ($/MMBtu)

Source: ICE, NYMEX, Spark Commodities. Brent-indexed price represents 12% slope of 90-day moving average of Brent contract. Netforward USGC to NWE calculation is 115% Henry Hub contract plus shipping and regasification costs into Gate (Spark Commodities).

Asian LNG-TTF front-month spread ($/MMBtu)

Source: ICE, Kpler Insight

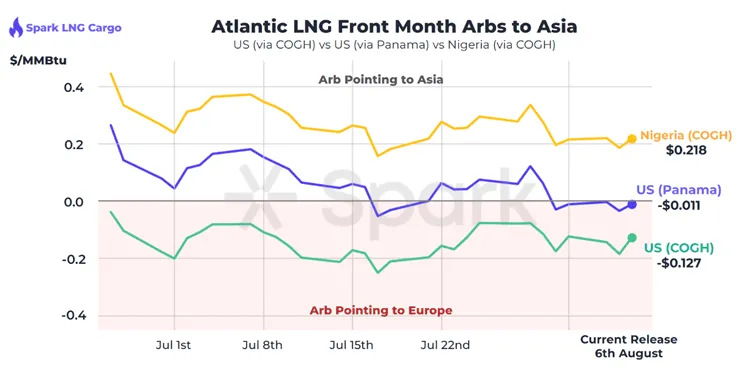

Atlantic basin LNG front-month arbs ($/MMBtu)

Source: Spark Commodities, incorporating ICE-listed Spark Freight and Spark Cargo products. For a full M+12 forward curve and netback cost breakdown, contact Spark at info@sparkcommodities.com.

LNG Supply: Atlantic LNG supply set to recover on Norway restart and rising US feedgas deliveries

Global LNG exports declined as expected last week, dropping by 0.48 mt w/w to 7.92 mt. The United States led the export drop, with a 0.36 mt w/w decline to 1.81 mt. Supply fell mainly due to reduced feedgas flows at Sabine Pass last week and brief outages at Freeport in recent weeks.

For this coming week, we anticipate steady to slightly higher global LNG supply. The return of Norway’s 4.2 mtpa Hammerfest plant following planned maintenance and a rebound in US feedgas deliveries will support Atlantic LNG exports this week. But continued underperformance at Malaysia’s 29.3 mtpa Bintulu and Russia’s 17 mtpa Yamal LNG plants will cap the upside.

Global LNG exports (mt, 10-day moving average)

Source: Kpler

In the Pacific basin this week, a steady drop in exports from Malaysia 29.3 mtpa Bintulu has stabilised, with 10-day moving averages averaging at 0.06 mt/day mark, down from 0.07 mt/day through much of July (see chart). At time of publication, it was unclear what was causing the drop in supply.

Malaysia’s Bintulu LNG exports (mt, 10-day moving average)

Source: Kpler

Meanwhile, LNG Canada continues to export at a rate of 1 cargo per week, as technical issues at one of two gas turbines limits the ramp up of the first 7 mtpa train. The Murex was the first cargo to load in August, leaving the plant on 3 August for South Korea’s Incheon terminal. Meanwhile, the Puteri Mayang is heading towards Kitimat and will be the second cargo to load this month. Kpler Insight expects 0.42 mt (6 cargoes) to load from the facility this month, up from 0.30 mt (4 cargoes) in July.

Australian LNG supply remains robust, with exports hitting their highest level in 4 months at 1.65 mt last week. However, Kpler Insight expects Australian LNG exports to gradually move lower through the course of August, with the 7.8 mtpa Gladstone LNG plant taking maintenance which will knock off half a train of capacity from 9 August to 4 September and the 9 mtpa Ichthys plant is expected to halt operations from 18 August to 8 October.

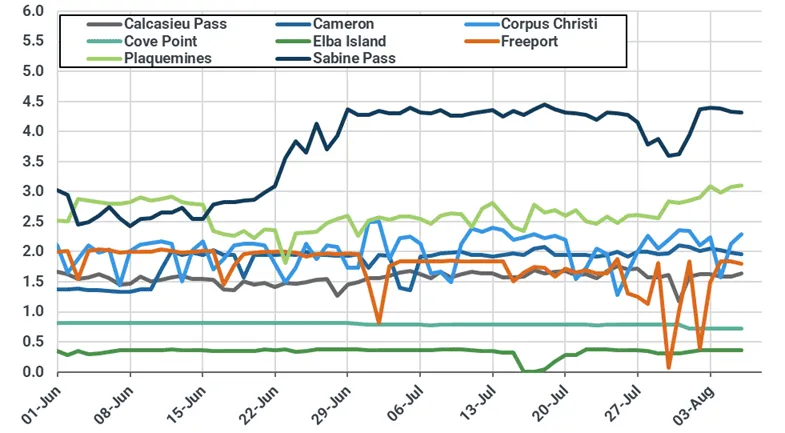

In the Atlantic basin, LNG exports are anticipated to rebound, supported by higher US and Norwegian exports. Feedgas flows into US liquefaction facilities have stepped up to hit the highest level in 3 weeks, which should support improved LNG exports following last week’s decline. Gas supply into the 30 mtpa Sabine Pass facility has recovered after a drop between 27 July-2 August, while feedgas into the 22.6 mtpa Plaquemines facility has taken another step up over the past week, hitting highs of 3.1 bcf/d on 3 August. Venture Global received approval to start up block 14 of 18 at the facility in mid-July.

Kpler continues to monitor exports at the 2.5 mtpa Elba Island facility. Since planned maintenance came to an end on 21 July, the facility has not loaded a cargo. The last carrier to load was the Alicante Knutsen on 5 July and no ballast vessels are currently due to arrive at the facility.

US LNG feedgas deliveries by plant (bcf/d)

Source: Williams, Cheniere, Sempra, Boardwalk, Kinder Morgan, Berkshire Hathaway

In Norway, the 4.2 mtpa Hammerfest plant has returned to service, with the Maran Gas Alexandria loading the first cargo since 18 April. Four ballast vessels are currently waiting outside the plant for loading. Kpler Insight forecasts the plant to load 4-5 cargoes of LNG this month.

Want the complete report?

The full report is available within Insight and contains:

- Europe: Stable TTF as strong supply is expected to balance higher cooling needs next week

- Asia: Slightly bearish signals as strong Chinese LNG inventories, cooler temperatures, and steady supply outweigh modest demand upside from Taiwan and South Korea

- US: Forecast of mid-August heat unable to impress market as Henry Hub remains near $3.00/MMBtu

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Get research & analysis driven by proprietary data