Aluminium value chain tracking: Multi-modal logistics approach of bagged alumina imports amid Hormuz crisis

GCC alumina climbed to 0.56Mt in May, driven by a multi-modal logistics approach of bagged alumina imports. The approach is costly but remains workable amid elevated aluminium prices. Even if shipping via the Strait of Hormuz resumes in June, alumina and bauxite imports are unlikely to rebound to pre-war levels immediately, as halted smelting and refining capacity cannot be brought back online soon.

High aluminium and low alumina prices sustain costly bagged alumina imports into the GCC

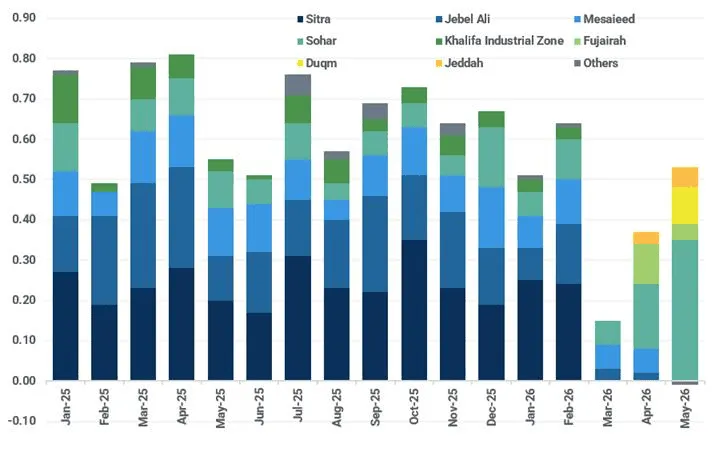

Seaborne alumina imports into GCC countries, excluding intra-regional flows, rose to 0.52Mt in May, recovering significantly from March and April levels, although still below the previous five-year average. With the Strait of Hormuz remaining effectively closed, Gulf aluminium producers are increasingly adapting to the status quo through costly but workable alternative alumina supply routes: importing bagged alumina through ports outside the Strait, primarily Sohar, Duqm and Fujairah, before distributing material via trucking and intra-GCC shipments.

GCC alumina imports by destination ports (Mt)

Source: Kpler

Based on our assessments, around 0.44Mt of alumina is estimated to have ultimately reached smelters in the Gulf in May, namely Bahrain’s Alba, Qatar’s Qatalum and the UAE’s Al Taweelah, after adjusting for Oman’s Sohar smelter's typical import requirements prior to the conflict. The adjustment uses 0.52 Mt to deduct 0.08 Mt, which is the 12-month average of imports by the Sohar aluminium smelter before the US/Israel-Iran war broke out.

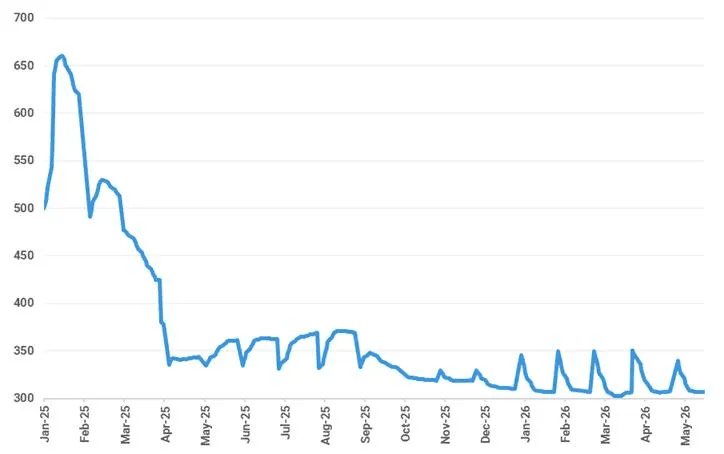

However, this alternative supply chain comes at a considerable cost. At least 0.22Mt of the imported alumina was suspected to have been bagged in China, though originally sourced from Australia and Indonesia, adding further logistical complexity. Preliminary estimates suggest that combined freight, handling, re-export, and trucking costs range from $100-160/t for these cargoes, representing a significant share of the FOB Australia alumina price, which has traded between $300-350/t since late 2025.

FOB Australia alumina price ($/t)

Source: MarketView, Kpler Insight

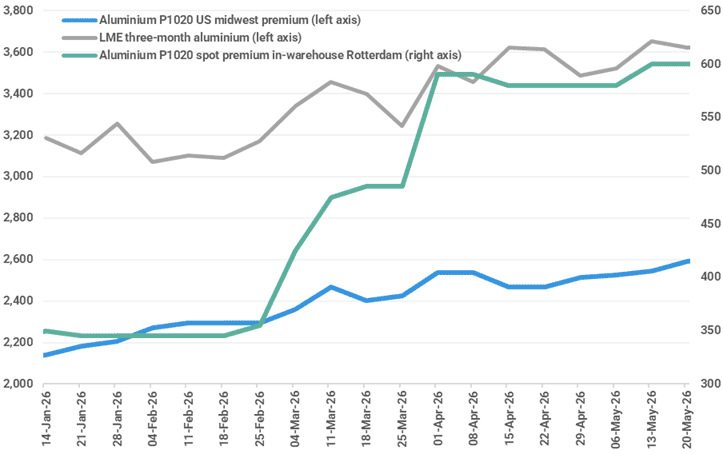

What makes these arrangements economically sustainable is the strength of aluminium prices. The three-month LME aluminium contract reached a fresh four-year high of $3,672.50/t on 26 May, while regional premiums in the US, Europe and Asia climbed to record levels. Elevated margins, driven by elevated prices, are effectively allowing Gulf smelters to absorb sharply higher input and transport costs.

LME aluminium, US Midwest premium and Rotterdam premium ($/t)

Source: MarketView, Argus, Kpler Insight

Alba’s latest results underline this dynamic. The company reported 312,563 tonnes of aluminium sales (-17% y/y) and $336 million of EBITDA (+90% y/y) for Q1 2026. With the average LME price so far in Q2 ($3,565/t) running 11.50% above the Q1 level ($3,198/t), profitability per tonne is expected to remain robust despite higher logistics costs, rising gas prices, lower operating efficiency and the dilution of fixed costs across reduced output.

Hormuz reopening unlikely to deliver immediate recovery for alumina and bauxite imports

Prospects for a reopening of the Strait of Hormuz are improving, with reports suggesting that Washington and Tehran could restore full maritime traffic within weeks if a broader ceasefire agreement is reached. However, even if shipping routes reopen in June, the full recovery of alumina and bauxite imports via Hormuz is unlikely to be immediate, as partially or fully suspended smelting and refining capacity across the Gulf will require time to restart.

According to the International Aluminium Institute (IAI), GCC countries produced 0.33Mt of primary aluminium in April. Given the region’s installed smelting capacity of 6.23Mtpa, equivalent to around 0.52Mt per month, this implies an operating utilisation rate of approximately 64%, sharply below the 97–98% levels recorded a year earlier. The decline has been driven primarily by disruptions at Alba, Qatalum and EGA’s Al Taweelah smelter, all of which have partially or fully curtailed output following the closure of Hormuz and subsequent Iranian attacks.

GCC smelters and their implied utilisation rate in April (Mt)

Source: Companies’ results, IAI, Kpler Insight

Even in the case of a full Hormuz reopening in June, the Gulf’s aluminium sector faces a lengthy and uneven recovery, as the disruption has extended well beyond logistics:

- EGA’s Al Taweelah Smelter

- The 1.50Mtpa Al Taweelah smelter has remained fully offline since Iranian strikes on 28 March triggered an uncontrolled, system-wide shutdown. EGA expects a complete restoration of production to take up to 12 months, implying a full recovery only by April 2027. While reopening Hormuz would accelerate the delivery of critical repair materials, including heavy machinery, replacement transformers and structural steel, the process of restarting more than 1,200 reduction cells remains technically complex and time-consuming. Even if initial pot restarts begin by the end of Q3 2026, restarting all cells is likely to require an additional two quarters, based on comparable industry cases.

- Alba Smelter

- Bahrain’s 1.60Mtpa Alba smelter implemented a controlled shutdown of reduction lines 1–3, equivalent to around 19% of total capacity. As these pots remain structurally intact, the company is expected to restart them relatively quickly using standard electrical preheating procedures, potentially restoring these lines within a quarter. However, capacity affected by the subsequent uncontrolled shutdown following the Iranian strikes may take considerably longer to recover. While the extent of the damage has not been disclosed, our analysis based on IAI’s April GCC production data indicates that around 15-20% of capacity has been further impacted. Nevertheless, Alba’s prior experience with rapid “crash-start” recovery techniques, demonstrated by a full recovery within 44 days after an 8-hour total power blackout in November 2024, suggests a faster overall recovery than at Al Taweelah.

- Qatalum Smelter

- Qatar’s 0.64Mtpa Qatalum smelter presents the least complex recovery scenario. The facility carried out a highly controlled shutdown of 40% capacity in March following warnings from QatarEnergy regarding fuel shortages. Importantly, the smelter sustained no direct physical damage from Iranian attacks. Assuming full gas supply is restored in June or July, Qatalum is expected to restart dormant pots relatively smoothly and could potentially return to normal full commercial operations by Q4 2026.

Scenario for capacity recovery if Hormuz fully reopens in June 2026 and alumina supply is sufficient

Source: Companies’ results, Kpler Insight

Based on the analysis above, if Hormuz fully reopens in June (at least for the aluminium value chain), the annual supply loss from three primary aluminium smelters could reach around 1.70Mt. In theory, most of the losses could be offset by new capacity or output expansion in China and Indonesia. However, whether all planned new capacity in Indonesia can come online as scheduled remains uncertain, and the closure of Mozal and lower output from Grundartangi, as well as potential higher global demand for aluminium on a more sufficient energy supply, still point to an over 1Mt supply deficit in 2026. Therefore, even if Hormuz opens soon, aluminium prices are expected to remain elevated at near-four-year highs throughout the remainder of 2026.

In alumina, the recovery of GCC refining capacity is expected to also be gradual, though, in theory, considerably faster than the restart of aluminium smelting operations, but actual progress could be impacted by the market environment:

- The 2.40Mtpa Al Taweelah refinery avoided the severe thermal damage suffered by aluminium reduction pots during the conflict. Once bauxite imports via Hormuz stabilise, the refinery should be able to restart the Bayer process relatively quickly. However, restoring operations still requires careful stabilisation of the caustic liquor circuit and management of sodium oxalate crystallisation, implying several weeks of technical recalibration. Under an orderly restart scenario, full capacity could likely be restored within a quarter.

- Guinean bauxite remains the preferred feedstock for Al Taweelah, though imports have been largely absent since late 2024 due to disputes between subsidiary GAC and Guinean authorities, with volumes from Australia and Ghana serving as alternatives. However, EGA’s agreement with the Guinean government in early May has improved the prospects for restoring bauxite imports. The deal resolves disputes linked to the suspension of GAC’s activities and includes renewed supply agreements between EGA and CBG. Even so, brewing bauxite export restrictions in Guinea, which could affect all trade partners, continue to cloud the outlook for long-term supply stability.

- A further complication is the mismatch in restart timelines between the refinery and the downstream aluminium smelter. Since the Al Taweelah smelter is unlikely to return to full production for a much longer period, EGA may have limited incentive to rapidly restore full alumina refining capacity. With alumina prices at multi-year lows, importing alumina directly through Hormuz could prove more economical in the near term, potentially delaying the full recovery of refinery operations and associated bauxite imports.

Forecasts dataset

Source: Kpler Insight

See why the most successful traders and shipping experts use Kpler