The Panamax market: A supply-side story

After Pacific market strength that has exceeded seasonal norms, Panamax earnings are set to rebalance as a rise in ships discharging in China boosts supply in the Pacific, and strength in Capesize and Supramax earnings offers upside potential for the Atlantic.

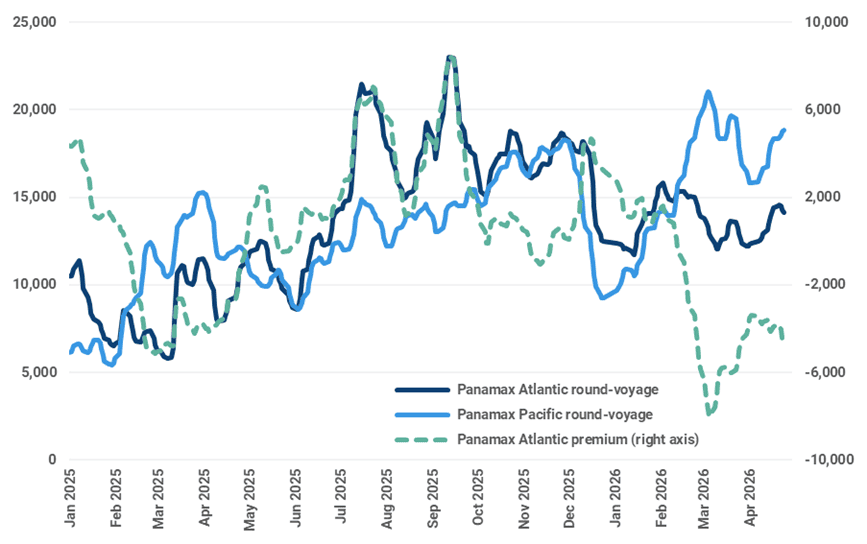

The Panamax Atlantic round-voyage rate has been at a discount of at least $1,500/day to the Pacific equivalent since mid-February, averaging -$4,935/day over the 45 trading days 18 February to 24 April. This is an exaggeration of the typical seasonal trend and compares with an average discount of -$3,896/day over the same period last year.

Panamax Atlantic vs Pacific round-voyage rates: Atlantic outperformance ($/day)

Source: Baltic Exchange, Kpler Insight

The premium on Pacific Panamax earnings reflects tighter vessel supply through February and into April.

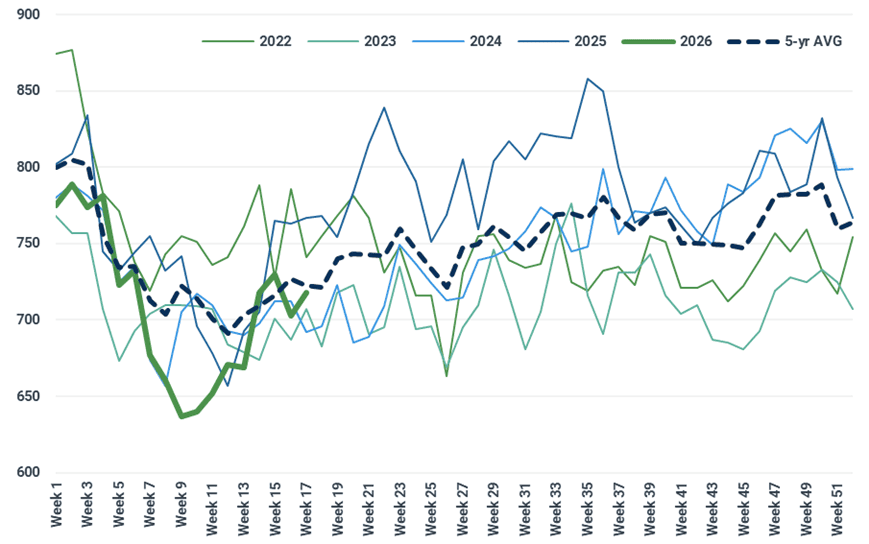

South American grain chartering, Brazilian soybeans and to a lesser extent Argentine corn, has drawn vessels out of the Pacific and into the South Atlantic. Most of these vessels would have been fixed and off the market. At 709, the average number of Panamax ballasters in the Pacific in the first 17 weeks of the year was down from 742 over the same period last year and below a five-year average of 733.

Panamax (68-99,999 dwt) ballaster availability in the Pacific was sharply lower y/y in February and March (Vessel count)

Source: Kpler Insight

This is a seasonal trend that was exaggerated this year by a combination of higher Brazilian soybean exports and port delays.

Brazil shipped an exceptional 15.67Mt of soybeans in March, Kpler data show, and April is on track to be similarly strong. We expect Brazil to export 112.92Mt of soybeans in the 2025/26 trade year (September-August), up from 101.91Mt in 2024/25. More than three-quarters of these cargoes will go to China.

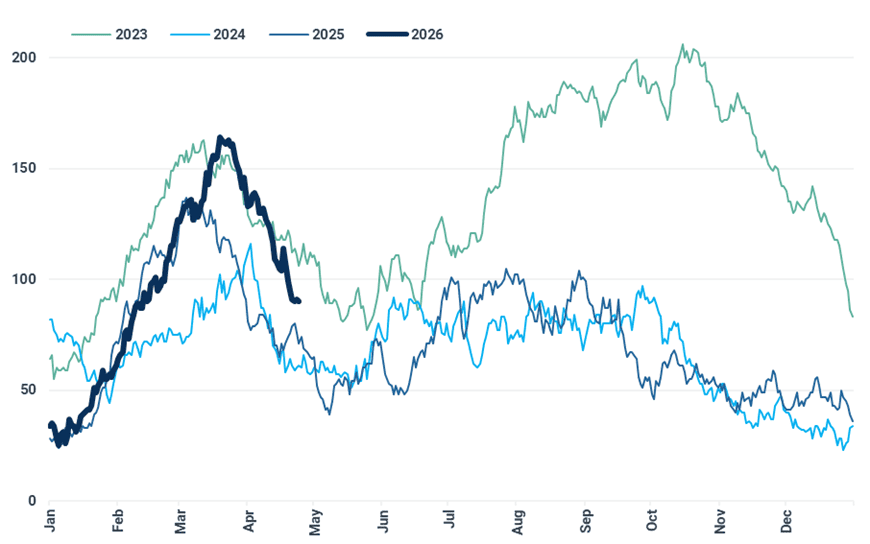

Meanwhile, phytosanitary checks briefly interrupted Brazilian soybean loadings in March and led to a buildup of Panamaxes outside the country’s ports. This tied up vessels in the Atlantic, tightened supply across the global fleet, and supported earnings.

Brazilian grain/oilseeds load port congestion spiked in March (Count of vessels)

Source: Kpler

However, this picture has now changed. Congestion at Brazilian load ports is clearing, and with greater numbers of ships arriving to discharge soybeans in China, more than 2.8 Mt/week was discharged over 6-19 April, ballaster supply in the Pacific basin is rising. This will put downward pressure on earnings.

We expect the Pacific Panamax earnings premium to be eroded through the rest of the second quarter.

While downward pressure on Pacific earnings as supply in the basin increases will be key, we also see upside potential for Atlantic Panamax earnings. The Capesize Atlantic round-voyage rate is at an unsustainably large three times the Panamax equivalent. Meanwhile, an implied Supramax Atlantic round voyage (average of S4A and S4B) is 36% higher than the Panamax equivalent. We therefore see an opportunity for Panamaxes to gain market share against both vessel types on coal and grain trades, respectively. The economics of splitting Capesize stems onto Panamaxes have been improved by an easing in bunker prices from their March highs, although they remain well above their pre-war levels. Lower bunker prices will also improve the economics of ballasting between basins.

See why the most successful traders and shipping experts use Kpler

Get real-time market intelligence on how global disruptions are reshaping dry bulk trade