Sulphur & sulphuric acid in 2026: The feedstock crisis cascading through copper, nickel & fertilisers

Three simultaneous shocks - a Strait of Hormuz closure, China's sulphuric acid export ban, Russia's sulphur export ban, and a structural Asian supply deficit - have converged to produce the most acute sulphur supply disruption in a generation. Kpler's vessel-level data tracks the downstream fallout in real time.

The MEG cage: +600K tonnes and counting

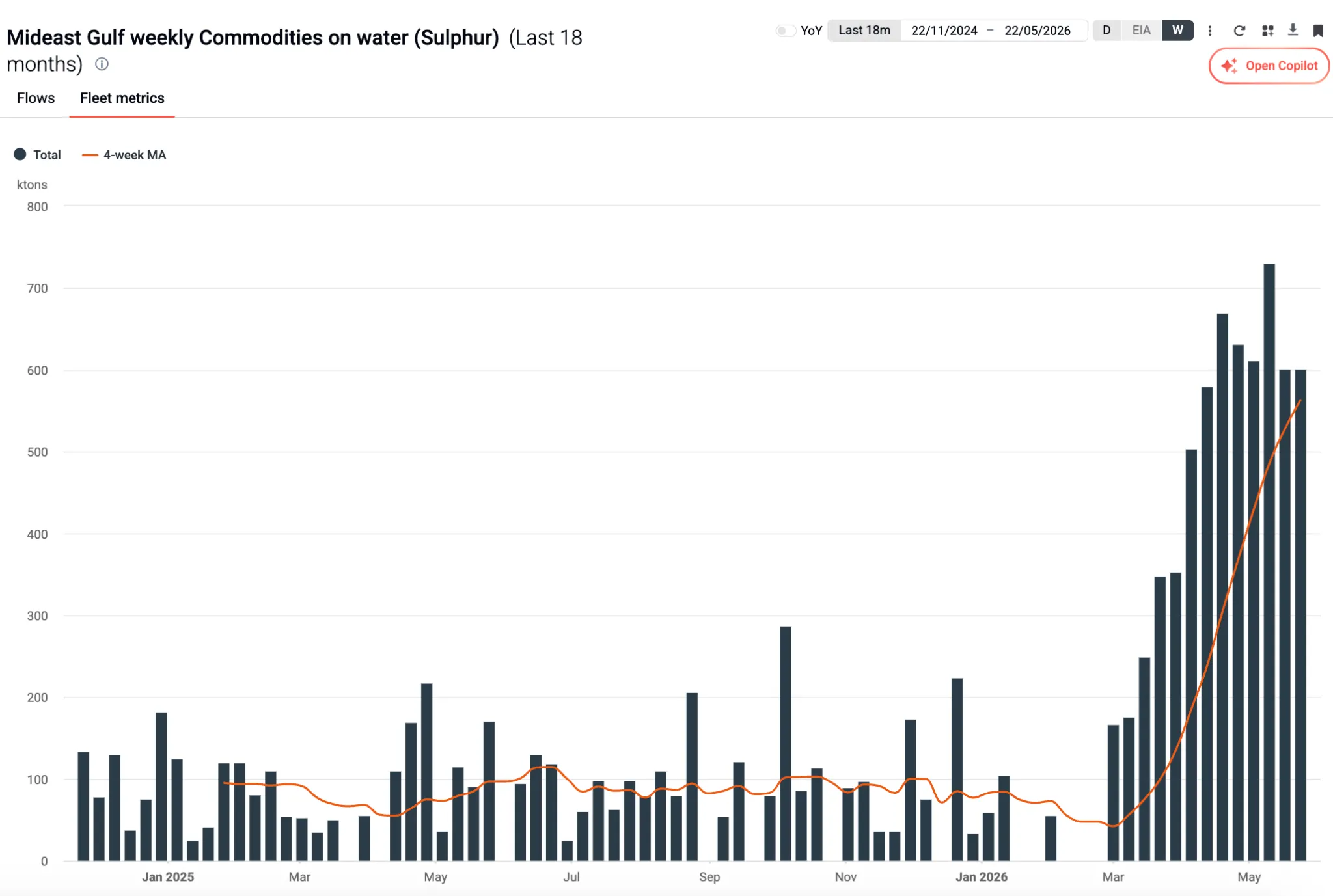

On 28 February 2026, the Strait of Hormuz closed to commercial dry bulk traffic. The impact on sulphur markets was immediate and measurable: Kpler tracked the cargo build-up in the Mideast Gulf in near-real time as loaded vessels queued with no exit.

Sulphur caged in MEG, weekly build-up since 28 Feb 2026

Source: Kpler fleet metrics, May 2026

By the first peak in April, +600kt sulphur was stranded across fertiliser-laden vessels in the Gulf. Global sulphur exports fell 45% below end-February levels. The UAE became the only MEG country still able to move sulphur via the Strait - Kpler confirmed 3 UAE-sourced transits in May 2026.

A critical caveat: Qatari, UAE, and Kazakh supply tonnes are substantially committed under long-term contracts to India and Morocco. Even when the Strait fully reopens, not all caged supply will reach the spot market as a meaningful share is already contractually obligated.

Track all sulphur transits via the Strait of Hormuz since 28 February

Source: Kpler cargo flows, May 2026

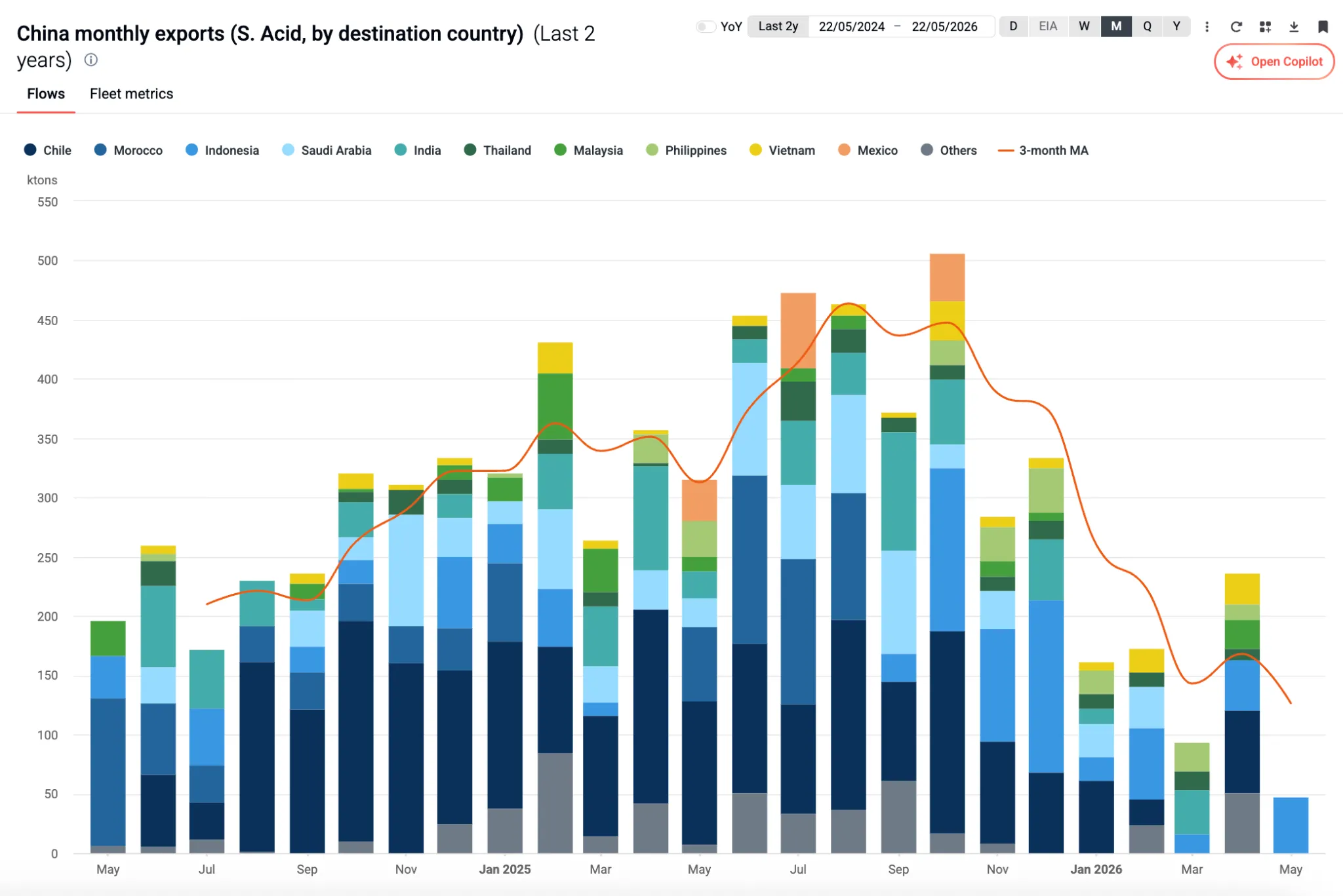

China's export ban removes the backstop

On 10 April 2026, China announced a full export ban on sulphuric acid through August 2026, replacing a 700,000-tonne annual quota with a complete cessation. China is the world's largest acid exporter, with Chile, Indonesia, and Saudi Arabia as its primary markets in 2026.

China sulphuric acid exports by destination (Jan-Apr 26)

Source: Kpler cargo flows, Jan–Apr 2026.

Each destination maps directly onto a critical downstream sector: Chile for copper SX-EW, Indonesia for HPAL nickel, and Saudi Arabia and India for fertiliser and industrial acid. The ban's timing was structurally catastrophic as it removed the secondary backstop supply at precisely the moment the primary MEG source was also constrained.

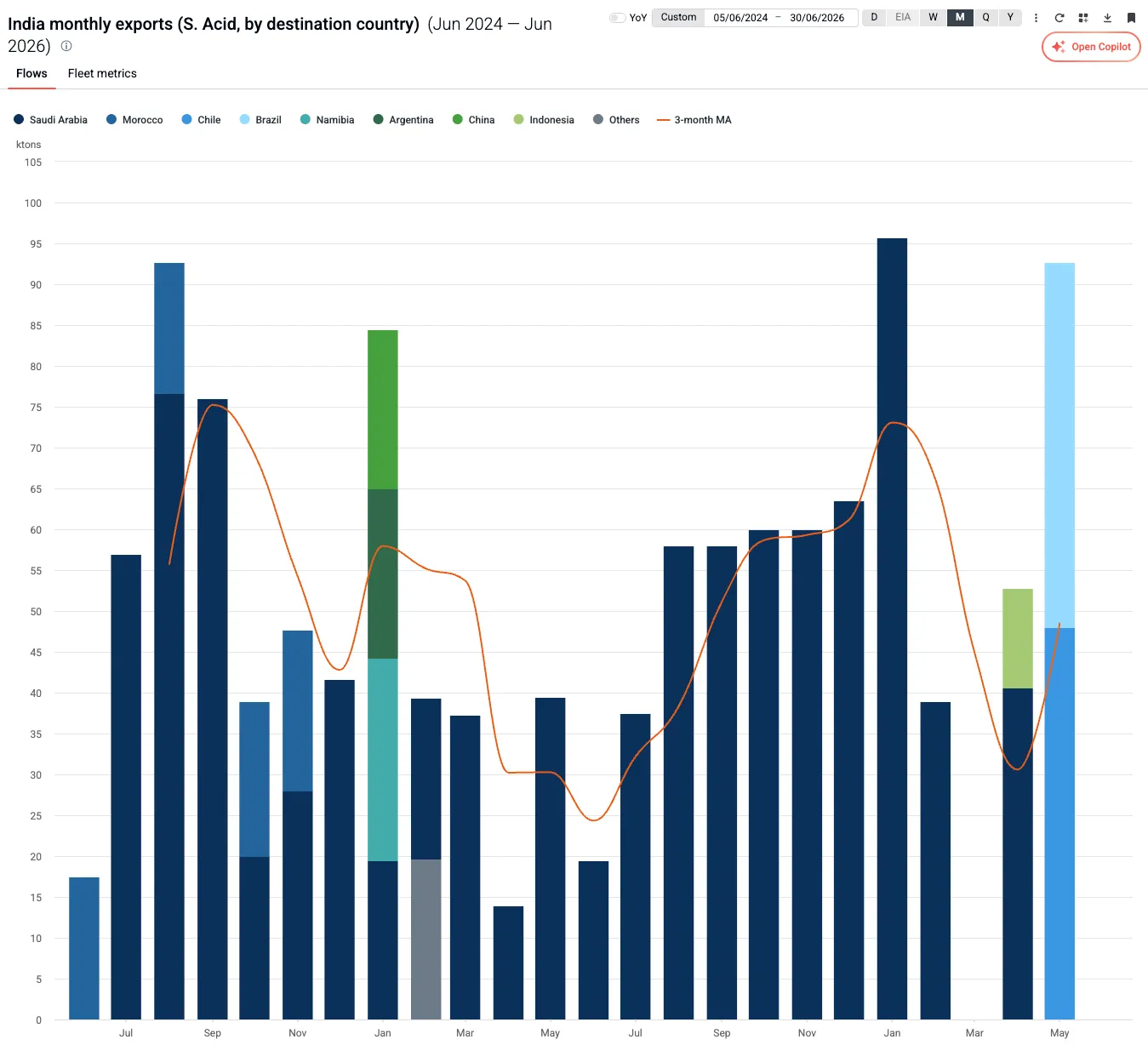

Strait of Hormuz Blockage Forces India to Find New Acid Importers

Saudi Arabia has long been the primary importer of sulphuric acid from India, with Ras al-Khair being the port handling these cargoes. However due to the conflict in the Mideast Gulf, no acid has been able to traverse the Strait of Hormuz. As a result, India has been forced to find new solutions for their sulphuric acid supply.

India sulphuric acid exports by destination country

Source: Kpler cargo flows, Jun 2026

There has been somewhat of a workaround by which Saudi Arabia has some sulphuric acid quantities via the port of Yanbu, albeit more irregularly than before. Regardless, India has also found other trade partners, sending its first shipments to Brazil and Chile in years.

Downstream: Three Industries, One Feedstock

Copper (SX-EW): SX-EW accounts for roughly 15% of global copper cathode production, concentrated in the DRC, Chile, and the US. Acid consumption ranges from 3t per tonne of copper (high-grade ore) to 22t per tonne (ultra-low grade). The critical divide is between integrated producers - notably Codelco, which generates its own acid from smelting byproduct, and non-integrated operators like BHP Escondida and Antofagasta, which must procure from the seaborne market and are fully exposed to the current squeeze.

Nickel (HPAL): HPAL plants have no partial-output mode as they are on or off. Indonesia's HPAL capacity imports approximately 75–80% of its sulphur from the MEG. With that supply cut off, Indonesian buyers are now actively sourcing sulphuric acid imports from Japan and Korea - competing directly with Chilean copper producers for the same smelter acid byproduct. However, replacement volumes remain insufficient to bridge the gap. Huayou has already reduced output at its Indonesian plant by approximately 50%. At current sulphur prices, feedstock represents more than 50% of total MHP production cost, making many operations uneconomic.

Fertilizers: Morocco's OCP received its last MEG sulphur cargo on 10 April 2026 (vessel: Kallone, discharging at Jorf Lasfar) and is now reliant on Russian supply. Mosaic has cut domestic US phosphate output by approximately 2 million tonnes due to elevated costs. North American sulphur tonnes are now flowing to Africa at historic premiums.

New Trade Corridors

The supply dislocation has generated trade routes with no meaningful historical precedent. Kpler has identified four active corridors currently tracked at the vessel level:

Why Supply Cannot Simply Respond to Price

Sulphur is a byproduct, not a primary commodity. No producer increases output because sulphur prices have risen. Recovery rates are a function of the sulphur content of hydrocarbons being processed and refinery throughput as both are driven by energy demand, not sulphur market signals. The extraordinary CFR bids now visible in the market are price-signalling into a structural void. The only resolution is a Strait reopening and gradual inventory drawdown, but even then, the contracted nature of MEG supply means spot market relief will be partial.

Key structural constraint

Sulphur production cannot be ramped up in response to price. The market is experiencing a supply shock with no short-term supply response mechanism - a rare and particularly dislocating dynamic for downstream industries with no alternative feedstock.

Kpler's sulphur and sulphuric acid intelligence spans dry bulk and chemicals - uniquely bridging both sides of the value chain with vessel-level cargo data, updated continuously.

See why the most successful traders and shipping experts use Kpler

Get real-time sulphur and sulphuric acid intelligence