Balances turn negative amid 6 Mbd supply cut in May-June

Downward revisions of around 6 Mbd to Middle Eastern supply for May and June have outpaced the corresponding revisions to global crude demand (-1 Mbd over the same period), pushing the global crude balance into deficit and implying stock draws of ~100 Mbbls through late June.

Key takeaways

- Supply revisions: Middle Eastern supply revised down ~6 Mbd for May–June.

- Demand revisions: Global crude demand revised down ~1 Mbd over the same period.

- Global crude balance outlook: Due to the discrepancy between our supply and demand revisions, the global crude balance has turned negative, implying ~100 Mbbl stock draws through late June.

- Logistical bottlenecks: Logistical bottlenecks post-reopening are expected to be the key near-term constraint on supply recovery.

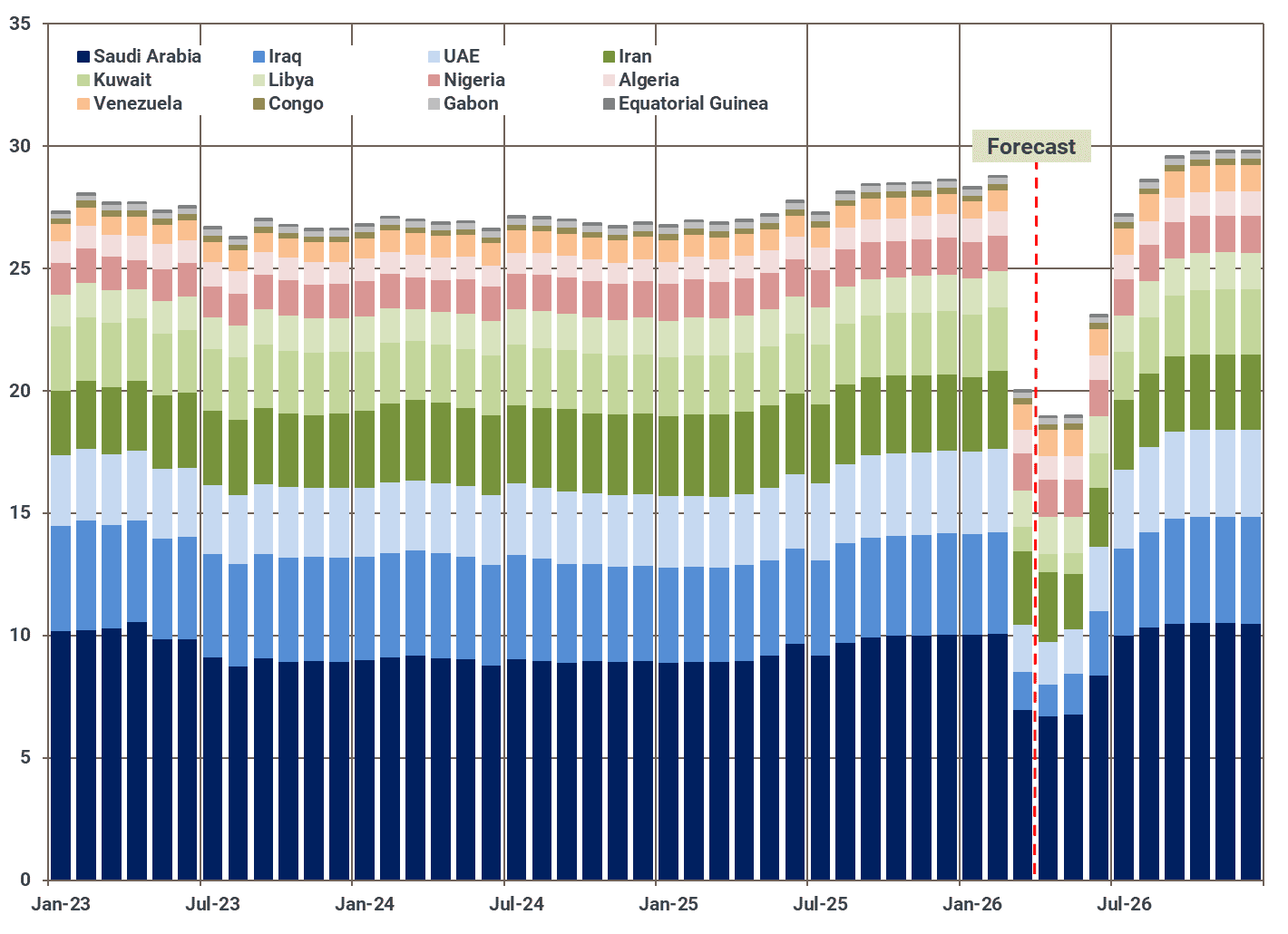

Following a review of our previous base-case assumption, which projected flows via the Strait of Hormuz gradually returning by late April, we have postponed this timeline to late May. The later-than-expected return of flows from the Strait of Hormuz will restrict Middle Eastern crude supply through May, with our base case now assuming relatively flat Middle Eastern crude supply next month. The latest revisions see May supply revised downward by roughly 6 Mbd. Further downward revisions are likely as the US blockade has constrained Iranian crude exports, putting 1.8 Mbd of Iranian crude supply at risk in the weeks ahead.

OPEC-12 crude supply by member, Mbd

Source: Kpler

While a potential recovery in Middle Eastern crude supply will depend on several factors, such as reservoir behaviour, infrastructure damage, and export constraints, logistical bottlenecks are likely to pose the greatest headwinds in the near term following a reopening. These assumptions have led to more severe downward revisions to our June forecast, with total supply revised down by just under 6 Mbd.

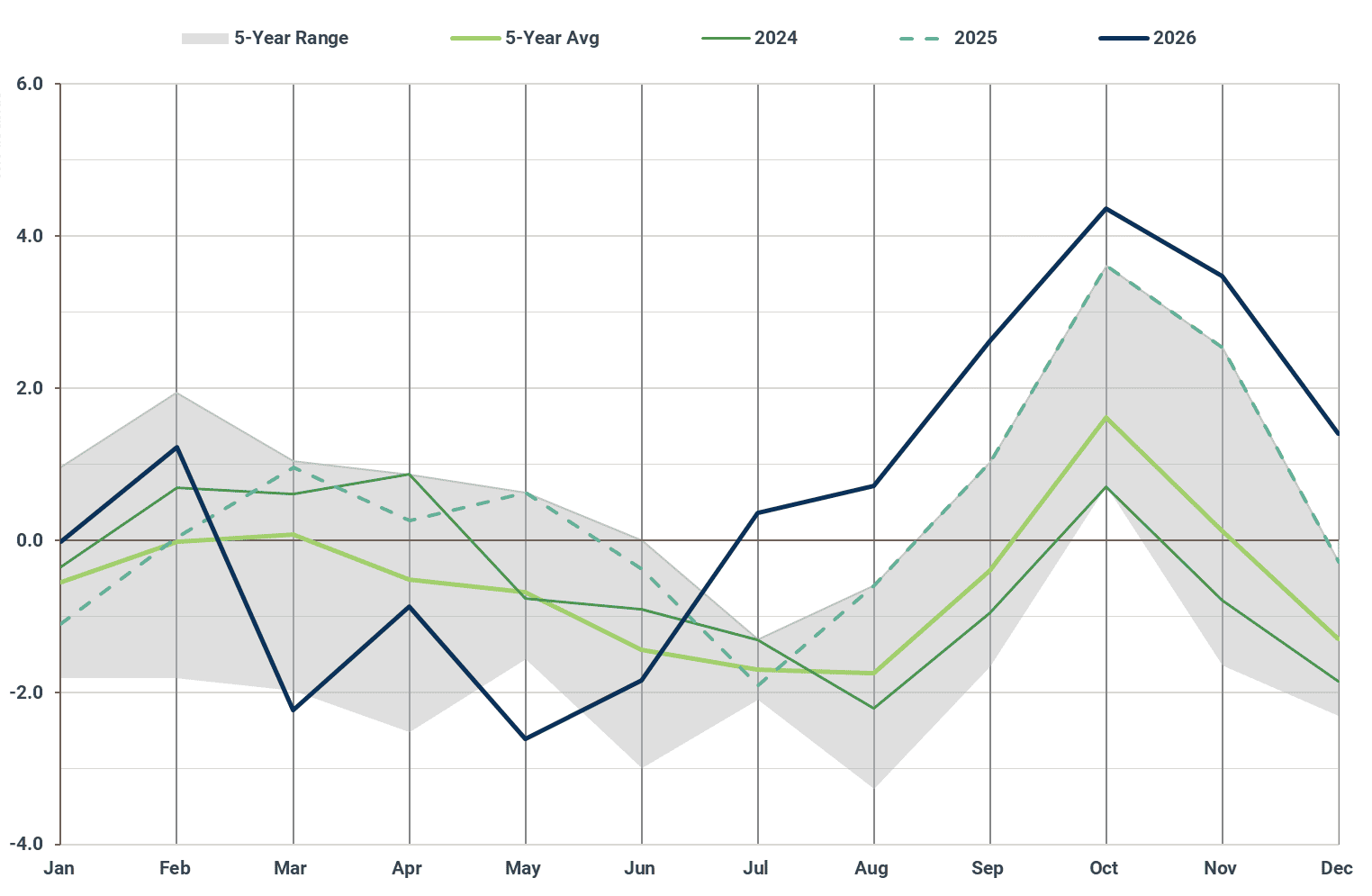

This stands in comparison to modest declines (relative to our previous view) in global crude demand, which has been revised downward by roughly 1 Mbd across May and June.

Considering this discrepancy between our supply and demand revisions, global balances are expected to remain tighter than previously anticipated. The global crude and condensate balance now shows a deficit of ~2 Mbd for May and ~1 Mbd for June, broadly in line with levels seen in March and expected for April. This implies global crude stock draws of around 100 Mbbls by late June.

Global crude and condensate balance, Mbd

Source: Kpler

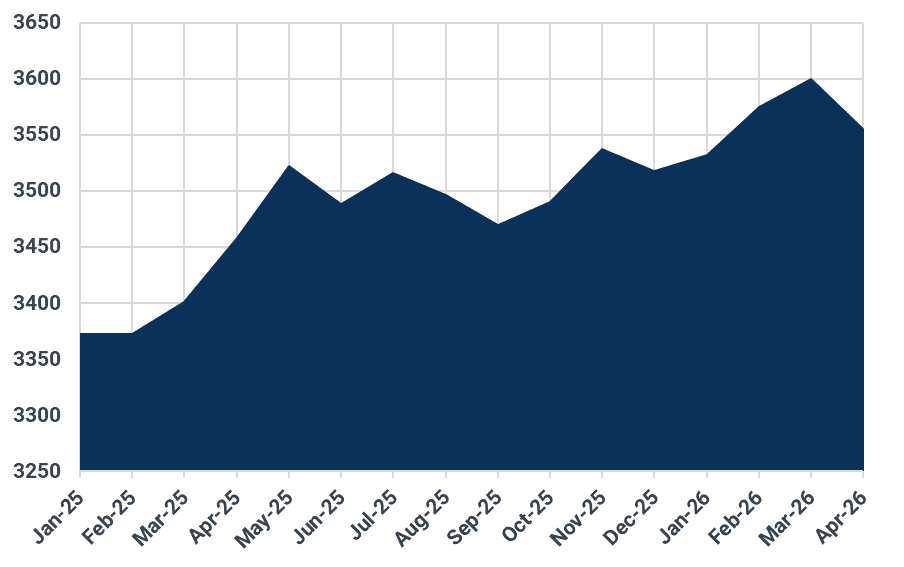

Recent data has shown that global stock draws have accelerated in April. The reasons for this are varied, including the fact that some Middle Eastern cargoes that departed prior to the conflict were still arriving at their destinations in late March and early April. Moreover, March saw an increase in inventories in the affected Middle Eastern countries, offsetting declines elsewhere.

Global onshore crude inventories, Mbbls

Source: Kpler

See why the most successful traders and shipping experts use Kpler