Strong CTA selling amplifies energy sell-off on Hormuz announcement

Stronger CTA selling in Brent is contributing to the ongoing fundamental narrowing of the Brent–WTI spread.

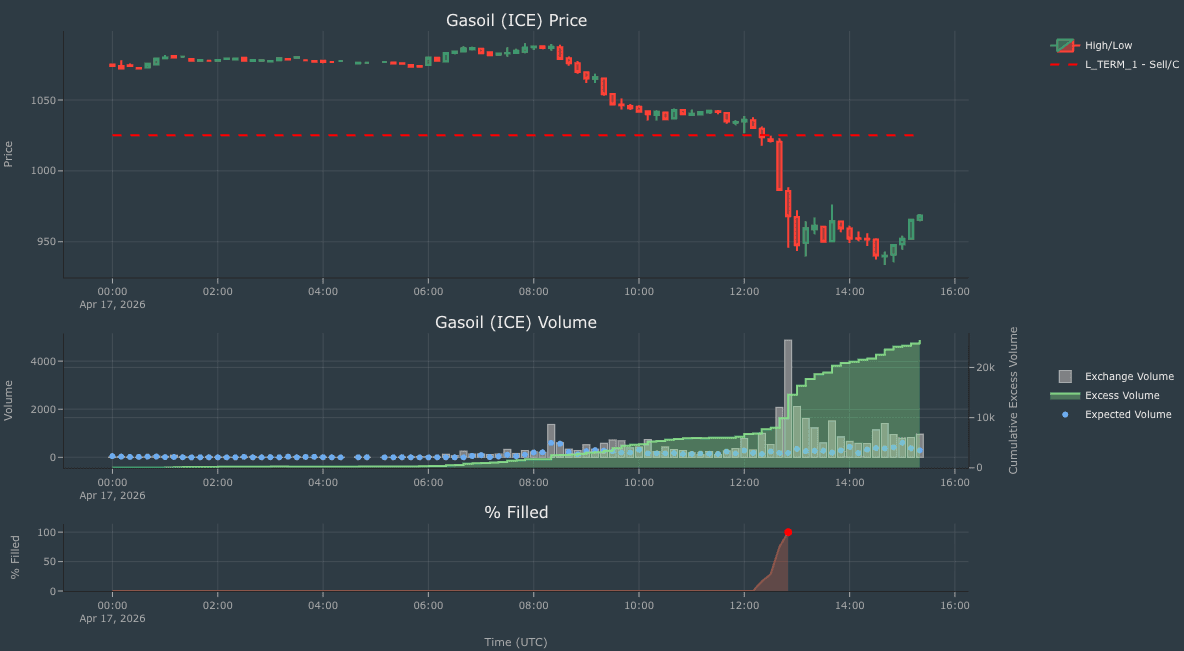

Iran’s declaration that the Strait of Hormuz is “completely open” for the duration of the 10-day Israel–Lebanon truce (from April 17) triggered a broad sell-off across crude and products, with heavy CTA selling amplifying declines in both flat price and time spreads. More aggressive CTA selling in Brent relative to WTI has also contributed to the ongoing fundamental narrowing in the Brent-WTI spread. Physical flows have ticked up over the past 24 hours, but they remain well below historical norms, and a normalization is not our base case. In fact, the Strait remains functionally closed despite diplomatic signaling suggesting otherwise.

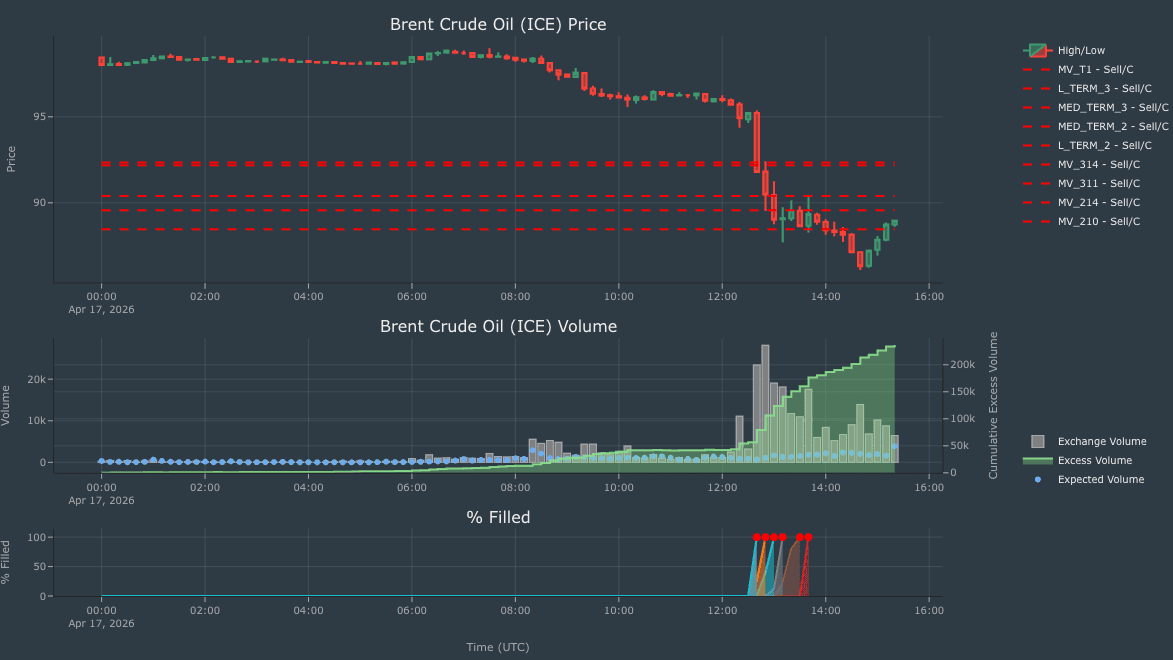

Brent

Trend CTAs sold ~53.5k lots across four strategies, with net positioning dropping sharply from 82% to 27% long within one hour. This accelerated the fundamental sell-off in Brent, which fell by more than $10.00/bbl as of 4pm GMT. Additional CTA sell triggers sit at $82.96/bbl (~17.8k lots combined).

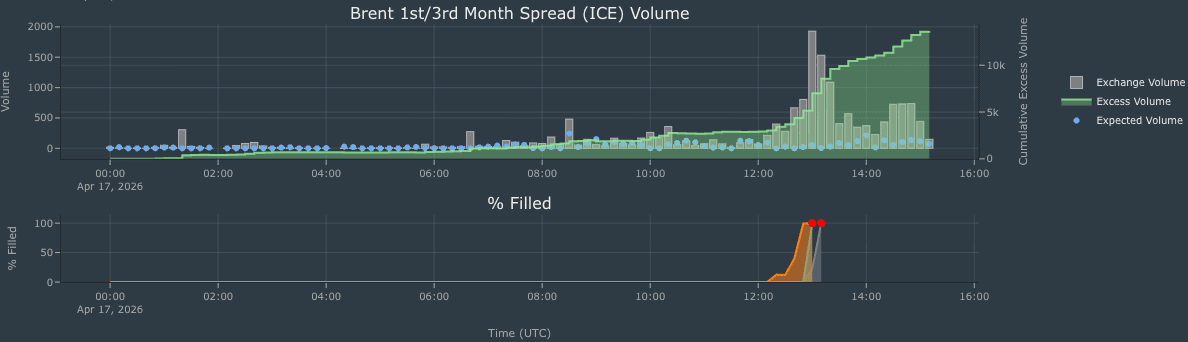

Improved expectations for Hormuz flows also weighed on market structure. Brent M1/M3 declined by ~$2.00/bbl (CTA selling across three strategies, ~2.7k lots), while M2/M3 eased by ~$0.80/bbl (two strategies, ~8k lots).

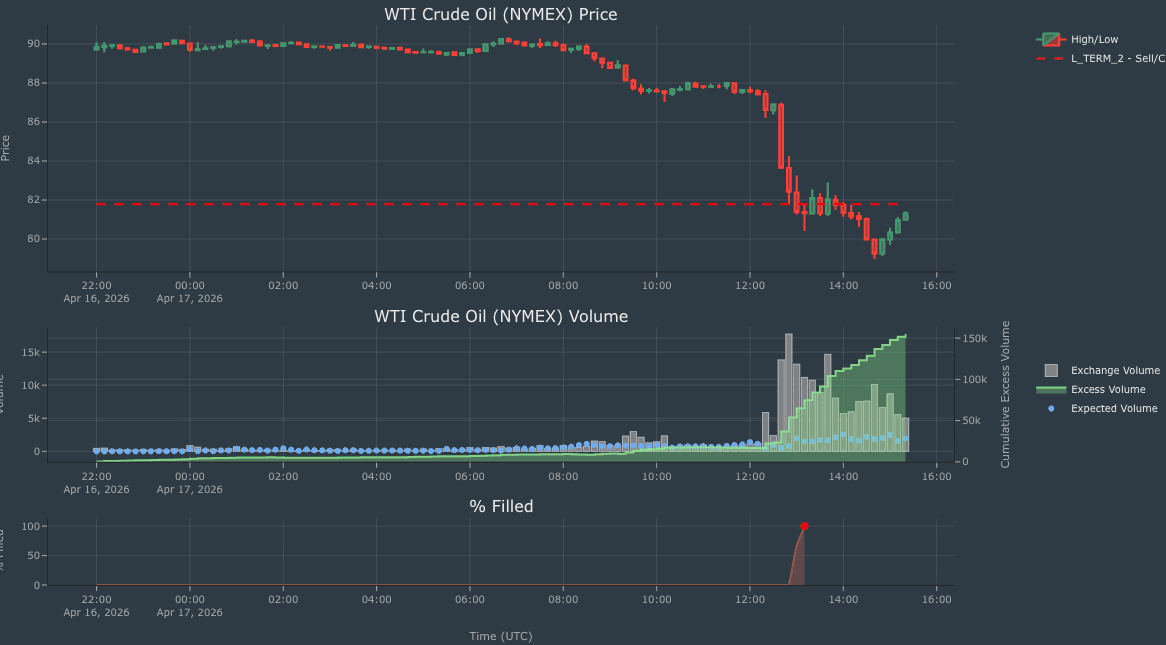

WTI

WTI declined less sharply (~$8/bbl as of 4pm GMT), driving a further narrowing in the Brent/WTI spread, which has been recovering from sub-$10/bbl levels seen last month.

Elevated volatility in WTI since the start of the conflict (e.g. US export ban rumors) has widened CTA thresholds, limiting systematic selling – only one Trend CTA strategy was triggered (~4k lots). Accordingly, Trend CTA net position moved lower from 81% long to 72% long. More limited CTA selling in WTI relative to Brent is thereby also contributing to the narrowing of the Brent-WTI spread.

Additional CTA sell triggers sit at $77.71/bbl (~15.7k lots combined).

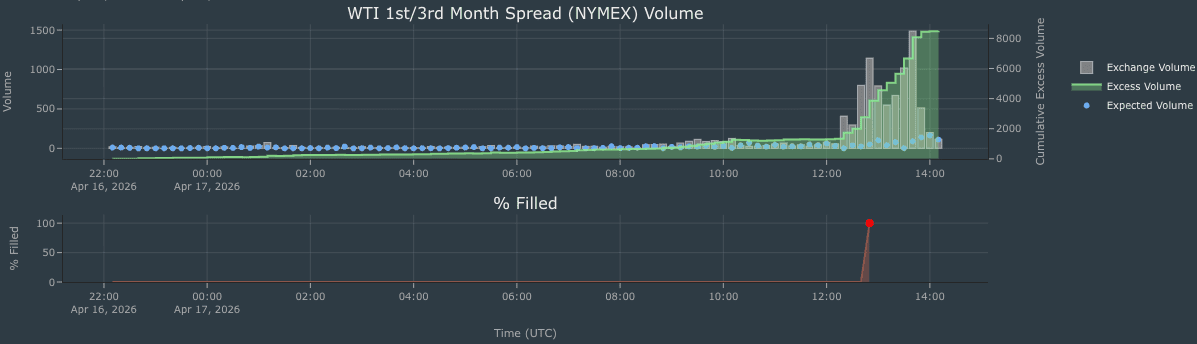

Time spreads also softened, with modest CTA pressure in M1/M3 (~139 lots) and M2/M3 (~324 lots).

Products

European Gasoil reacted more violently than crude, falling by ~$140/t as of 4pm GMT. Heightened volatility over recent weeks as Europe has been scrambling to secure middle distillates, has widened CTA stops, with one Trend CTA strategy selling ~4.5k lots (net position from 82% long to 64% long). CTA-driven downside convexity could accelerate, with three sell triggers between $913.95-914.50/t (~11.2k lots combined).

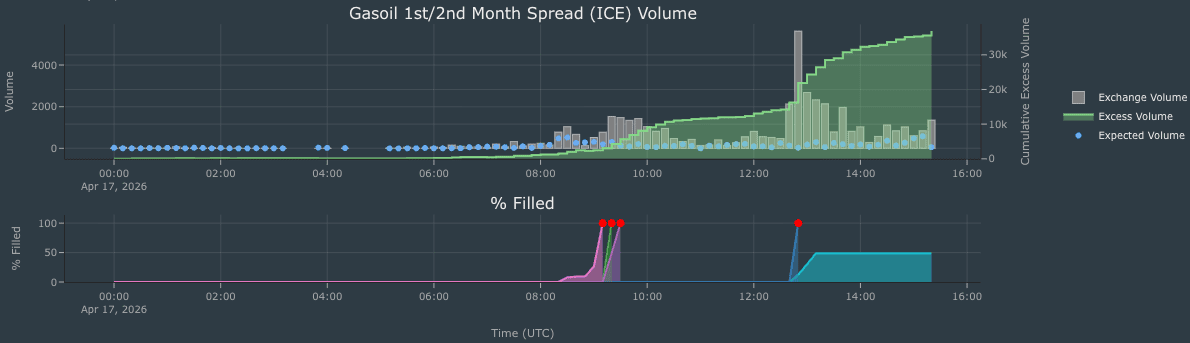

CTA flows also pressured structure:

- M1/M2: -$45/t (~2.5k lots sold across four strategies)

- M1/M3: -$80/t (~1.2k lots sold across three strategies)

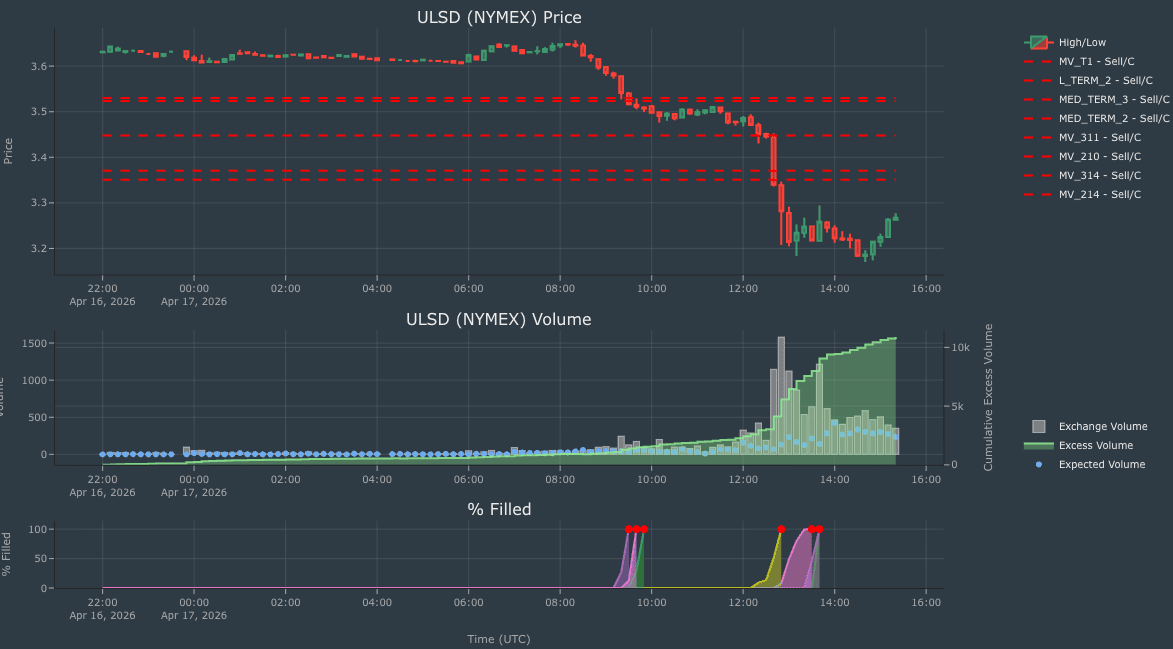

In the US, ULSD declined by nearly $0.50/gal, with ~6.9k lots sold across three Trend CTA strategies amid tighter stops, reinforcing bearish momentum. Trend net position fell from 64% long to 19% long. Renewed CTA selling of ~1.4k lots could occur at $3.13/gal.

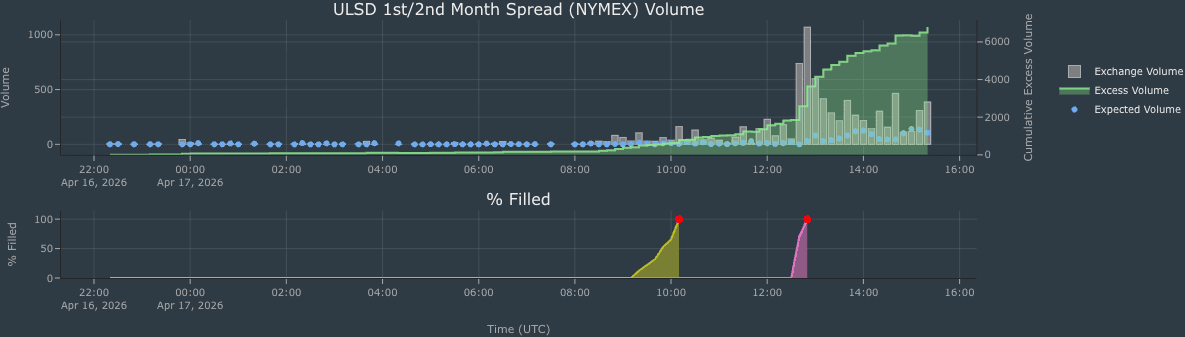

Time spreads weakened in parallel, with CTA selling in M1/M2 (~584 lots) and M1/M3 (~178 lots).

Source (all charts): Kpler Financial Flows, ICE, CME

Kpler Financial Flows

This report draws on Kpler Financial Flows. The full dataset delivers daily and intraday CTA positioning, order stacks, and flow estimates - allowing you to track systematic moves as they develop, rather than after the fact.

- Historical data back to 2014.

- 400+ market tickers across global markets.

- Signals with 0.8+ correlation to key benchmarks.

See why the most successful traders and shipping experts use Kpler

.png)