Weather-driven TTF and Henry Hub strength contrasts with capped upside in Asian LNG

Market & Trading Calls

European TTF front-month price outlook: Bullish, driven by colder temperatures, weaker wind generation, and French nuclear outages lifting gas-for-power demand. Geopolitical risk adds upside, while upward revisions to temperature forecasts or wind output could cap gains.

Asian LNG front-month price outlook: Stable, as ample LNG inventories in China and Korea and rebounding LNG Canada exports cap upside from cold spells in Northeast Asia and firmer TTF movement.

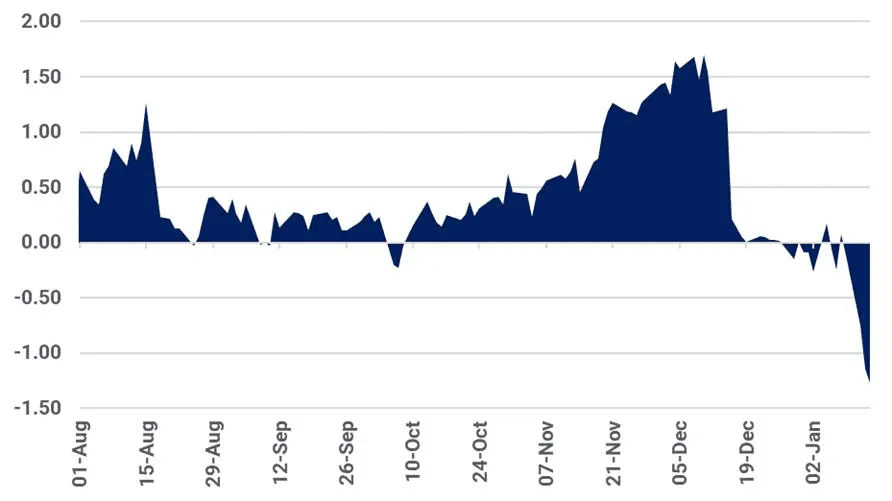

Asian LNG – TTF spread outlook: to Widen as Asian LNG prices are likely to remain stable while TTF is expected to extend gains next week. The negative discount increased over the last week to $1.27/MMBtu on 14 January, largely driven by the sharp w/w uptick in TTF prices.

US Henry Hub front-month price outlook: Slightly bullish as the arrival of colder January weather lends modest upward support to prices, with strong production and a bearish upcoming storage report capping gains.

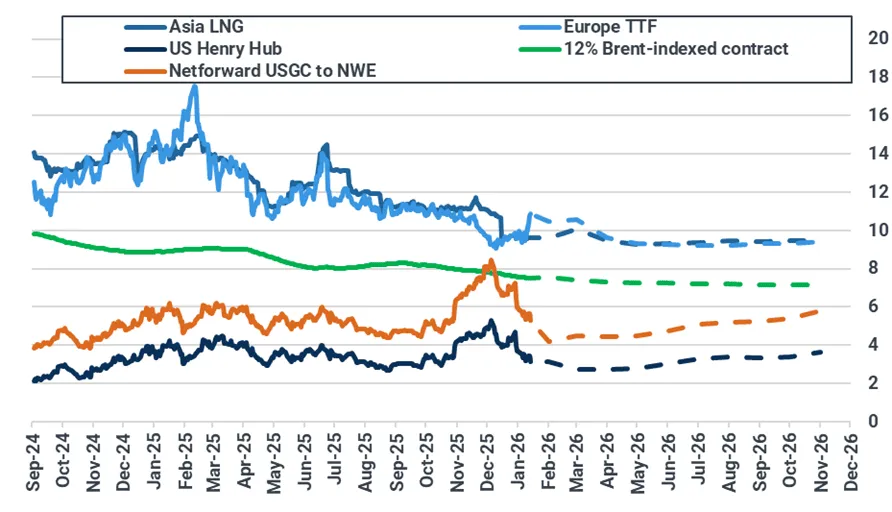

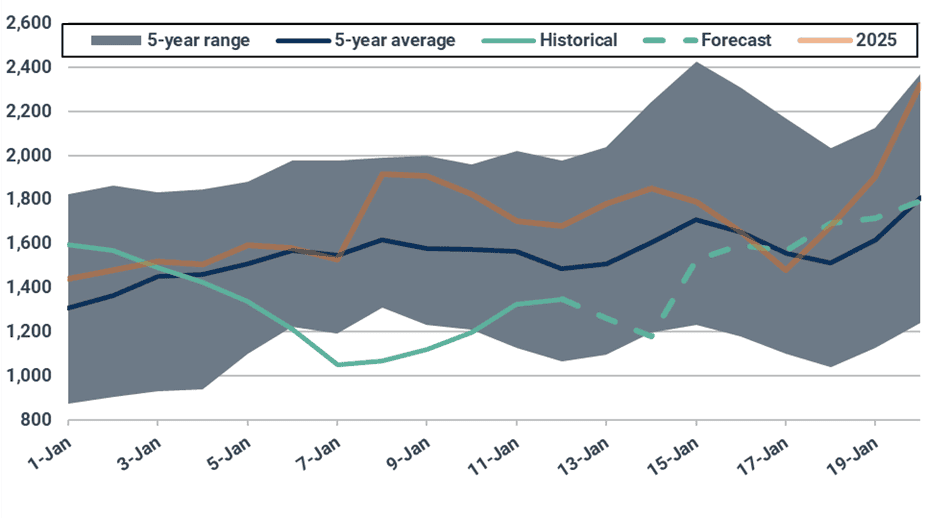

Key natural gas and LNG front-month prices ($/MMBtu)

Source: ICE, NYMEX, Spark Commodities. Brent-indexed price represents 12% slope of 90-day moving average of Brent contract. Netforward USGC to NWE calculation is 115% Henry Hub contract plus shipping and regasification costs into Gate (Spark Commodities).

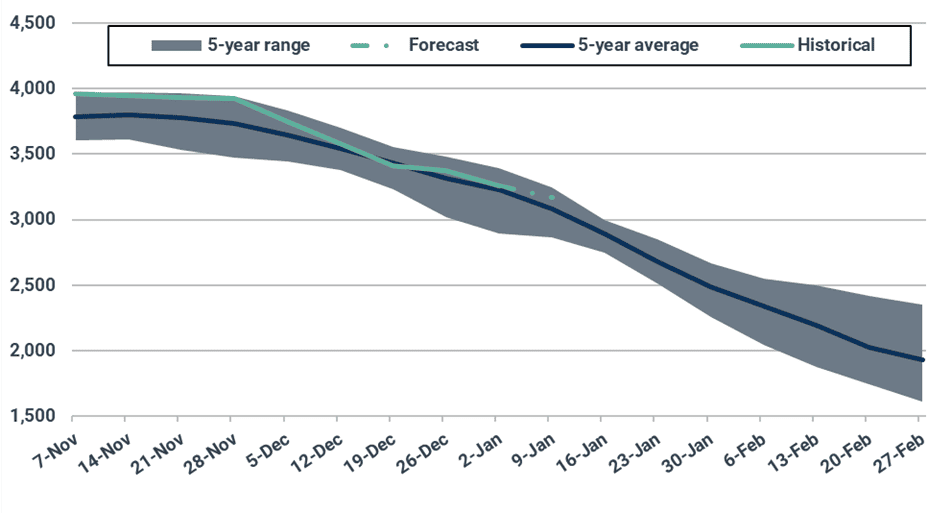

Asian LNG-TTF front-month spread ($/MMBtu)

Source: ICE, Kpler Insight

Europe: Bullish outlook for TTF driven by colder weather forecasts, and rising gas-for-power demand

European TTF front-month contract rose sharply last week to $10.86/MMBtu on 14 January, increasing by $1/MMBtu (+10%) from 7 January. The rally was driven by increasingly pessimistic weather forecasts, with significantly below-average temperatures expected from next week. Rising storage withdrawal rates have further supported prices, amplifying concerns over faster-than-expected stock drawdowns. While pipeline supply remains stable and LNG imports are recovering, colder weather is expected to lift consumption, offsetting the otherwise comfortable supply backdrop.

Looking ahead, Kpler Insight holds a bullish view on the TTF front-month contract for next week, as latest forecasts revised temperatures lower across the continent. In addition, wind generation expectations have been revised down, with Germany alone seeing an estimated 8 GW downward revision to expected wind output. Combined with outages at several French nuclear units, these factors are expected to lift gas-for-power demand, particularly in Northwest Europe, providing further upside support to prices. Additional upside risks stem from geopolitical uncertainty, with markets closely monitoring developments related to Iran. That said, downside risks remain should weather forecasts shift warmer in the coming days.

Turning to supply, EU net pipeline imports increased by 7% w/w to an estimated 3.4 bcm. The rise was driven by slightly higher Algerian flows, which continue to recover following extended maintenance in December, alongside higher net inflows from the UK. Norwegian flows remained stable w/w despite maintenance at the Nyhamna processing plant. Looking ahead, Kpler Insight expects EU net pipeline imports to remain broadly stable, as no major maintenance events are scheduled and Gassco has not revised its planned outage schedule, this should offset increased exports from Poland and Slovakia to Ukraine.

United Kingdom daily net pipeline flows to the EU (bcm)

Source: ENTSOG, Kpler Insight

Aggregate daily capacity unavailability of Norwegian fields and processing plants over the next 30 days (scm)

Source: GASSCO, Kpler Insight. As of 15 January 2026 14:00 UTC

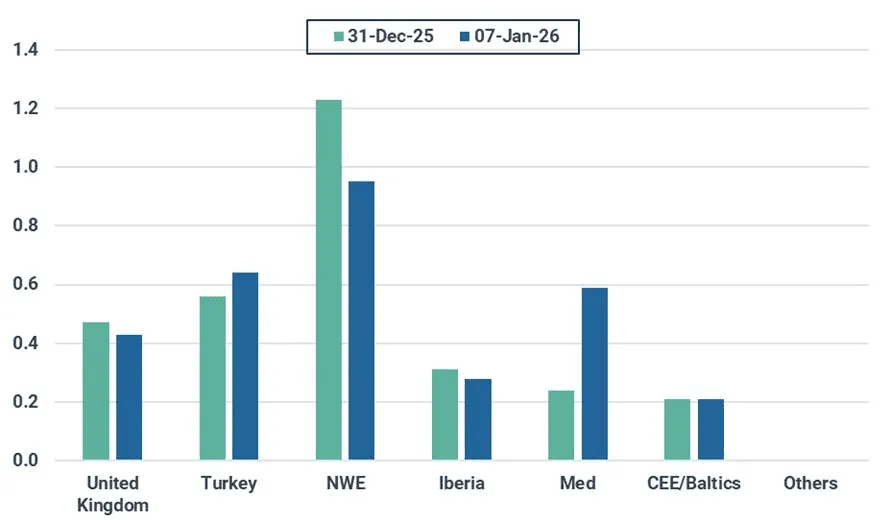

European LNG imports increased by 3% w/w to 3.1 mt last week. Lower arrivals in Northwest Europe, the UK, and Iberia were more than offset by stronger inflows into Turkey and the Mediterranean, particularly Italy, where the Ravenna FSRU and other terminals received their first cargoes in over a week. Looking ahead, European LNG imports are expected to rise sharply, supported by a recovery in Atlantic Basin exports following a dip observed in the week of the 22 December, and higher TTF prices attracting uncommitted cargoes to Europe.

EU-27 weekly LNG imports by region (mt)

Source: Kpler Insight. Data represents week commencing 31/12 and 07/01. NWE=FR, BEL, NL, GER. Iberia=ESP, POR. Med=ITA, HVR, GRE. Baltics/CEE=FI, LT, POL. Others=SWE, MT.

On the demand side, local distribution consumption rose to an estimated 5 bcm across 15 EU countries, up 10.5% w/w, marking the highest level recorded for the first two weeks of the year since 2023. While temperatures increased toward the end of the week, this was insufficient to offset the impact of the preceding cold spell. Kpler Insight expects local distribution to keep increasing as forecasts point to persistently below-average temperatures over the coming week.

EU-15 weekly consumption in the local distribution sector (bcm)

Source: ENTSOG, ENAGAS, Eustream, AGCM, Kpler Insight. The EU-15 perimeter includes AT, BE, CZE, FR, HU, GRE, ITA, NL, LUX, POL, POR, ROM, SLVN, SLVK, and SPA.

On the power side, EU-25 gas-fired generation rose sharply to an estimated 12 TWh, up 20% w/w. The increase was driven by stronger total power demand which increased by 11% w/w. Looking ahead, Kpler Insight expects gas-fired generation to increase further next week, as a combination of nuclear outages in France, colder temperature forecasts, and weaker wind generation raises the call on thermal units to meet power demand.

EU-25 weekly gas-fired generation (TWh)

Source: Kpler Power, Kpler Insight.

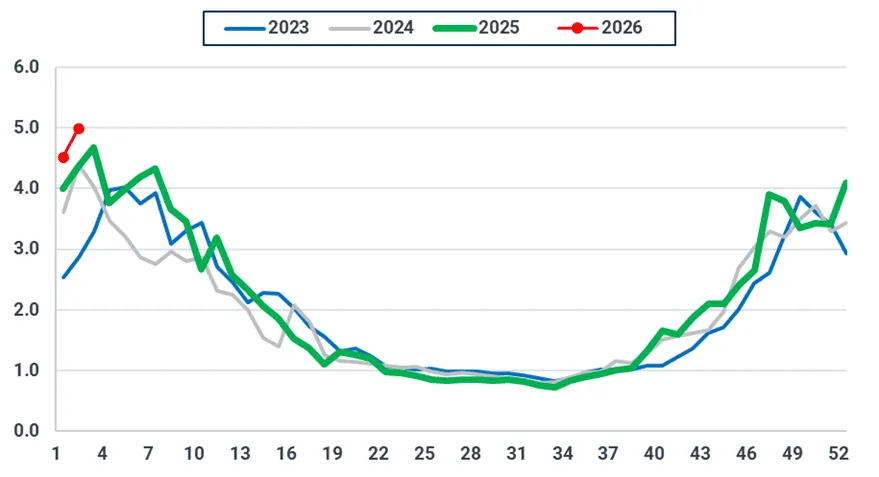

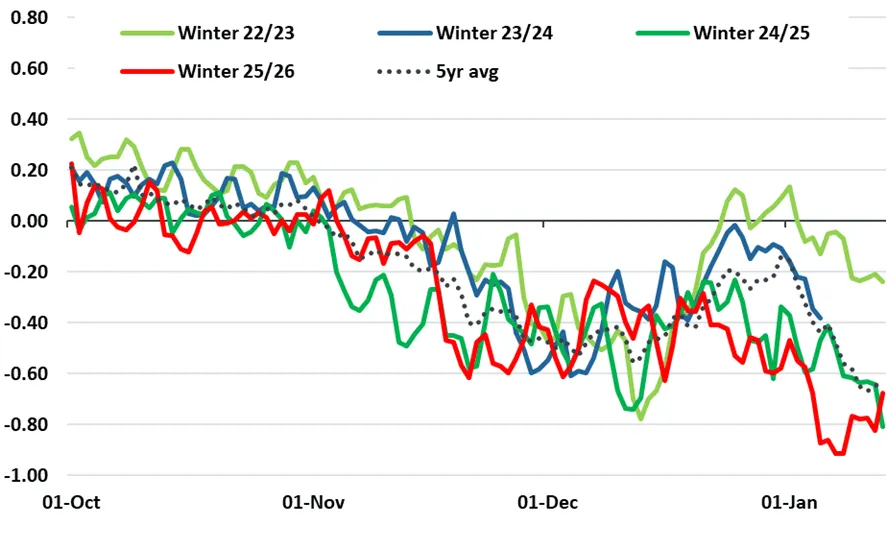

Average forecast temperatures for NWE, excluding the UK (°C)

Source: Kpler Insight. Run comparison 15/01 (solid) vs. 08/01 (dotted), 00:00 UTC. Seasonal is a five-year average. NWE includes BE, NL, FR, DE

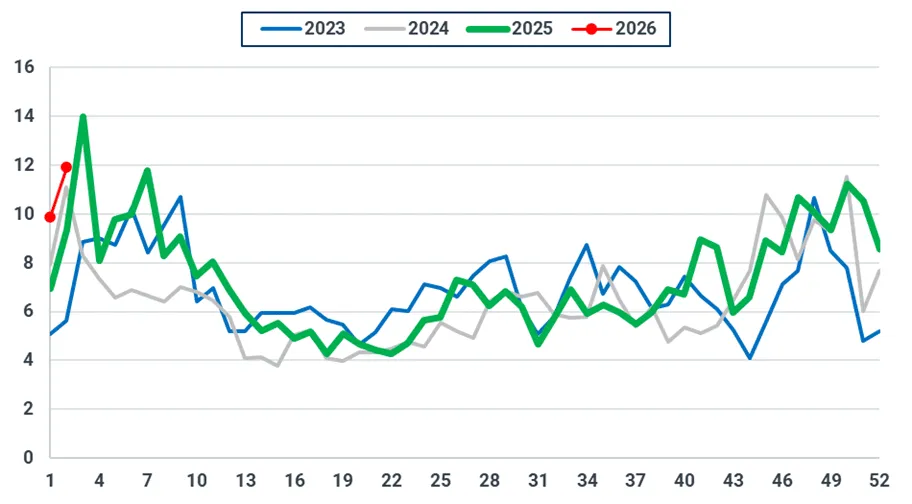

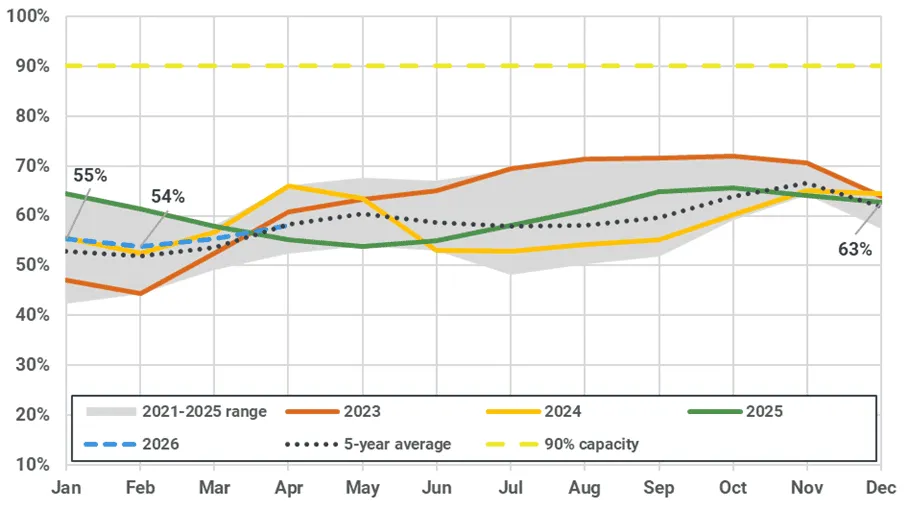

EU-27 underground gas stocks fell to 52.5% full as of 13 January, down 5.6 percentage points w/w. Withdrawal rates eased in the previous week, in line with our expectations, as a gradual rise in temperatures and stronger wind output during the second half of the week reduced demand. Looking ahead, Kpler Insight expects storage withdrawals to pick up as colder temperatures and weaker wind generation increase heating and gas-for-power demand. However, the day-ahead versus month-ahead TTF spread has narrowed from €0.82/MWh on 7 January to €0.18/MWh on 14 January which could cap upside to withdrawal rates unless the day-ahead contract regains a stronger premium during the forecast cold snap.

EU-27 daily UGS change (bcm)

Source: GIE, Kpler Insight. Latest data as of 13 January 2026.

Asia: Ample Pacific supply and LNG inventories cap upside from brief Asian cold spells and stronger TTF movement

Asian LNG prices kept largely stable at $9.60/MMBtu on 14 January, down 0.01 w/w, as upside from earlier cold snaps in Northeast Asia was offset by ample LNG inventories and recovering Pacific supply.

Asian LNG prices are expected to remain broadly stable this week, as healthy LNG inventories, rebounding supply from LNG Canada and softer gas-for-power demand in Taiwan offsetting upside from upcoming cold spells in Northeast Asia. Limited near-term restocking needs continue to restrain competition for additional cargoes despite a stronger TTF. The March contract rollover may prompt a brief uptick, but prices are expected to ease and stabilise as colder conditions begin to subside from late next week.

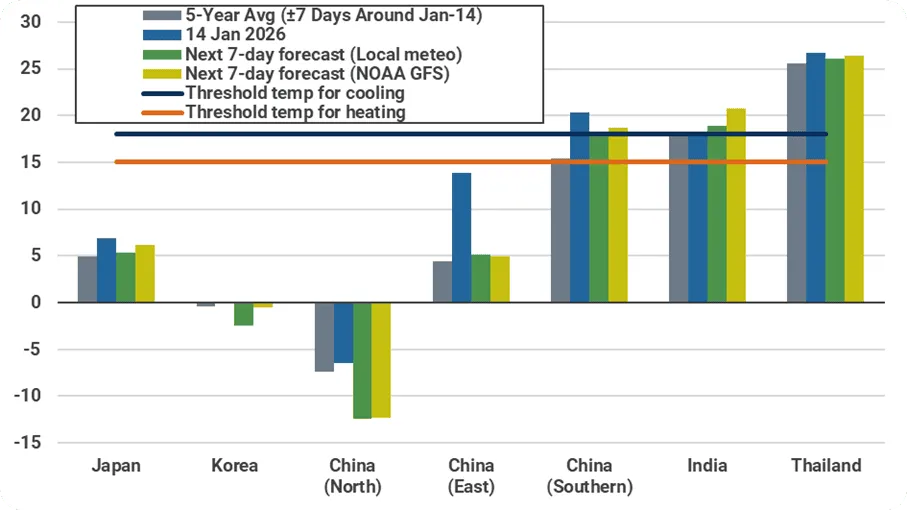

Temperatures across North China and Korea are expected to drop below five-year averages, lifting regional heating-related gas demand week-on-week. In Southeast and South Asia, readings are forecast to track seasonal averages, keeping cooling-related gas demand stable w/w. Overall, below-normal temperatures in North China are largely driving higher gas demand across Asia w/w.

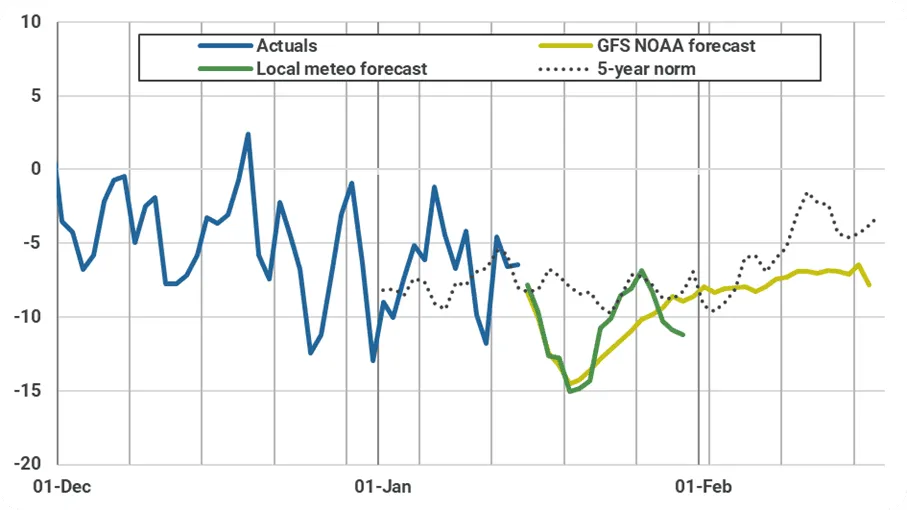

Temperature trend in North China (°C)

Source: Meteostat, GFS, Kpler Insight. As of 15 January 2026 00:00:00 UTC. Population-weighted average temperature is shown for both historical and forecast.

Forecasted average temperatures for Asian countries (°C)

Source: Meteostat, Kpler Insight. As of 15 January 2026 00:00:00 UTC. Population-weighted average temperature of selected major cities across a country is shown for both historical and forecast.

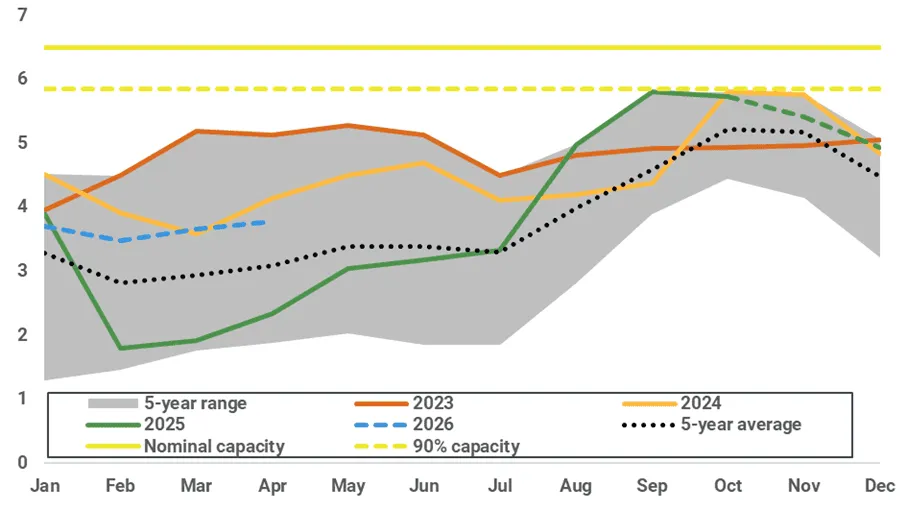

Japan’s METI reported major utility LNG stocks at 2.3 mt as of 11 January, largely stable w/w and tracking five-year averages. Planned maintenance at Shimane 2 nuclear unit (820 MW) from 9 February, alongside the ramp-up of first unit (622 MW) at Himeji gas-fired plant, is expected to boost near-term gas-fired generation. As a result, implied power-sector LNG inventories are projected to ease to 2.4 mt by end-Jan and 2.3 mt by end-Feb. Below-average February inventories are unlikely to trigger aggressive restocking or provide support to regional prices, given expectations of warmer conditions in March.

Japan implied power-sector LNG inventory forecast (mt)

Source: METI, Kpler Insight

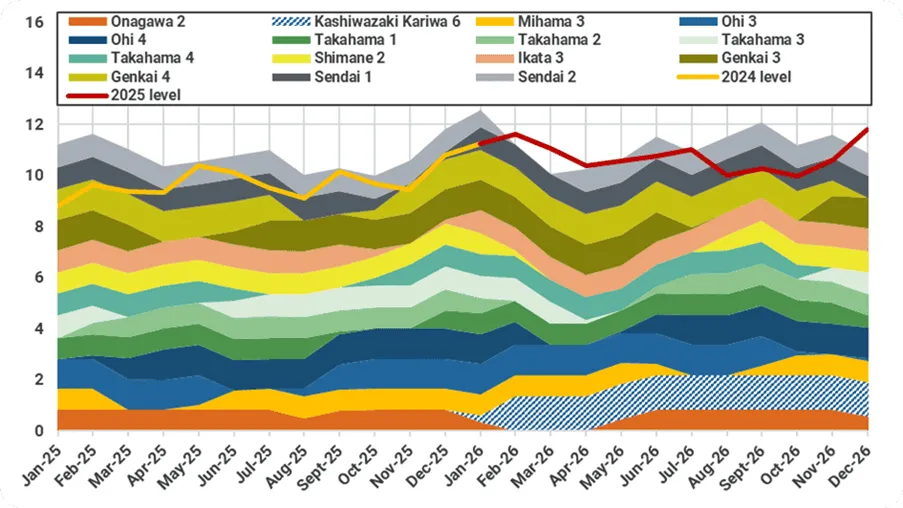

Japan monthly nuclear availability forecast by reactor (GW)

Source: HJKS, Kpler Insight. Note: Dashed area shows the assumed restart timeline and capacity availability of Kashiwazaki Kariwa 6

In South Korea, upcoming cold snaps are expected to lift heating-related gas demand w/w. Despite stronger y/y coal-fired generation expected in January, Kpler Insight projects gas-fired generation to rise by 0.6 TWh y/y to offset lower nuclear output amid extended outages. Total LNG inventories are forecast to ease to 3.7 mt by end-January and 3.5 mt by end-February, slightly below previous estimates but still above five-year averages. Healthy Korean inventories continue to cap regional price upside.

Year-on-year change in power generation by fuel type in Korea (TWh)

Source: KPX, Kpler Insight. Note: y/y changes in January is our forecast data.

South Korea monthly implied LNG inventory (mt)

Source: Kpler Insight, KESIS

In China, Kpler Insight has slightly revised up January HDDs for North China following colder NCC forecasts on 12 January. Preliminary China Customs data show total natural gas imports of 13.4 mt in December, likely reflecting stronger-than-expected LNG imports. As a result, ample inventory build-up is expected to buffer weather-driven drawdowns, with implied LNG inventories easing to 55% full by end-Jan and 54% by end-Feb—above five-year averages and capping regional price upside.

Population-weighted HDD (Heating Degree Day) in North China (degree-days)

Source: Meteostat, Kpler Insight

China implied LNG inventory forecast (%)

Source: Kpler Insight

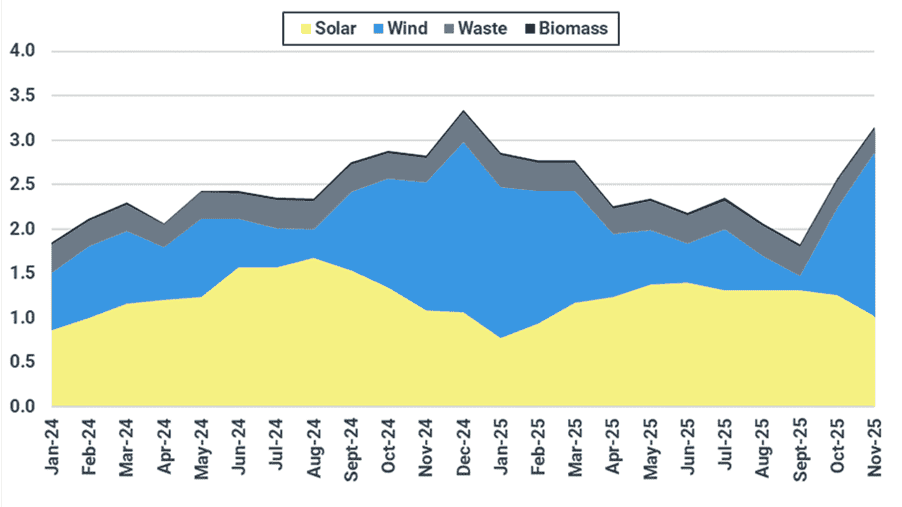

Elsewhere in Asia, Taiwan’s latest MOEA data point to stronger-than-expected wind generation amid windier conditions and rising capacity, slightly reducing near-term gas-for-power demand and adding modest downward pressure to regional spot prices.

Historical renewables generation by type (TWh)

Source: MOEA

US: Henry Hub hits seasonal lows amid uncertain weather outlook, robust production

US Henry Hub front-month prices settled at $3.10/MMBtu on 14 January, down substantially from $3.56/MMBtu on 7 January. Price movements proved erratic over the last week, with Friday settling at $3.17/MMBtu due to strong gas production and weak near-term heating demand supporting bearish market sentiment. However, over the weekend both the US and EU weather models added moderate amounts of HDDs, showing a possible series of back-to-back cold snaps starting at the end of this week that brought prices back to $3.41/MMBtu. Prices held steady during trading on Tuesday before falling $0.30/MMBtu on Wednesday. Persistently high natural gas production, expectations of a bearish storage report, and growing uncertainty surrounding the intensity of upcoming cold came together to shift the market harshly bearish.

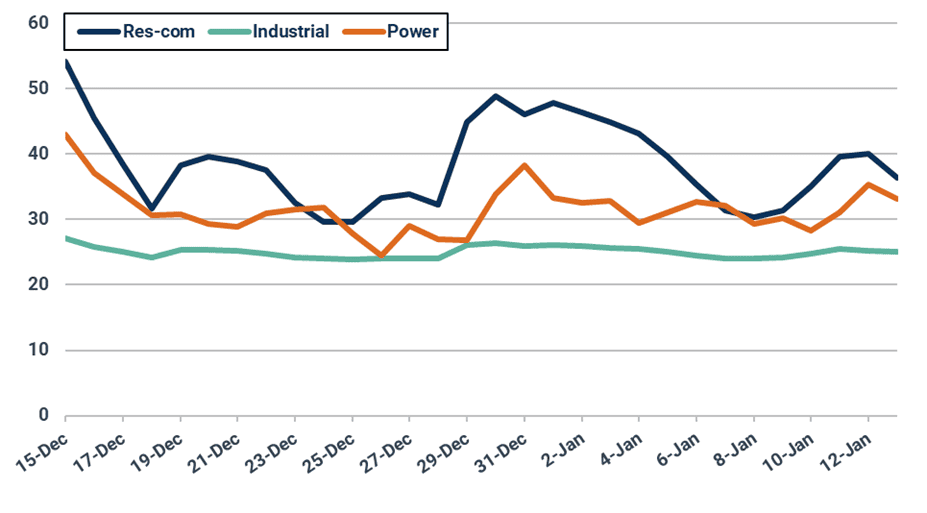

US domestic gas consumption by sector (bcf/d)

Source: EIA

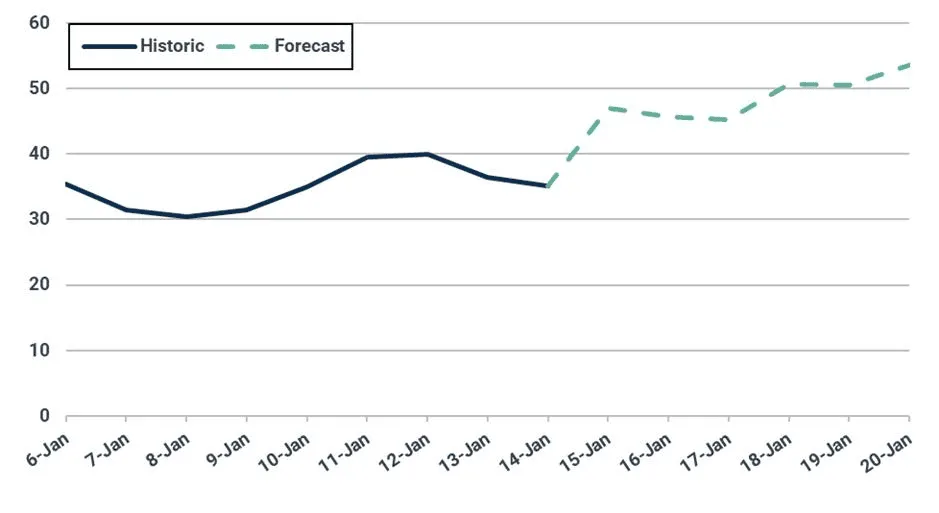

Broadly above-average temperatures across the Lower 48 over the last week kept heating demand relatively tame. Demand fell to 30 Bcf/d on 8 January before slowly rising back towards 40 Bcf/d on 12 January. Warmer weather mid-week saw demand drop again, though a cold front is set to impact the northern half of the US in the coming week, increasing heating demand considerably. Heating requirements are projected to rise to just shy of 50 Bcf/d on Thursday and remain elevated for much of the coming week. While elevated compared to demand earlier in the month, upcoming demand expectations are a far cry from the nearly 70 Bcf/d of heating demand seen in the same period last year. Kpler Insight expects prices to rise back towards $3.50/MMBtu over the next seven days with the onset of colder weather.

Forecast of residential and commercial demand

Source: National Weather Service

Forecast of heating degree days

Source: National Weather Service

US dry gas production averaged near 110 Bcf/d over the last week, holding steady at December levels. Producers are likely to keep supply near current values given upcoming cold weather and continually robust LNG feed gas demand. Kpler Insight expects supply to remain at 110 Bcf/d for the coming week.

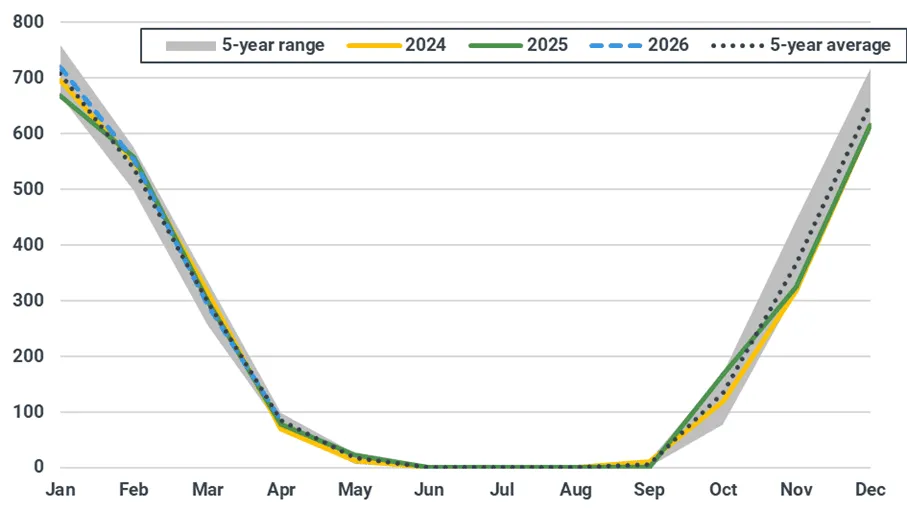

Forecast of natural gas volumes in underground storage (bcf)

Source: EIA

The US withdrew 119 Bcf from underground storage for the week ending 2 January, reflecting a period of relatively cold weather. This storage pull brought total US inventories to 3,256 Bcf, only 1% above the 5-year average. However, the surplus of gas in storage is set to grow, with weak weather driven demand and strong production during the week ending 9 January leading to a decidedly bearish storage pull. Kpler Insight projects an 83 Bcf net withdrawal from storage for the week ending 9 January.

Global LNG Supply: US LNG exports hit record weekly high

Despite US LNG exports hitting an all-time weekly high, global LNG exports slipped last week by 0.12 mt to 9.53 mt. LNG Canada didn’t export any cargoes last week, while Indonesia reduced supply to the international market by 0.16 mt w/w to 0.18 mt.

For this week, we anticipate largely flat to slightly higher global LNG supply. Kpler continues to monitor US feedgas nominations, LNG Canada exports, supply from Algeria and the Alexey Kosygin Arc7, which is likely to begin lifting volume from Russia’s sanctioned Arctic LNG 2 plant in the coming weeks. Several new and and restarted liquefaction plants are also expected to come online over the coming weeks, including Australia’s 3.7 mtpa Darwin, Congo’s 2.4 mtpa FLNG 2 and US’ 5.2 mtpa Golden Pass T1.

Global LNG exports (mt, 10-day moving average)

Source: Kpler

In the Pacific basin, the 14 mtpa LNG Canada facility had disappointing exports last week with no cargoes loaded. However, supply from the plant is ramping up this week with 2 cargoes already loaded on board the Puteri Ledang and Valencia Knutsen and at least one additional loading expected on board the Diamond Gas Crystal. Four ballast vessels are waiting offshore for loading over the coming weeks as train 2 ramps up its utilization rate. Rising supply from the plant is expected to push Pacific basin LNG exports to fresh record highs in the second half of January.

Further adding to Pacific basin supply is the upcoming restart of Australia’s 3.7 mtpa Darwin facility. The Kool Husky vessel had been expected to be the first loading from the facility around mid-January, but later diverted to North West Shelf. The Kool Blizzard that arrived offshore of Darwin on 14 January is now currently tipped to load the first cargo from the facility.

In the Atlantic basin, US LNG exports hit record weekly highs of 2.74 mt last week – 0.12 mt higher than the previous record in mid-December. Feedgas into liquefaction plants also topped a record 18.99 bcf on 12 January on resilient winter utilisation rates and supported by the Plaquemines and Corpus Christi stage 3 expansion coming online in 2025. However, US feedgas has since dipped from the record high recorded on 12 January amid an outage at the Freeport and Corpus Christi plants on 13 and 14 January, respectively. US feedgas slipped to 16.77 bcf on 14 January.

Algerian LNG exports remain subdued, with loadings tracking near the lower end of five-year range, potentially reflecting colder weather conditions driving up the gas demand in the country. Pipeline exports to Italy and Spain, however, remain resilient. Algeria’s domestic gas balance is tight, meaning disruptions on the supply side or periods of increased demand can curtail exports.

Algeria LNG exports (mt, 10-day moving average)

Source: Kpler

Kpler Insight continues to monitor developments at new liquefaction facilities in the Atlantic basin, most notably Congo FLNG 2 and the US’ Golden Pass facility. In recent developments, the Congo FLNG 2 facility has now received a partial cooldown cargo on board the Seapeak Galicia, with a first LNG cargo export expected in February.

Meanwhile, exports could soon rise from the sanctioned Arctic LNG 2 facility following the handover of the Alexey Kosygin Arc7 vessel to Russia’s Sovcomflot. The vessel is currently moored transiting the Northern Sea Route and will likely loading at the Arctic LNG 2 facility before the end of the month. The completion of this vessel raises the plant’s Arc7 vessel availability to 2 vessels, enabling higher winter LNG exports. Amid the addition of this vessel, Kpler Insight has revised up its annual LNG export forecast for the plant from 4.1 mt to 5.7 mt in 2026, with technical issues at the plant and China’s Beihai LNG demand likely to continue limiting supply.

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you to track critical crude oil market developments for your own analysis. Our precise forecasting empowers smarter trading and risk management decisions.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler