From supply shock to demand anxiety: China’s demand takes centre stage in the crude market

As the US-Israel war against Iran passed the 100-day mark, fears of extremely high oil prices stemming from Middle East supply losses have quickly waned. While the market remains broadly balanced for now, attention is increasingly turning to the possibility of a minor oversupply in Q3 as additional Middle East supplies emerge and Chinese buying remains subdued.

Market & Trading Calls

- Bearish Dubai time spreads as rising Persian Gulf exports routed through reduced-visibility channels are adding more prompt barrels to the market than expected.

- Bearish Middle East crude premiums: Oman and Murban premiums are likely to remain under pressure as additional Middle East-origin barrels emerge and buyers gain optionality.

- Bearish prompt crude balances until Chinese buying returns: China's ability to draw down inventories at roughly 1 mbd for months reduces the urgency to procure seaborne crude. With refinery runs weak, product inventories elevated, and imports likely to remain near recent lows, China remains a passive buyer, leaving the market vulnerable to a minor Q3 oversupply.

In previous reports, we argued that the oil market had managed to settle into a tight balance through inventory drawdowns, rerouted exports, higher Atlantic Basin supplies and demand destruction. As these balancing mechanisms continue to hold, rising flows from the Middle East and the potentially prolonged absence of Chinese procurement demand risk tipping the market into a slight oversupply in Q3.

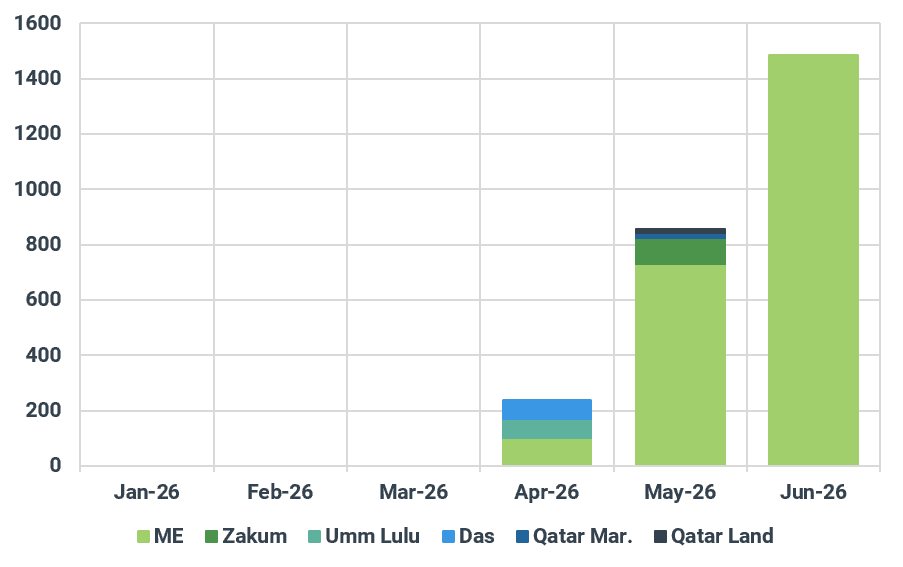

While a limited number of vessels carrying non-Iranian crude continue to transit the Strait of Hormuz after receiving approval from the IRGC, Persian Gulf producers increasingly rely on reduced-visibility shipping practices to maintain supply flows through the waterway and market cargoes via STS transfers near Fujairah and Sohar. Kpler identified 858 kbd of such exports in May, surging from 237 kbd in April, with volumes continuing to trend higher so far this month. While it remains difficult to pinpoint the exact origins of these cargoes, they are understood to be largely linked to the UAE, with the remainder likely associated with Iraq and Kuwait.

While the market is still trying to gauge the scale of these previously unexpected flows, ADNOC sold at least 13 mb of June-August loading Upper Zakum, Das and Umm Lulu cargoes to refiners in China, South Korea, Malaysia, India and Japan, as well as to a trading house, according to market participants. Shortly after closing those deals, ADNOC issued another tender this week to sell cargoes originating from within the Persian Gulf for the same loading period, suggesting the company expects these flows to be sustained. As a result, the Dubai M1-M3 spread narrowed to $5.8/bbl on Monday from around $8/bbl in late May, while Oman and Murban premiums against Dubai swaps also eased amid rising Persian Gulf supplies.

Gulf of Oman crude/co exports by grade (as of June 8), kbd

Source: Kpler

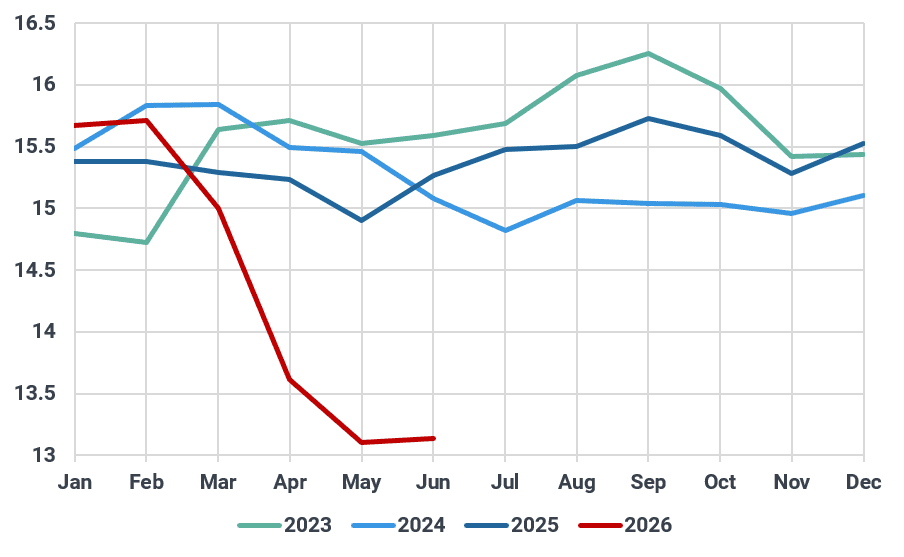

The softening physical market also reflects growing concerns over Chinese demand. In the West of Suez market, some June-loading cargoes remain unsold despite the approaching loading window, reflecting subdued buying interest, particularly from China, where imports and refinery run rates have fallen sharply, yet oil inventories continue to hold up well. With China’s seaborne crude imports in June and July likely to remain near May’s low level of around 7 mbd, and refinery run rates expected to stay at about 13 mbd as state-owned refiners keep some units under maintenance while independent refiners cut production amid weak margins and the prospect of tighter Iranian crude supplies, the country is expected to see inventory drawdowns of around 1 mbd over the next two months.

China refinery runs, mbd

Source: Kpler

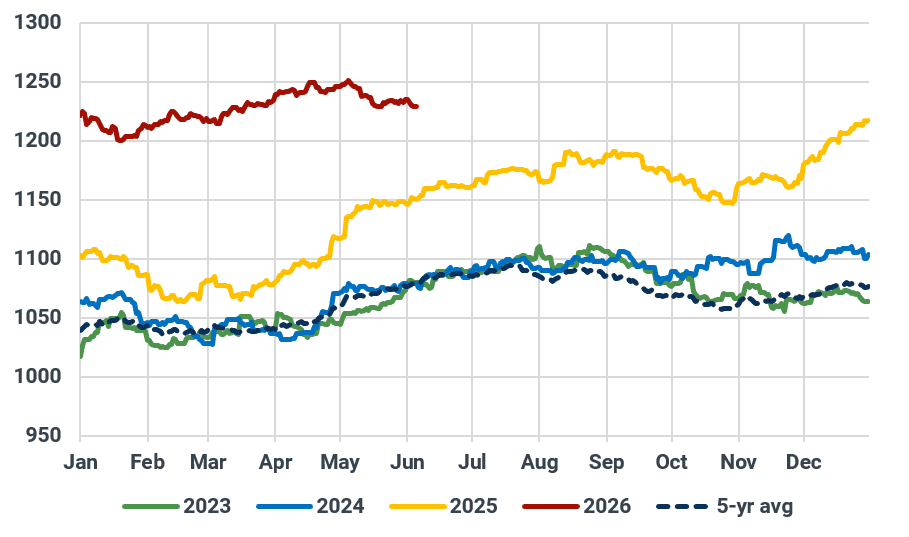

China currently holds 299 mb in refinery stockpiles and a further 507 mb of crude oil in commercial storage. Assuming refiners need to maintain inventories equivalent to 15 days of demand and commercial storage utilization does not fall below 30% of capacity, China could sustain 1 mbd inventory drawdowns until Q2 next year without tapping its SPRs.

Of course, Beijing is unlikely to allow such an extreme scenario to unfold, as it would jeopardize the country’s energy security, and the global economy would likely slip into recession well before then. Nevertheless, the large inventory cushion makes China a swing buyer in the crude market in the near term, as it can afford to stay on the sidelines and wait for oil prices to plunge before re-entering the market.

China onshore crude oil inventories, mb

Source: Kpler

What worries the market more is the destruction of China’s refined product demand driven by higher oil prices — with retail gasoline and diesel prices up around 30% since the war began — as well as the continued energy transition. Without clear visibility into the country’s refined product inventories, some China-based consultancies estimate that commercial gasoline stocks are still building, while diesel inventories have only recently retreated from multi-year highs, even as production has been reduced by around 1.22 million tonnes since early March.

That said, unless Beijing eases refined product export restrictions or oil prices pull back significantly enough to revive demand, China’s commercial gasoline and diesel inventories are likely to remain slow to deplete, limiting refiners’ appetite for crude procurement.

With ex-China refinery throughput in Asia-Pacific now close to pre-war levels and demand in the West of Suez market showing limited upside, ongoing US SPR releases and additional flows from the Persian Gulf are tilting the prompt market balance toward a slight oversupply in Q3. As additional Middle East supplies continue to emerge, the key questions for the market are becoming not only how much supply is lost, but also when Chinese buying returns.

See why the most successful traders and shipping experts use Kpler