Strong US stock draw reinforces bullish narrative

Crude prices fell slightly early Monday morning amid improved US-Iran diplomacy and renewed tariff-driven macro pressure, but a sharp 9 Mbbls US inventory draw and elevated refinery runs are keeping the physical market tighter and sentiment supported even as global balances are set to lengthen in April.

Market & Trading calls:

- Geopolitical de-escalation and tariff uncertainty are weighing on prices, but tighter US crude balances are limiting the downside.

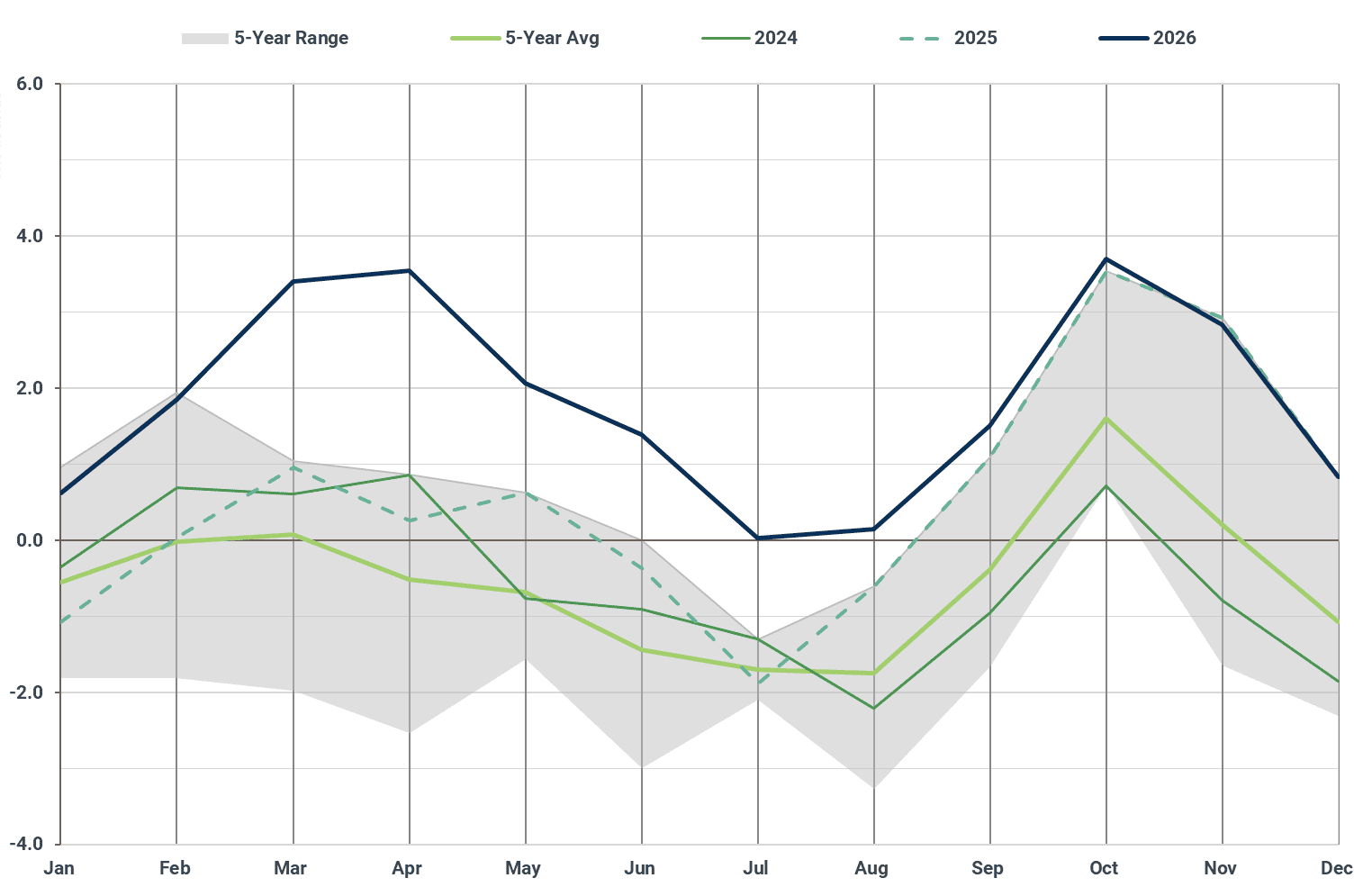

- Near-term direction hinges on this week’s US-Iran talks, but the market is heading into one of the year’s longest months with global balances expected to average a 3.5 Mbd surplus in April.

Crude prices are softer early Monday as geopolitical risk premia unwind following a partial de-escalation between the US and Iran. The two sides are expected to resume nuclear talks in Geneva this Thursday, signaling that Tehran is putting forward more serious proposals—potentially including steps to dilute its stockpile of highly enriched uranium. The macro backdrop is also weighing on the complex, with trade uncertainty rising again after the Trump administration floated a 15% blanket import tariff, a rapid pivot after the Supreme Court struck down the prior emergency tax framework.

Global crude and condensate balance, Mbd

Source: Kpler

Even so, the pullback is running into a supportive physical backdrop. Spot balances remain tight enough to underpin sentiment and blunt concerns around a well-supplied global market, even as the crude and condensate balance is set to swing deeper into surplus—approaching one of the longest months of the year at an estimated 3.5 Mbd surplus in April (up ~100 kbd versus our initial estimates in early February).

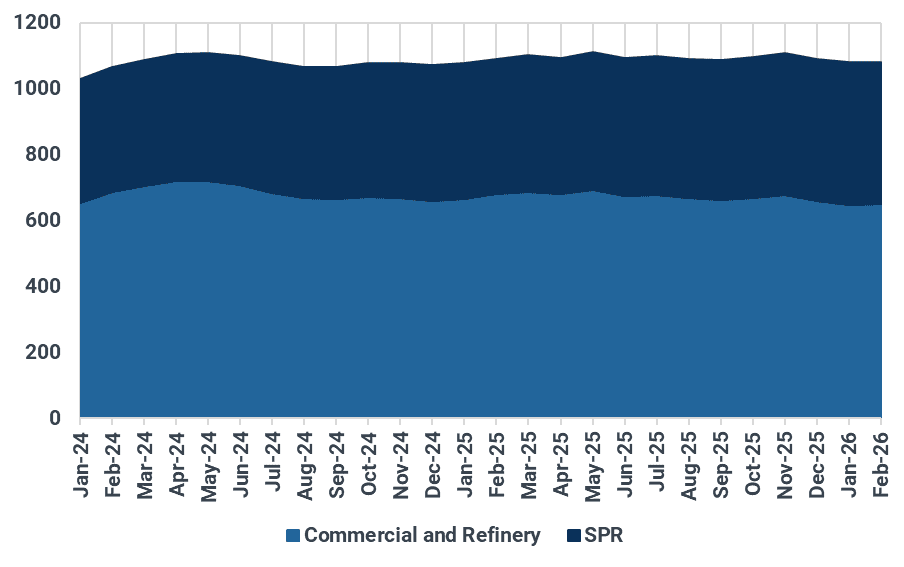

US crude stocks tightness lifts sentiment

While global crude stocks are currently hovering at record highs of over 3,500 Mbbls, outside of China, crude inventories remain constructive. In fact, stocks in the US and EU-27 combined are currently hovering at 1,080 Mbbls, down ~25 Mbbls from November 2025 (see chart below).

EU and US crude stocks by tank type, Mbbls

Source: Kpler

In the US, the signal is unequivocally constructive: inventories fell by roughly 9 Mbbls last week, defying the typical seasonal tendency to build as refinery maintenance takes hold. Refinery demand remains the key driver, with runs holding around 16.4 Mbd and utilization near 91%, supported by favorable heavy sour crude economics. Wider heavy sour differentials are improving feedstock value and incentivizing refiners to keep units running harder than seasonal norms.

That operating strength is especially notable given the closure of two major facilities last year and late-January weather disruptions—yet the latest EIA weekly data for January and early February 2026 still shows utilization tracking roughly 5 percentage points above typical seasonal averages.

Looking ahead, absolute runs may ease later in 2026 as maintenance cycles and planned closures bite, but as long as margins and heavy-feedstock economics stay favorable, operating rates look set to remain elevated—tightening inventories even against record-high domestic production of 13.7 Mbd, providing further support to overall sentiment, painting a bullish narrative as we approach the tighter summer months.

Want market insights you can actually trust?

Kpler delivers unbiased, expert-driven intelligence that helps you to track critical crude oil market developments for your own analysis. Our precise forecasting empowers smarter trading and risk management decisions.

Unbiased. Data-driven. Essential. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

.jpg)