Why a 20 mbd supply shock is no longer moving oil prices

The recent collapse in crude premiums, weaker outright prices, and a correction in refining margins have led many market participants to conclude that the oil market is returning to normal despite the ongoing disruption in the Middle East. This comes although flows through the Strait of Hormuz remain heavily constrained, both crude and product throughput well below pre-crisis levels. However, the severe shortages many feared have not fully materialised. This apparent contradiction is not evidence that the disruption was overstated. Rather, it reflects the remarkable ability of the global oil market to adapt through multiple balancing mechanisms operating simultaneously.

Key Takeaways

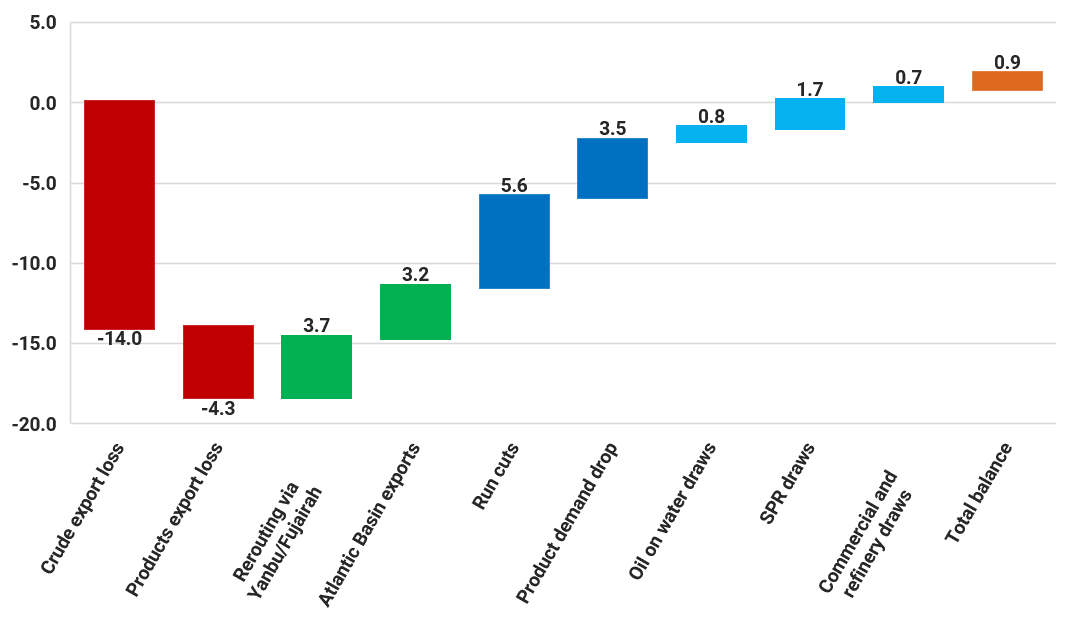

- The global oil market has offset nearly all of the ~20 Mbd of crude and product supply lost following the closure of the Strait of Hormuz through demand destruction, inventory withdrawals, strategic stock releases, rerouted exports, and higher Atlantic Basin exports.

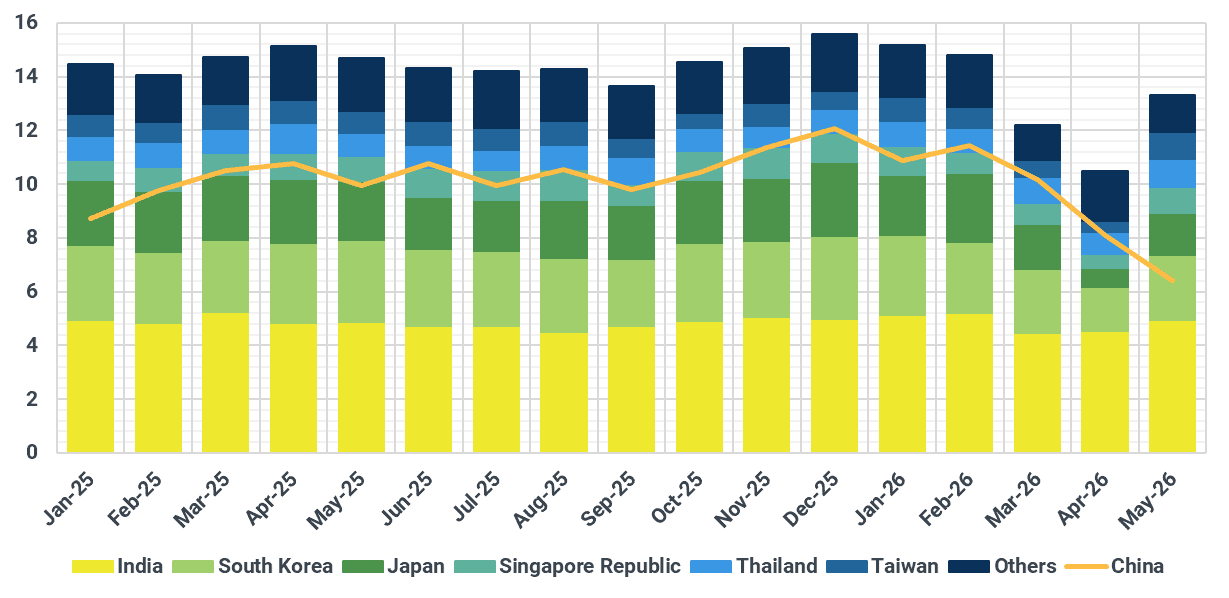

- China has emerged as the market's primary balancing mechanism. Seaborne crude imports fell to a decade low of 6.7 Mbd in May, reducing competition for available barrels across Asia.

- Global refinery runs are estimated to have averaged 5.6 Mbd below pre-war expectations during March-May, removing a substantial source of crude demand and helping ease physical tightness.

- Saudi Arabia and the UAE have maximised alternative export routes, increasing crude shipments from Yanbu and Fujairah by 3.7 Mbd compared with pre-war levels.

- Atlantic Basin oil exports jumped by 3.2 mbd, and flows to Asia have risen by 2.5 Mbd since the disruption, despite Brent-Dubai EFS widening above $11/bbl, demonstrating that security of supply has become more important than arbitrage economics.

- Recent weakness in crude premiums, refining margins, and outright prices reflects successful market adaptation.

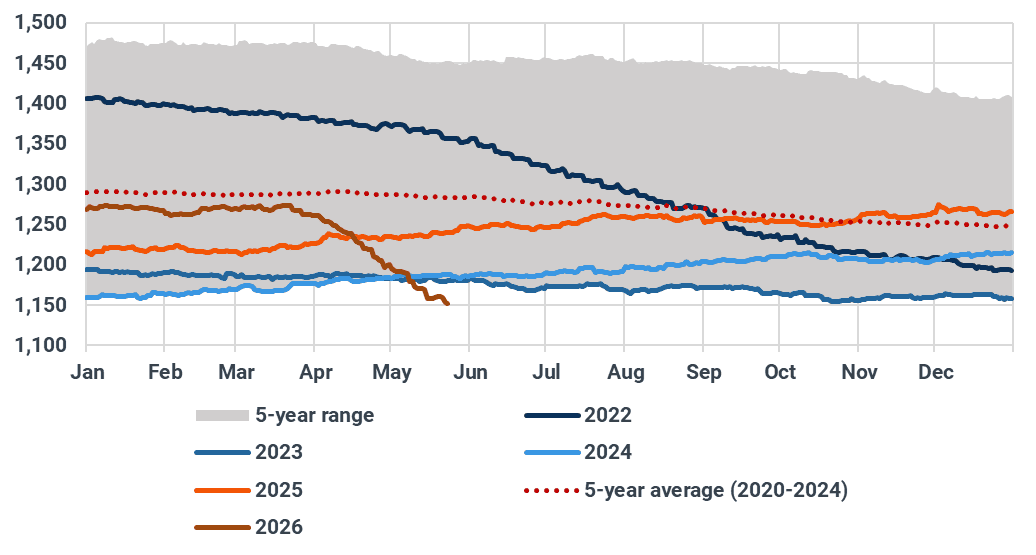

Rebalancing ~20 mbd of lost supply

Source: Kpler

The oil market has now offset all of the largest supply disruption in modern history. The closure of the Strait of Hormuz initially removed close to 20 Mbd of crude and product availability from global markets. Yet nearly three months later, crude differentials have retraced most of their initial gains, refining margins have weakened, and outright prices have moved lower. The explanation is that the market has successfully found alternative barrels, alternative routes, and alternative sources of demand adjustment.

The market has effectively rebalanced a major supply shock through a combination of demand-focused measures and inventory buffers, as well as higher supply from the Atlantic Basin and a maximum re-routing of barrels through alternative routes in the Arabian Peninsula. Demand destruction, particularly in Asia and Europe, has also helped reduce the imbalance.

These adjustments have significantly reduced the effective supply deficit the market faces and helped pressure crude premiums, product cracks, and outright prices lower. The easing in market indicators, therefore, reflects successful adaptation rather than a return to normal operating conditions. Below, we outline the major contributors to the current unusual equilibrium in oil markets:

- lower Chinese imports;

- strategic stock releases;

- refinery run cuts;

- inventory withdrawals;

- oil-on-water reductions;

- increased Atlantic Basin exports;

- re-routing through Yanbu and Fujairah.

China has become the market's primary balancing mechanism

The country's seaborne crude imports (including flows from Made Island) fell to 6.7 Mbd in May, the lowest level in a decade, down 3.5 Mbd year-on-year and 4.4 Mbd below Q1 2026 levels. At the same time, refinery runs declined to around 13.1 Mbd, lower by 1.8 Mbd y/y.

The combination of lower imports and weaker refinery activity has released barrels into the broader Asian market, easing regional competition for Atlantic Basin, Russian and Middle Eastern cargoes at a time when supply chains remain under stress.

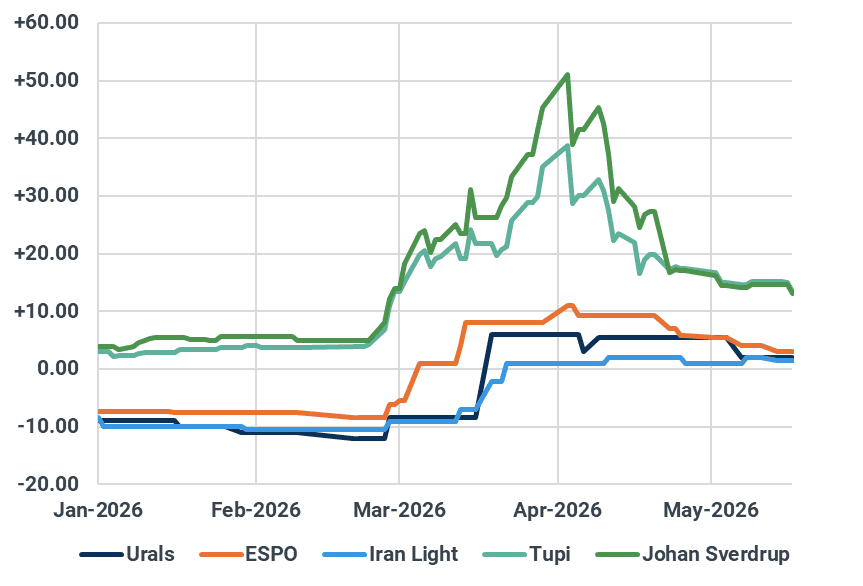

The impact has been felt across the region. Reduced Chinese buying has improved crude availability to refiners in Japan, South Korea, India and Southeast Asia, helping ease the apparent physical tightness despite ongoing disruptions to Middle Eastern flows. This has helped reduce the steepness in Dubai backwardation and crude differentials on a delivered basis into Eastern Asia. Aramco has had to cut its OSPs into Asia by $4/bbl for Arab Light as a result.

Selected grades differentials against ICE Brent, DES Shandong, $/bbl

Source: Argus Media

However, the durability of China's adjustment remains uncertain. Evidence of increasing inventory draws suggests that part of the decline in imports is being offset by stock withdrawals, raising questions about how long China can continue to act as the market's primary shock absorber.

Asia oil imports, Mbd

Source: Kpler

This new trend of lower Chinese buying could continue over the summer as refiners' inventories are still elevated, reducing the need to draw from SPR. Our estimate shows China’s SPR have built since the beginning of the war by 8 mbbls. On the other side, inventories stored at refinery installations have drawn by 15 mbbls in May.

With refinery inventory currently just above 300 mbbls, the shortfall in imports can be compensated by drawing from refiners' storage tanks for 60-75 days, indicating that China’s oil imports are likely to remain low until August.

China oil inventories by tank type, mbbls

Source: Kpler

Refinery run cuts in Asia have become a critical part of the puzzle

Another somewhat underappreciated component of the adjustment has been lower refinery activity. Chinese refinery runs have fallen sharply, while refinery throughput across Asia remains materially below both last year's levels and historical averages. Run reductions due to logistical constraints and feedstock availability continue to influence operating decisions.

Indeed, refinery run cuts have removed approximately 2.7 Mbd of crude demand from Asia since March. Run reductions have been even more pronounced in the Middle East, averaging around 3.0 Mbd, driven by product export bottlenecks and operational disruptions at several facilities, including Sitra, Mina Al Ahmadi and SATORP. Russia has also experienced refinery run cuts of roughly 375 kbd following a series of drone attacks on refining infrastructure. These reductions have been partially offset by higher refinery utilisation elsewhere. Refiners in the United States, Latin America (Brazil, Argentina), and Nigeria's Dangote refinery have increased crude processing in response to stronger margins and shifting trade flows. Nevertheless, the increase in runs outside the affected regions has only partly compensated for the losses. On a net basis, global refinery runs are estimated to be around 5.6 Mbd below pre-war expectations on average during March-May.

As a result, part of the current balance has been achieved through weaker crude demand rather than improved supply availability. This distinction is important. The decline in crude premiums and refining margins does not necessarily signal stronger supply conditions; it also reflects the fact that refiners are processing materially less crude than they would under normal market conditions.

Asian refinery runs, kbd

Source: Kpler

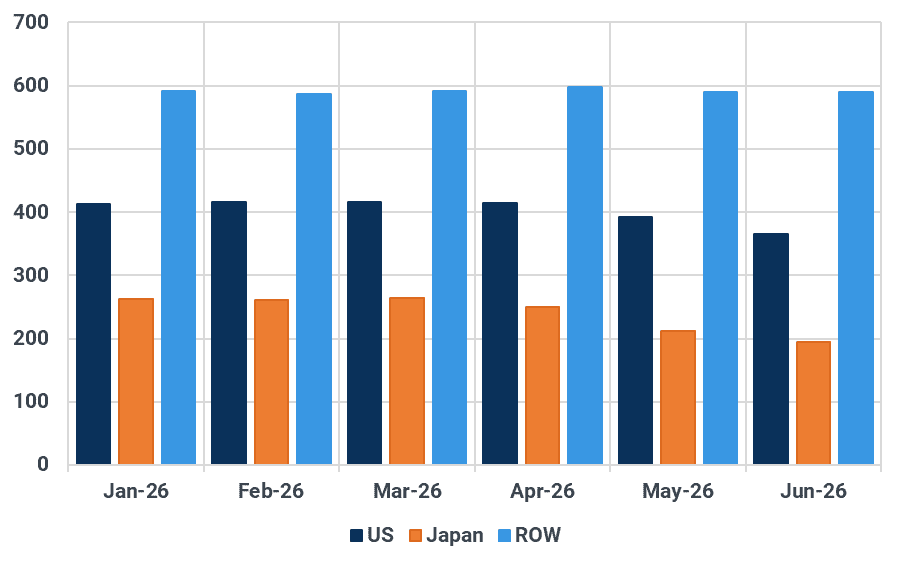

West of Suez oil shipments jump by 3.2 Mbd; flows to Asia jump by 2.5 Mbd

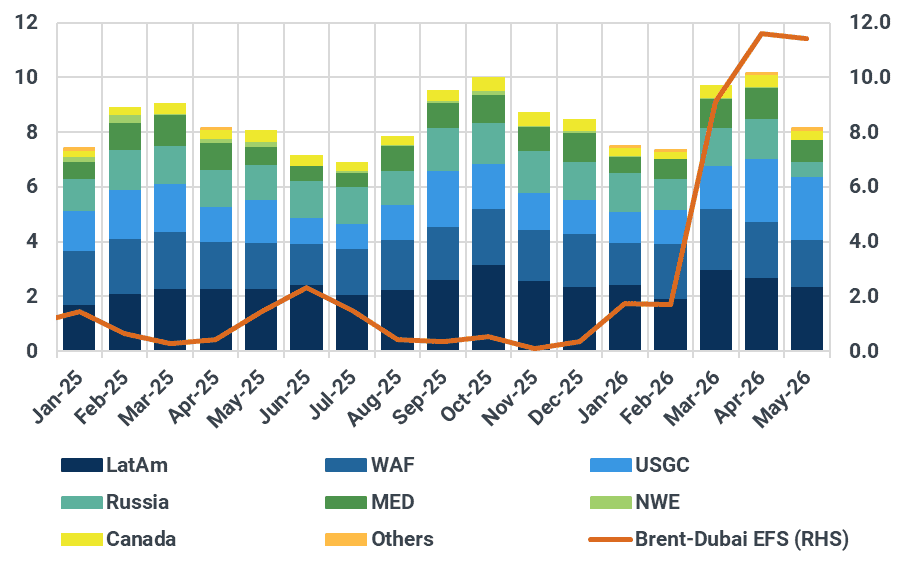

The market's response has not been limited to demand adjustments. Increased crude exports from the US, Brazil, Guyana, Libya, West Africa, Russia and Kazakhstan have helped offset part of the loss in Middle Eastern flows. West of Suez oil exports have jumped by 3.2 Mbd since the war, compared to Jan-Feb, with flows to the East of Suez counting for 2.5 Mbd of the increase. WoS flows to Asia reached a new record of 10.1 Mbd reached in April.

Russian crude exports remain elevated amid sustained drone strikes. Lower domestic refinery runs have pushed more barrels to export markets. Russian shipments increased by nearly 400 kbd to 3.7 Mbd since March, the highest level in two years.

Flows to the EoS are likely to remain as elevated in May; our estimate of 8.9 Mbd at the time of writing will be revised upward as we receive more information about cargo destinations.

This jump comes despite an unworking arbitrage, with the Brent-Dubai EFS spread jumping from ~1.70/bbl to more than $11/bbl on average since the beginning of the war, highlighting that security of supply matters more than arbitrage flows.

Atlantic Basin oil flows to Asia (Mbd, LHS) and Brent-Dubai EFS spread ($/bbl, RHS)

Source: Kpler. Our May 2026 estimates are likely to be revised upwards in the coming days

However, the replacement barrels entering the market are predominantly light-sweet grades, creating a different quality balance than existed before the disruption. This shift helps explain why premiums for grades such as Es Sider, CPC Blend, WTI Midland, and several West African streams have weakened so significantly in recent weeks. The market is increasingly long light barrels while remaining comparatively tighter in medium and heavy crude grades.

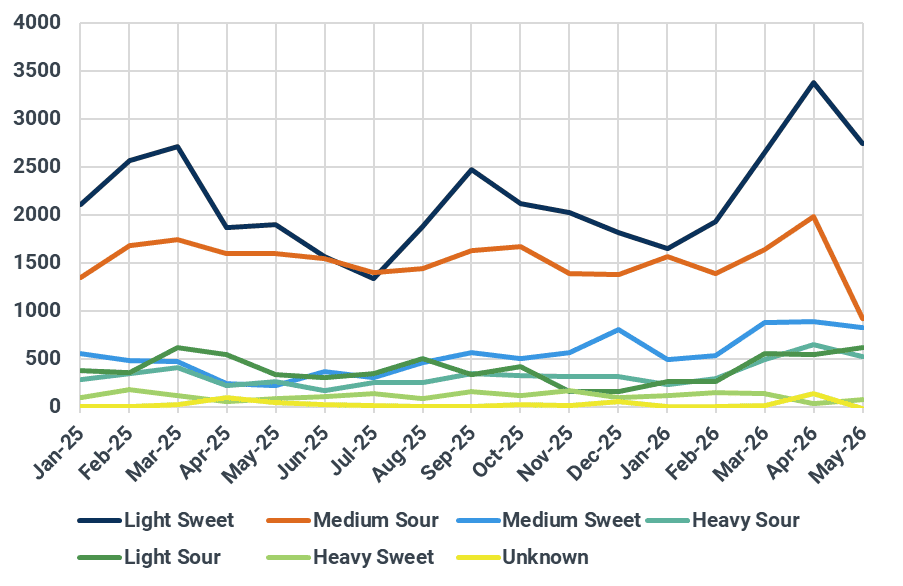

The softness in these differentials should therefore not be interpreted as evidence of a broadly oversupplied crude market. Instead, it reflects changing refinery economics, shifting crude slate preferences, and the growing availability of light-sweet barrels at a time when refinery runs have been reduced across Asia. The challenge is increasingly one of crude quality and placement rather than absolute crude availability.

Atlantic Basin oil flows to Asia (excluding China) by crude quality, kbd

Source: Kpler. Our May 2026 estimates are likely to be revised upwards in the coming days

Saudi Arabia and the UAE re-route 3.7 Mbd of crude via Yanbu and Fujairah

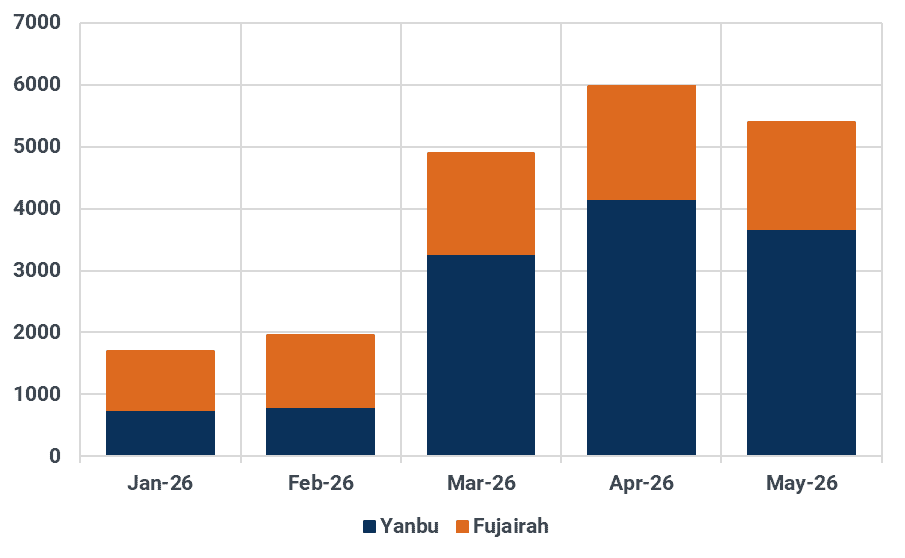

The closure of the Strait of Hormuz has pushed Aramco and Adnoc towards a full utilisation of their alternative pipelines. It took around 4 weeks to maximise pipeline throughput in Saudi Arabia as the East-West pipeline was only used at a rate of around 35% before the war. We now believe throughput is maximised, resulting in a combined crude export growth of 3.7 Mbd from Yanbu and Fujairah.

Crude exports from Yanbu and Fujairah, kbd

Source: Kpler

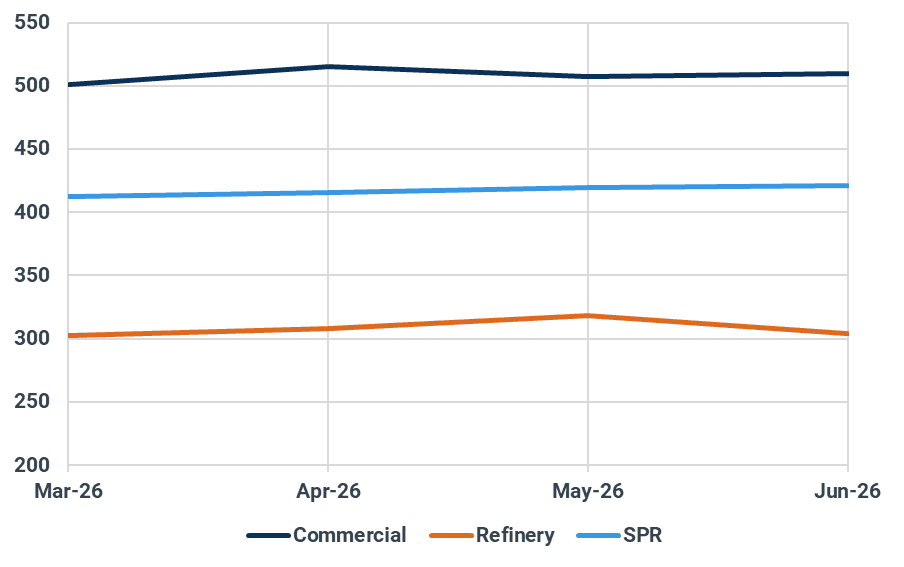

Strategic stocks, inventories and oil-on-water have bought the market time

A key component of the market's adjustment has been the drawdown of strategic and commercial inventories. The US has released approximately 870 kbd from its Strategic Petroleum Reserve (SPR) since March, while Japan, South Korea and other IEA members have also contributed emergency barrels to the market. These releases have helped alleviate prompt tightness and provide refiners with additional feedstock during a period of severe logistical disruption.

It took the OECD about two weeks to start taking decisions around the release of strategic reserves. This is why SPR levels started to drop significantly from 20 March onwards. Since that date, they have been drawing by 124 mbbls, or 1.77 Mbd.

Global oil in SPR, mbbls

Source: Kpler

By far, the US and Japan have been drawing the most from their SPR. Since March, these draws have reached 50 mbbls for the US and 69 mbbls for Japan, while SPR in the rest of the world only drew by 1.2 mbbls.

Global oil in SPR, mbbls

Source: Kpler

Beyond strategic stocks, commercial inventories and oil-on-water have acted as critical buffers. Since 20th March, inventory holdings at commercial tanks and refineries have decreased at a rate of 777 kbd, or a total of 53.4 mbbls. Crude volumes in transit have declined by roughly 790 kbd since early March, effectively supplying the market with barrels that would otherwise have remained in storage or within the global logistics system. Cargoes already on the water have been particularly important, helping bridge supply gaps while Atlantic Basin barrels were redirected toward Asia and alternative trade routes developed.

Global oil inventories in commercial tanks or refineries, mbbls

Source: Kpler

However, these mechanisms should not be mistaken for new supply. Strategic releases, inventory withdrawals and reductions in oil-on-water all represent future availability being brought forward into the present. While they have successfully cushioned the immediate impact of disrupted Middle Eastern flows, their ability to support the market is inherently limited.

As inventories approach minimum operating levels - the volume required to maintain normal operations across storage, pipeline and refinery systems - the market becomes increasingly reliant on demand restraint and supply normalisation to maintain balance.

Adaptation doesn't mean normalisation

The market has replaced almost 20 Mbd of lost supply. Prices, differentials, and refining margins are reflecting that reality.

Our analysis suggests that lower Chinese imports, refinery run cuts across Asia and the Middle East, strategic stock releases, commercial inventory withdrawals, reduced oil-on-water, increased Atlantic Basin exports, and maximum utilisation of Saudi and UAE bypass infrastructure have collectively offset the almost entire loss of Persian Gulf supply.

The market has effectively exchanged one form of balance for another. Before the disruption, global balances relied on uninterrupted flows through the Strait of Hormuz. Today, balances depend on demand restraint, inventory depletion, emergency stock releases, and the redirection of long-haul crude flows from the Atlantic Basin to Asia. The result is a market that appears adequately supplied on the surface, but one that is operating with significantly less flexibility than before.

This distinction matters. Recent weakness in crude premiums should not be interpreted as evidence of abundant supply. Rather, it reflects a market where refinery demand has been curtailed, inventories have been mobilised, and every available logistical workaround has been pushed close to its operational limit.

Our current accounting suggests the global market is now broadly balanced and may even be running a modest surplus. However, this apparent surplus is being created by mechanisms that are largely finite. Strategic stocks cannot be released indefinitely. Commercial inventories cannot be drawn without limit. Oil-on-water cannot continue to decline forever. Likewise, Chinese imports are unlikely to remain near decade lows once refinery inventories normalise.

The next phase of the adjustment will therefore be determined by how quickly disrupted Middle Eastern supply returns relative to the pace at which inventories continue to decline. Until then, the market remains dependent on temporary balancing mechanisms rather than a restoration of normal trade flows.

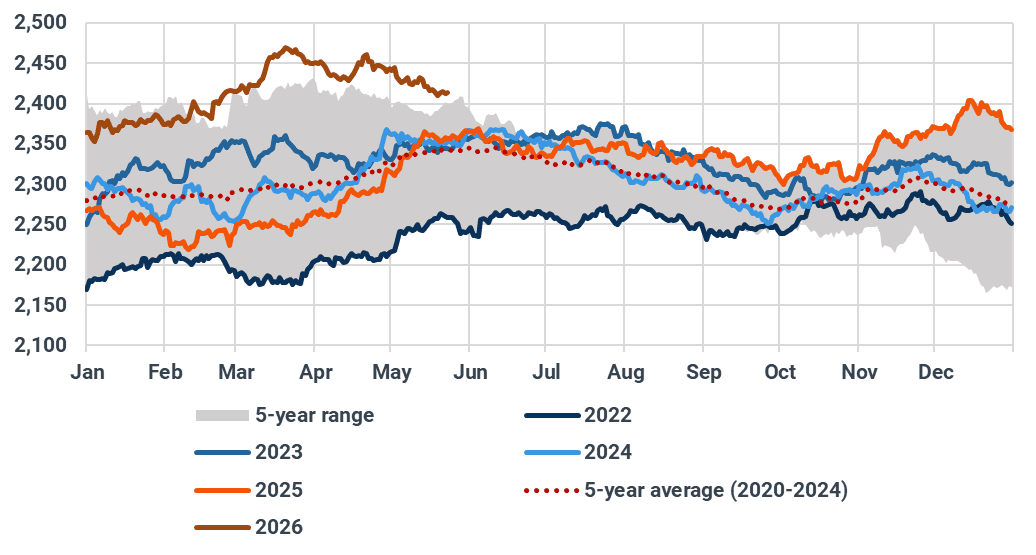

Rebalancing ~20 mbd of lost supply

Source: Kpler

See why the most successful traders and shipping experts use Kpler