War Endurance Model Update: Jet Inventories draw gradually then suddenly

Global jet fuel markets have exhausted their primary buffer, with jet fuel on water no longer able to offset the loss of Middle Eastern and Chinese supply as refinery runs begin to fall. As the system shifts to drawing down inventories, the adjustment moves from price to availability, setting the stage for rapid tightening and demand rationing.

Key Points

- Jet fuel on water has been the buffer—and it is now largely exhausted, removing the system’s most flexible source of supply.

- The market is structurally short, with ~700 kb/d of Middle Eastern and Chinese supply removed and refinery runs now declining, tightening balances further.

- Europe’s ~50 days of cover is not a cushion, but a steady-state level that will erode quickly as inventories begin to draw toward operational minimums.

- The adjustment is shifting from price to availability, with inventories now doing the work and setting up demand rationing and flight disruptions as the next phase.

Ernest Hemingway once wrote that bankruptcy happens “gradually, then suddenly.” That is how markets adjust as well, and it is exactly what is now unfolding in refined products.

The product market has been cushioned by oil on water, a floating supply pool of cargoes at sea that has acted as a temporary bridge to importing regions. That bridge is now exhausted. While this note could address many products, I want to start with jet fuel. It is the most visible, the most immediate, and the one most likely to disrupt behavior, particularly summer travel.

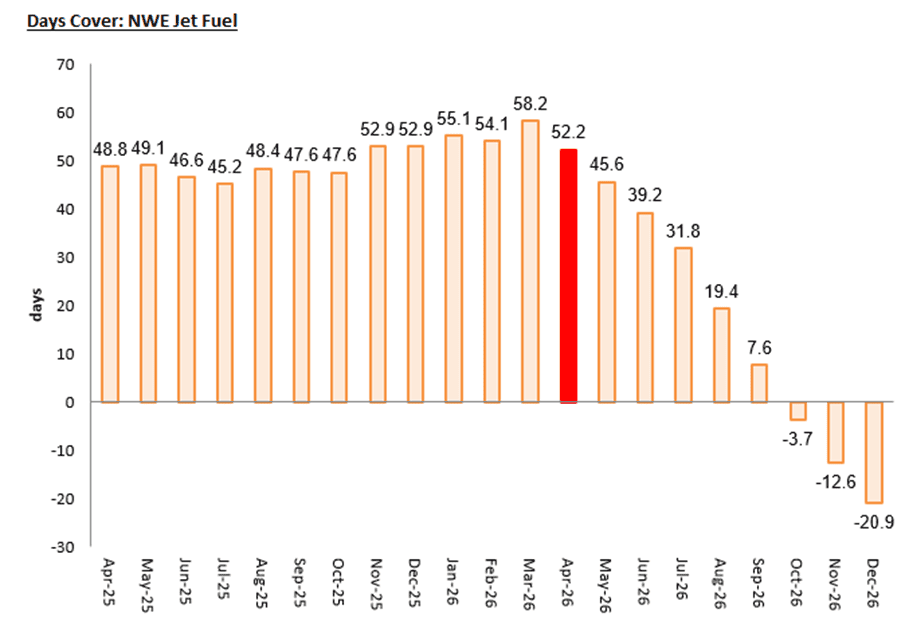

The head of the IEA warned last week that Europe has “maybe six weeks or so” of remaining jet fuel supplies, with possible flight cancellations “soon” if flows remain disrupted. We have already seen the first cancellations. Let’s fact check Birol.

When this war started (50 days ago) we built a War Endurance Model (WEM), and it identified Europe, Australia and New Zealand, smaller Asian economies, and Africa as the regions most vulnerable to jet fuel disruption. Oil on water has bought those regions some time but the"then suddenly" moment has now arrived.

Just so we’re all on the same page:

Kpler S&D Model, Kpler Cargo Tracking

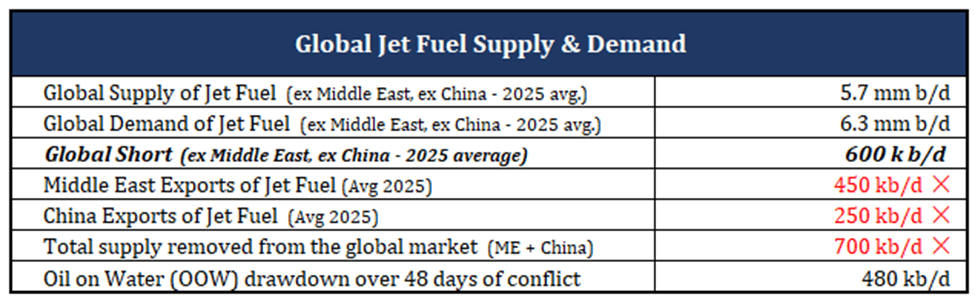

The global supply picture outside the Middle East and China is structurally short. Non-ME, non-China production runs at roughly 5.7 million barrels per day against demand of 6.3 million barrels per day. That 600k b/d structural deficit was historically filled by two suppliers: Middle East Gulf exports of approximately 450k b/d, and Chinese exports of approximately 250k b/d. Both are now effectively zero. The Strait of Hormuz closure has eliminated the Middle East Gulf. China has imposed an export ban. Together, 700k b/d of supply has been removed from the global market in a matter of weeks.

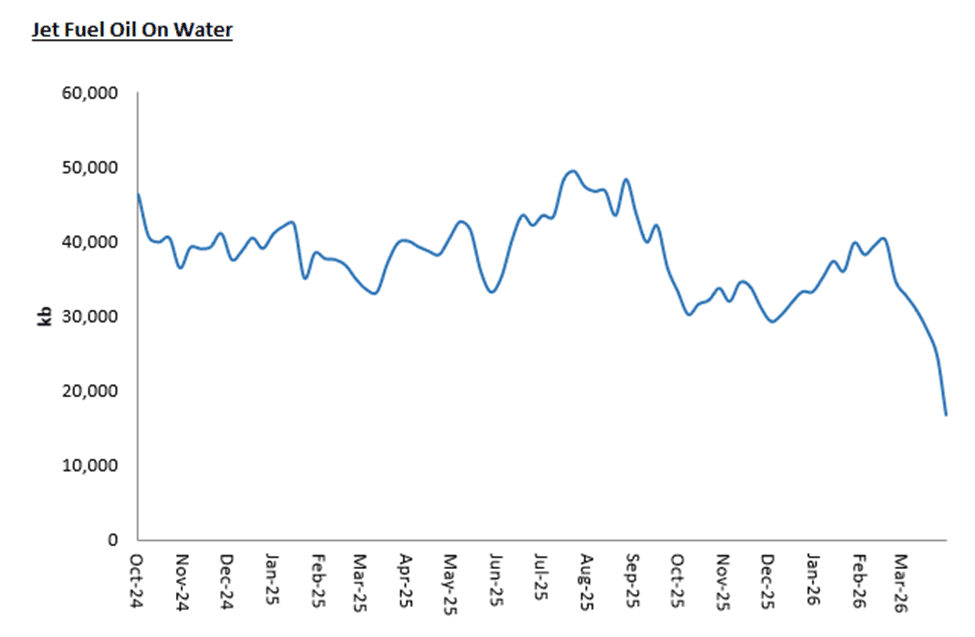

Jet fuel on water absorbed the initial shock. Over the 48 days since the war began, OOW has drawn down at roughly 480k b/d, nearly matching the supply gap, but missed covering it fully by approximately 220k b/d. That shortfall has already pulled roughly 10 million barrels from land-based inventories globally, excluding China and the Middle East. The floating bridge has now been largely crossed.

Kpler Jet/Kero Commodities on Water

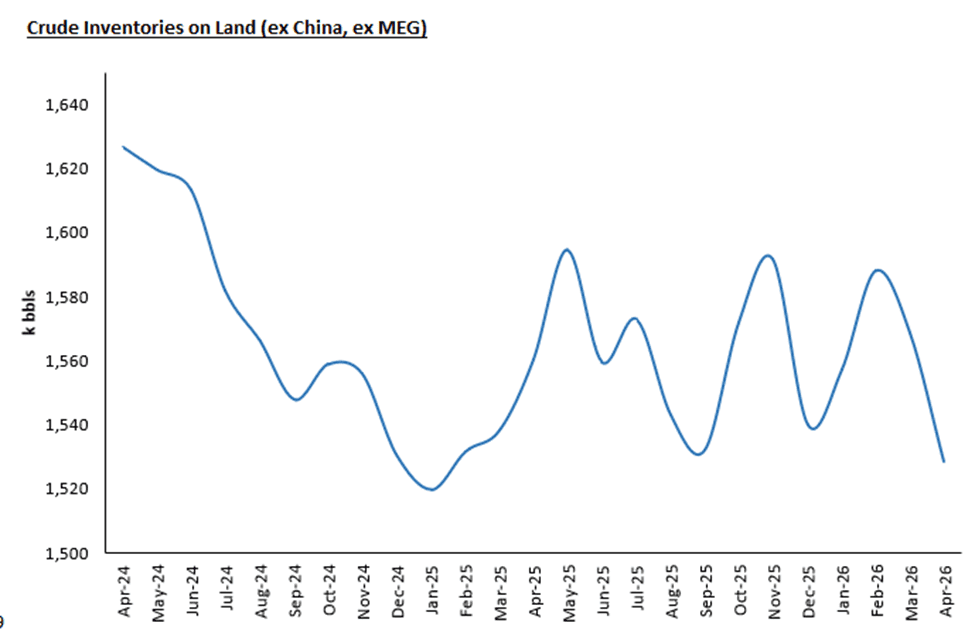

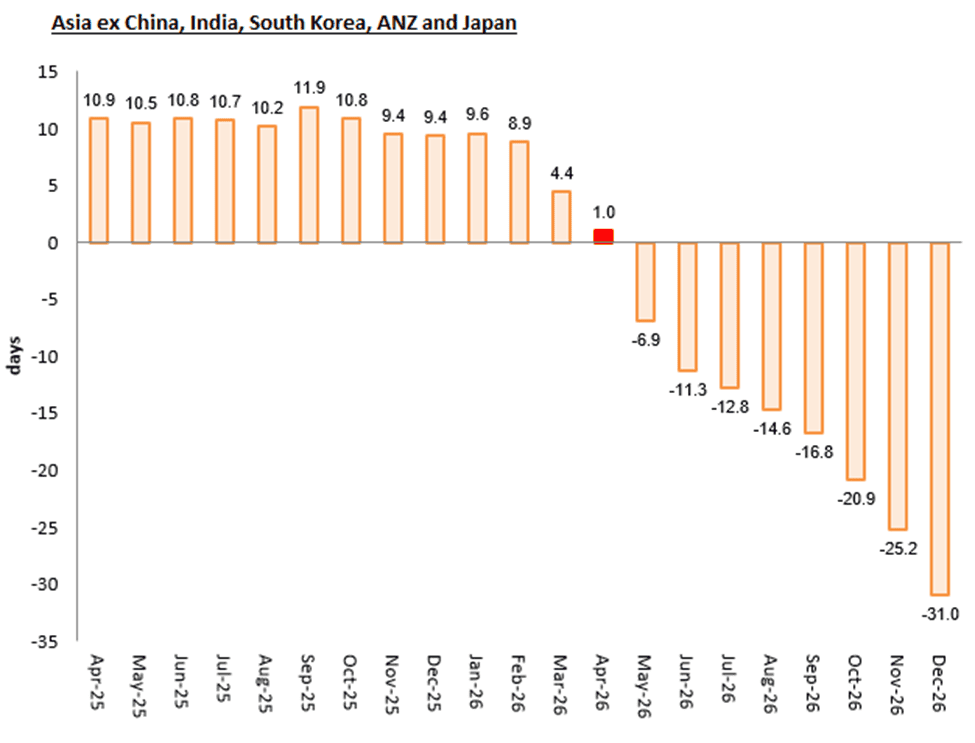

In Asia, crude inventories outside China and India were already 15 to 30 million barrels below the five-year seasonal average before the war began. They are now 64 million barrels below. Arab Light crude has reached $137 per barrel, forcing run cuts of 2.6 to 2.7 million barrels per day in March and April. Governments across 12 of 14 South and Southeast Asian countries have layered on work-from-home mandates and fuel rationing on top of that, engineering a demand collapse of nearly 3 million barrels per day between February and April.

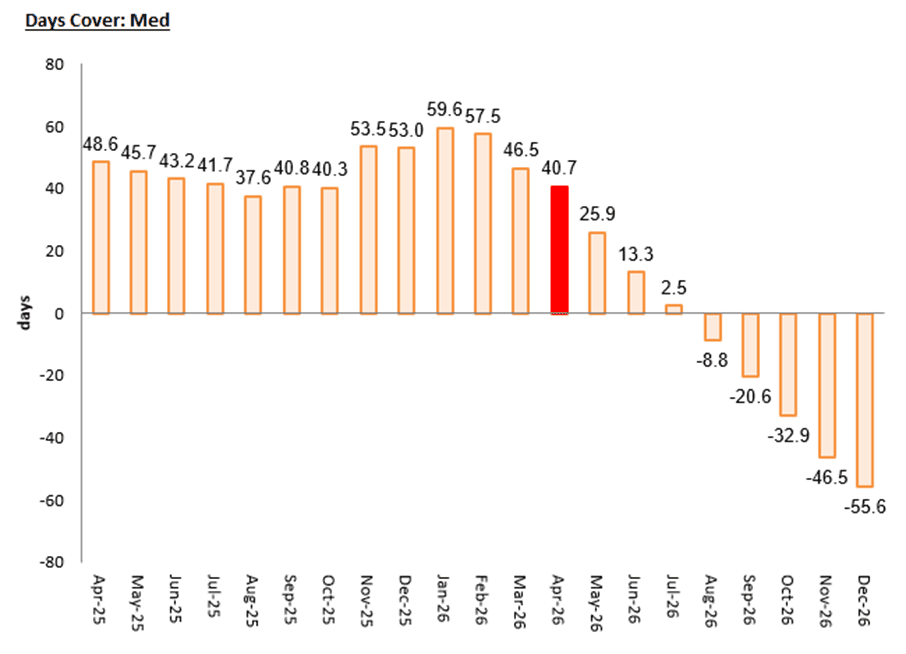

In Europe, the mechanism is different but equally damaging. Sixteen countries have deployed the same subsidy toolkit used in 2022. Germany's €1.6 billion relief package, Spain's VAT cut from 21% to 10%, Italy's excise reductions, Norway's fuel tax cuts, Greece's fuel pass vouchers. In 2022 that worked because supply rerouted. This time supply has been eliminated. The subsidies are preventing refiners from passing through $130 per barrel crude, destroying margins across every configuration. Even the most sophisticated hydrocracker setups in Northwest Europe are losing $10 to $20 per barrel. The European Commission has urged refiners to maintain high utilization, but you cannot legislate away negative margins indefinitely.

This is the quadruple whammy for Jet: Middle East exports near zero, Chinese exports near zero, oil on water exhausted, refinery output falling. The supply pool is draining from every direction at once.

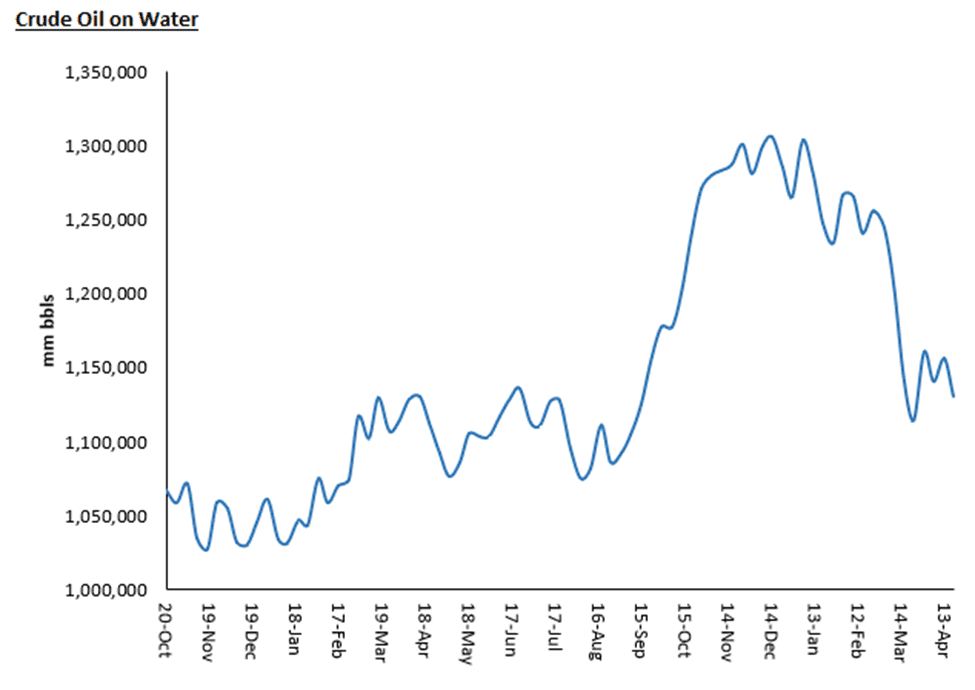

Kpler Crude Oil Commodities on Water

Kpler Crude Oil Inventories - Satellite

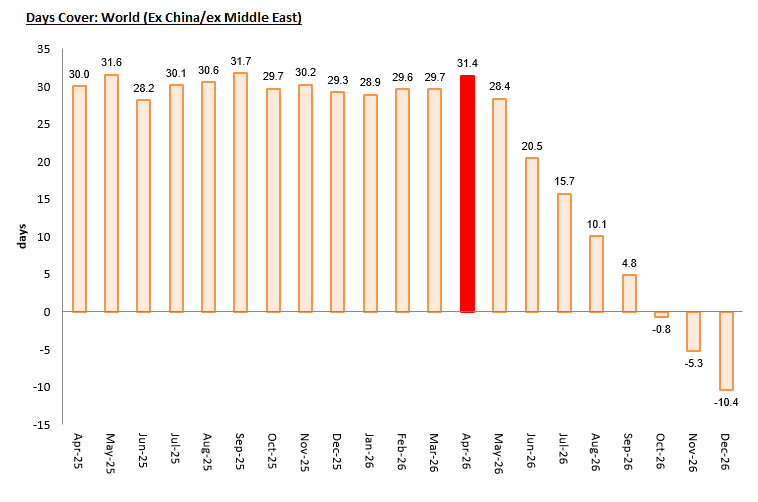

So was Birol right? Does Europe really have only six weeks of jet fuel left?

Europe does have roughly 50 days of jet fuel cover today, a little more than six weeks. This is where Europe typically sits under normal conditions, with steady imports and stable refinery runs. On its own, it does not signal stress. But we are not in normal conditions. For the past several weeks, as the war raged on, oil on water has masked the deficit. Floating cargoes have been bridging the gap left by the loss of Middle Eastern and Chinese supply. That buffer is now largely exhausted. At the same time, refinery runs are beginning to fall as crude availability tightens and bad polices compress margins. The global system is losing both its most flexible source of supply and its ability to replenish inventories at the same time.

This is where the countdown starts. And this part will not be slow. Once inventories begin to draw in a structurally short system, they tend to fall faster than expected, because there is no flexible supply left to stabilize the market.

Kpler

Kpler

Kpler

Kpler

How does the global picture look from here?

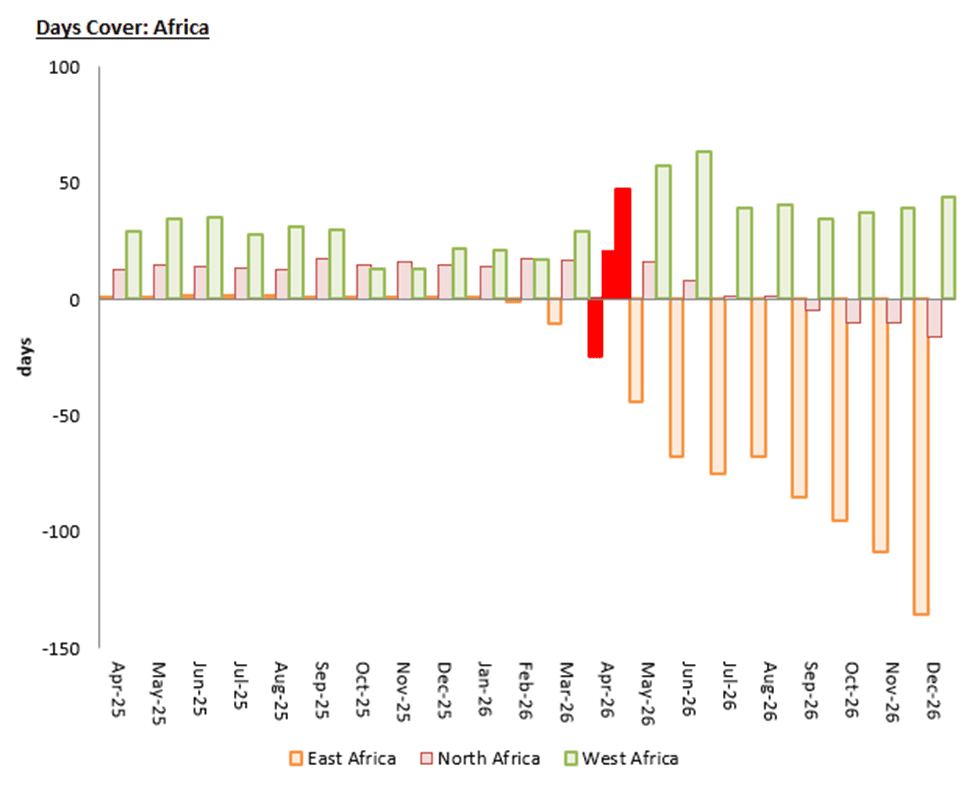

Asia is in acute distress, but through a different transmission mechanism. Direct jet dependency on the Middle East Gulf is minimal, accounting for just 1% of regional inflows, but that understates the exposure entirely. The shock is arriving through crude feedstocks, not product flows. Asian refineries depend structurally on Middle Eastern crude, and with that crude now blocked, run cuts follow automatically. China’s export ban removes a further 300,000 b/d from regional balances, barrels that were effectively the market’s only remaining swing supply. India’s windfall tax on aviation fuel exports, at roughly $50 per barrel, further disincentivizes spot sales. Australia and Thailand are already facing the sharpest near-term demand losses.

Most of the remaining accessible inventory sits in just a few places: the United States, Japan, and South Korea. South Korea has already moved to restrict exports. If European and Asian refineries cut runs deeply enough to create visible shortages, the bid for US export barrels will surge, and domestic prices will follow.

The question is not whether the world runs out of jet fuel. It is how long the system can continue to absorb the shock before something breaks. Europe may still show 50 days of cover on paper, but that number is already decoupling from reality. The buffers are gone, supply is still constrained, and inventories are now doing the work.

Rudi Dornbusch once said, “The crisis takes a much longer time coming than you think, and then it happens much faster than you would have thought.” In jet fuel, that second phase has now begun.

This note outlines potential scenarios and is intended for analysis purposes only.

See why the most successful traders and shipping experts use Kpler