Stable global price outlook for next week: TTF to remain stable as higher global supply caps cold snap demand gains in Europe. Asian LNG and HH follow suit.

Market & trading calls

European TTF front-month price outlook: Stable, as latest weather forecasts suggest the return of higher temperatures in NWE after 18 October, following a shorter-than-expected cold snap between 13-17 October. We anticipate increased demand in the coming days, also supported by a gradual worsening of wind generation, to be met by higher Algerian pipeline exports and stable LNG imports. Recent news about lower-than-expected demand in Egypt is balanced with the possibility of higher exports to Ukraine in the short term.

Asian LNG front-month price outlook: Stable as ample supply, healthy inventories, and softer prompt demand in Taiwan are capping upside. Support from the December contract rollover offsets the bearish pressure.

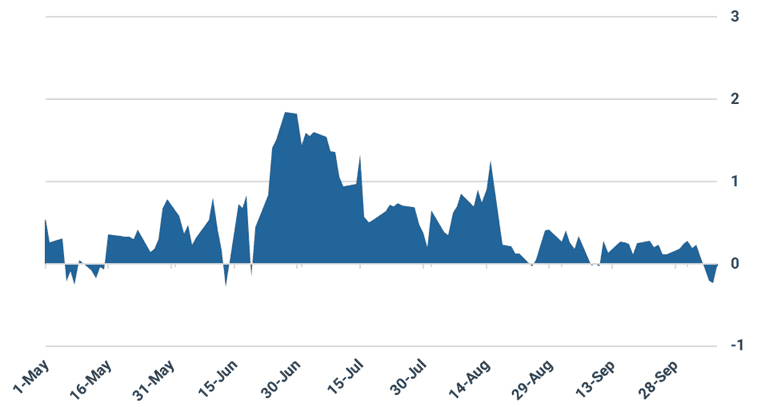

Asian LNG – TTF spread outlook: Stable with both indices likely to trade within recent ranges through the week ahead. The spread narrowed by $0.31/MMBtu to -$0.03/MMBtu on 08 October.

US Henry Hub front-month price outlook: Stable as cooler weather forecasts for the eastern and western US clash with warmer expectations for the central third of the Lower 48.

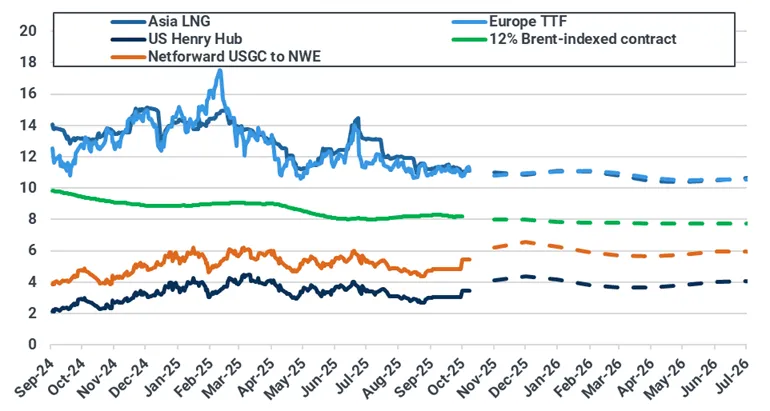

Key natural gas and LNG front-month prices ($/MMBtu)

Source: ICE, NYMEX, Spark Commodities. Brent-indexed price represents 12% slope of 90-day moving average of Brent contract. Netforward USGC to NWE calculation is 115% Henry Hub contract plus shipping and regasification costs into Gate (Spark Commodities).

Asian LNG-TTF front-month spread ($/MMBtu)

Source: ICE, Kpler Insight

Europe: Higher supply and weather revisions pointing to a shorter-than-expected cold snap to keep TTF rangebound

The European TTF front-month increased last week, with prices reaching $11.14/MMBtu on 08 October, $0.38/MMBtu higher than $10.77/MMBtu on 01 October. The gains were driven by attacks on Ukraine’s production and underground storage infrastructure on 03 and 05 October, respectively, as reported by Naftogaz. Prices bounced on the expectation that Ukraine will likely need to ramp up gas imports from the EU to cope with the risks of further attacks on its energy infrastructure during the heating season. Weather forecasts also added to the bullishness, with runs pointing to colder temperatures in several parts of Europe in the coming days. In addition, more maintenance works were announced in Norway for the second half of October, a slow return of Algerian exports to Italy, and a temporary suspension of shipping activities in Qatari waters due to a technical fault with its GPS contributed to the bullishness.

For the week ahead, Kpler Insight has a stable outlook for the TTF front-month contract, as the latest weather forecasts suggest the potential return of higher temperatures in NWE after 18 October, following the expected cold snap between 13-17 October. We expect the increase in demand in the coming days, which is also supported by a gradual worsening of wind generation, to be met by higher supply as we anticipate Algerian pipeline exports to increase and stable LNG imports into the continent. Recent news about lower-than-expected demand in Egypt is balanced with the possibility of higher exports to Ukraine in the short term.

On the supply side, EU pipeline imports increased by 2.5% w/w, reaching 3.13 bcm. Weekly ramp-up in Norwegian and Algerian flows, despite unplanned maintenance works in the former and a slow return in exports from the latter, alongside Turkstream output nearing full capacity, more than offset the loss of supply flows from the UK to EU due to planned works at the UK-Belgium interconnector.

UK daily net pipeline flows to the EU (bcm)

Source: ENTSOG, Kpler Insight

Turkstream daily net pipeline flows to the EU (bcm)

Source: ENTSOG, Kpler Insight

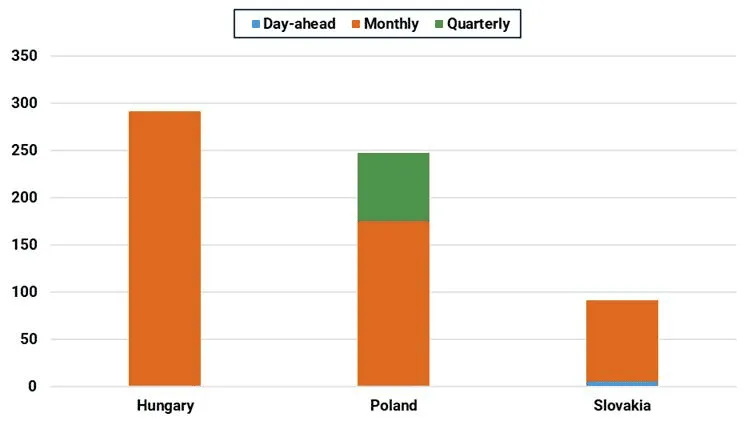

Regarding attacks on Ukraine production and underground storage infrastructure, the impact on imports from the European Union has been limited likely due to capacity constraints with Poland and Hungary and high costs of importing gas via Slovakia. Our view is that it is unlikely that Ukraine will ramp up day-ahead imports via Slovakia as costs become prohibitive for Naftogaz and other players, however, we could see an increase in monthly bookings. So far, most capacity in Q4 has been booked monthly.

Gas TSO UA capacity bookings in Q4 2025 as of 9 Oct (mcm) - excluding DA for UGS

Source: Gas TSO UA, Kpler Insight

Looking into next week, EU-27 net pipeline imports are anticipated to slightly increase, supported by the gradual return of Algerian exports to Italy.

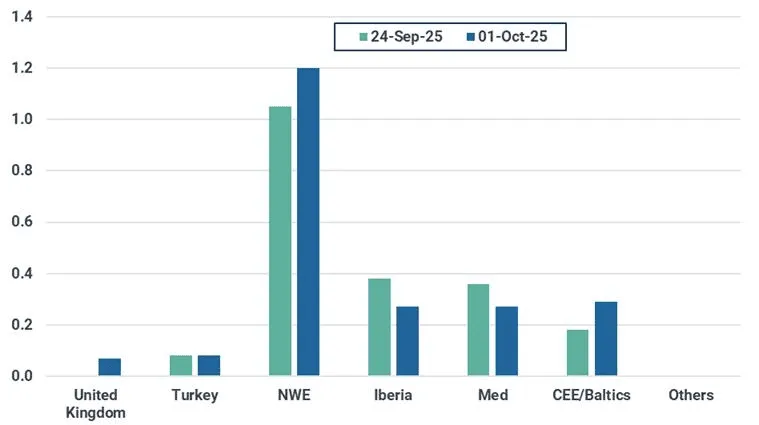

Regarding European LNG imports, they rose w/w for week starting 01 October, reaching 2.2 mt as strong demand emerged from NWE and the CEE/Baltics region. Some demand emerged from the UK and contracted Turkish demand continued.

Looking ahead, we expect LNG volumes to remain relatively stable despite higher volume expected into Turkey and Egypt, as US supply to the region remains plentiful.

EU-27 weekly LNG imports by region (mt)

Source: Kpler Insight. Data represents week commencing 24/09 and 01/10. NWE=FR, BEL, NL, GER. Iberia=ESP, POR. Med=ITA, HVR, GRE. Baltics/CEE=FI, LT, POL. Others=SWE, MT.

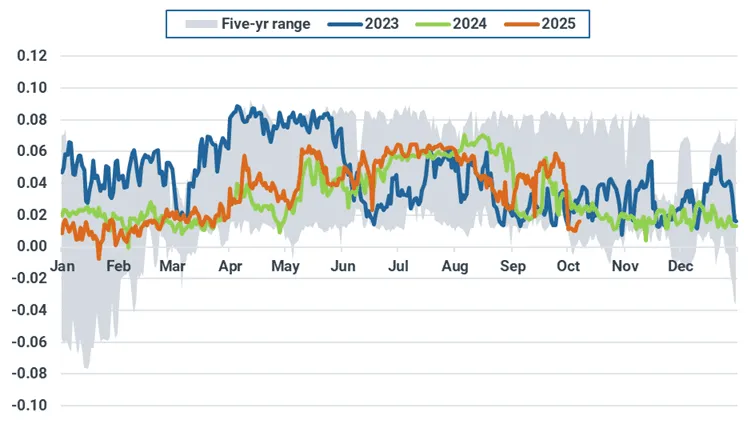

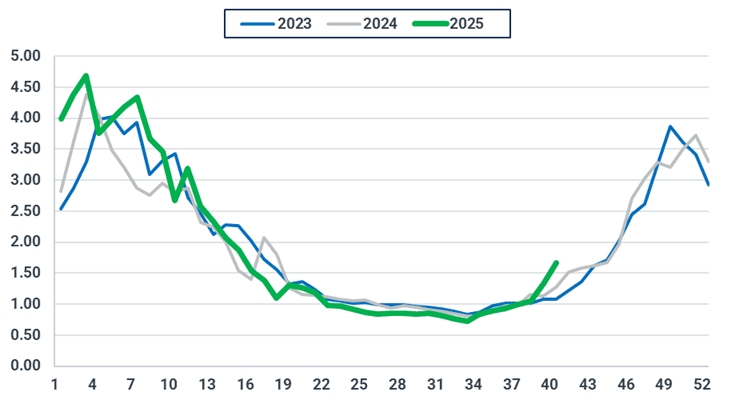

Local distribution consumption continued its upward trend, increasing 25% w/w to 5.3 bcm across 15 EU countries, fueled by lower-than-average temperatures in parts of Europe. However, Eastern countries saw the largest gains, with Romanian distribution demand increasing by almost 90% w/w. Looking ahead, local distribution demand is expected to maintain momentum consistent with typical seasonal patterns as weather forecasts indicate a drop in temperatures in the coming days.

EU-15 weekly consumption in the local distribution sector (bcm)

Source: ENTSOG, ENAGAS, Eurstream, AGCM, Kpler Insight. The EU-15 perimeter includes AT, BE, CZE, FR, HU, GRE, ITA, NL, LUX, POL, POR, ROM, SLVN, SLVK, and SPA.

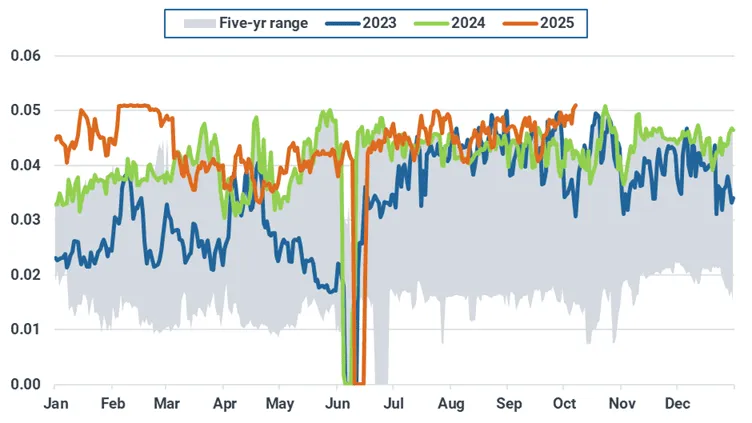

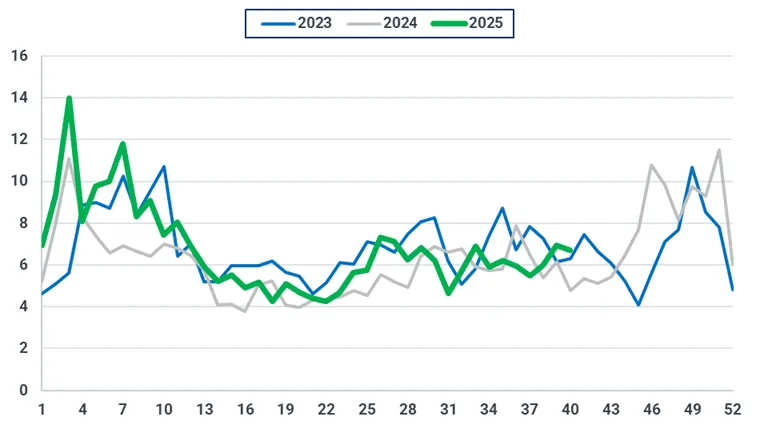

Conversely, EU-24 gas-fired generation dropped by 3% w/w as strong wind output helped offset weekly increases in overall power demand more than the cold weather spread across Europe. Looking ahead, with temperatures expected to stay around seasonal norms and wind output set to rebound, gas-fired generation will depend on the strength of the wind recovery.

EU-24 weekly gas-fired generation (TWh)

Source: Kpler Power, Kpler Insight.

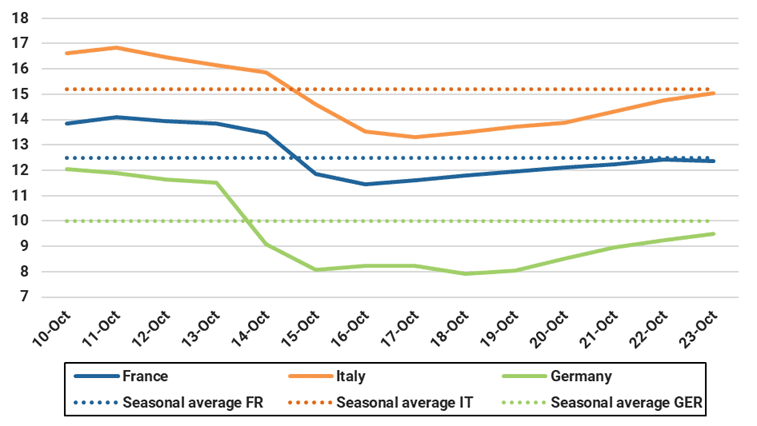

Average forecast temperatures for selected European countries (°C)

Source: Kpler Power. As of 09/10 00:00 UTC.

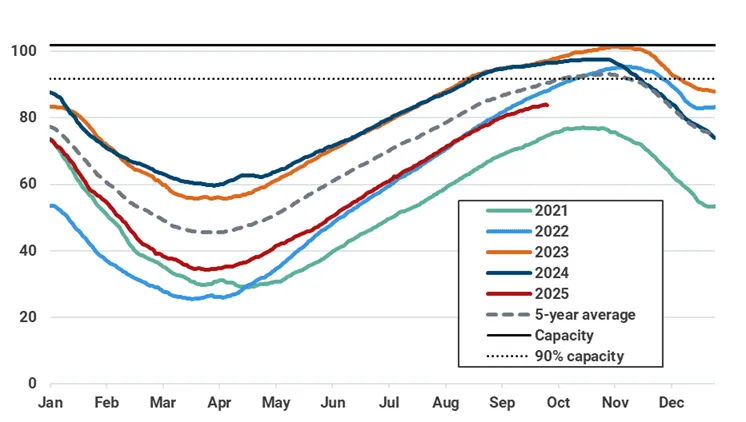

EU-27 underground gas stocks increased to 82.9% as of 8 September, 7.4% percentage points below the five-year average. Low temperatures caused two days of small net withdrawals during the week. Despite this, net injections were observed in the Netherlands, one of the laggard countries in terms of underground storage levels within the EU, mostly driven by a ramp-up in LNG imports.Recent Russian attacks on Ukrainian infrastructure have slightly increased injections into the Ukrainian grid, but no substantial increase in Slovakian flows has been noted so far (Hungarian and Polish flows are already at maximum capacity).

EU-27 underground natural gas inventories (bcm, left) as of 7 September

Source: GIE, Kpler Insight. Latest data as of 30/09/25.

Want the complete report?

The full report is available within Insight and contains:

- Europe: Higher supply and weather revisions pointing to a shorter-than-expected cold snap to keep TTF rangebound

- Asia: Steady outlook as ample supply and inventories offset December rollover signals

- US Henry Hub: Prices prove volatile as mixed fundamentals clash with technical resistance

- LNG Supply: Output set to rise in October as Nigeria’s Bonny and Australia’s Ichthys return to full service following maintenance, Qatari maintenance to cap the upside

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

Research & analysis driven by proprietary data