WTI flirts with physical squeeze as Cushing buffers evaporate

Inventory draws have been in keen focus since the start of the US-Iran war. The US has pivoted to a net liquids exporter in this time, but the realities of sharp draws are pushing prompt structure higher and putting further pressure on critical inventories and domestic consumers.

Key Takeaways

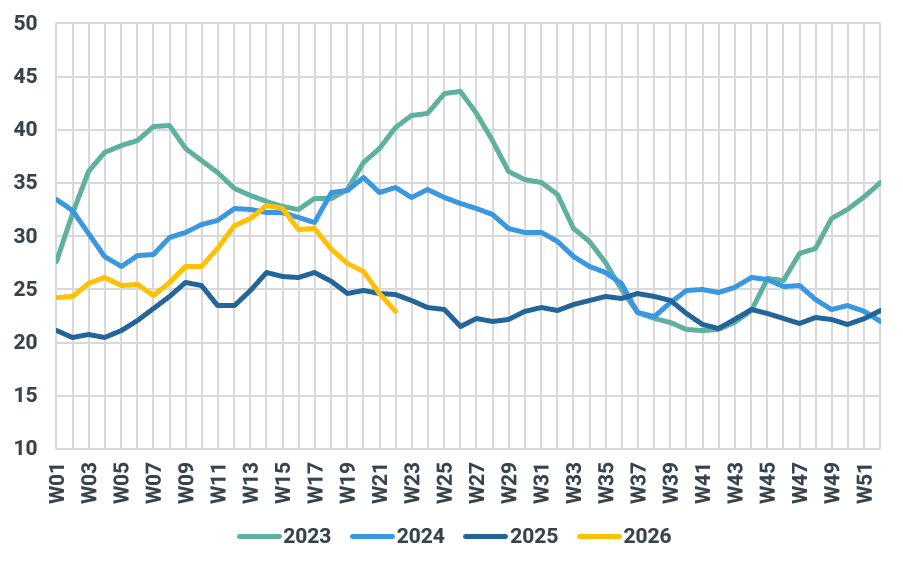

- Cushing inventories are critically low at around 22 mb, following another weekly draw of 583 kb.

- The WTI futures curve reflects extreme backwardation due to the US-Iran war, with WTI M1-M3 structure jumping by over $2/bbl in the last five sessions.

- Hard physical limits on US exports near 5.5 Mbd for crude on a sustainable basis, representing only a marginal replacement for the disrupted Middle Eastern volumes.

- Escalating Canadian wildfire risks threaten up to 500 kbd of heavy oil sands production, exposing PADD 2 refiners to immediate supply shocks.

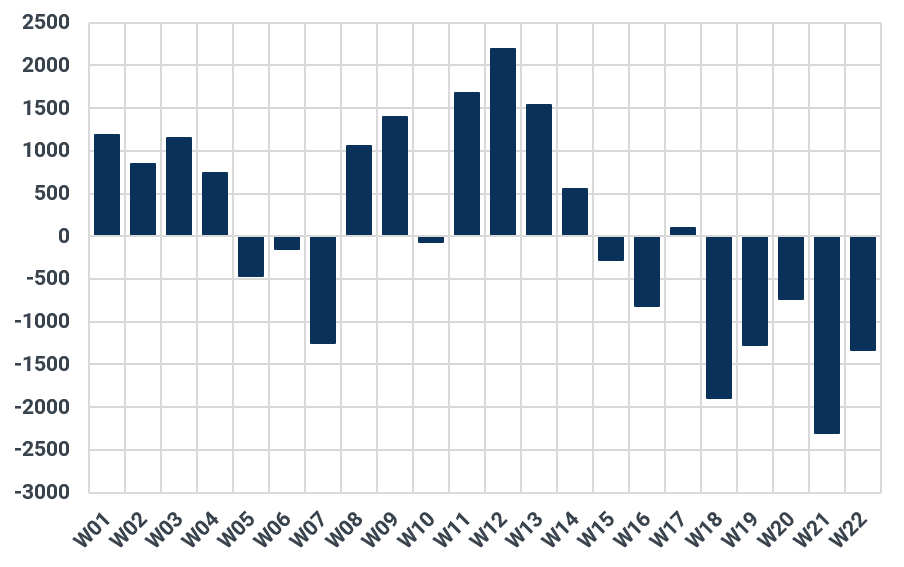

The latest weekly data showed a total crude draw (including SPR pull) of 16 Mbbls, with Cushing down to under 22 Mbbls. The total petroleum stocks in the US now sit at multi-decade lows, and as such WTI flat prices rapidly rose by nearly 2% off the back of the weekly statistics.

As such, the structural thinning of Cushing buffers is no longer a tail risk, it is the base case, and the implications ripple across the entire WTI complex. Low Cushing inventories directly underpin the steep WTI term structure, with structure on M1-M3 futures moving back up towards $7/bbl, for the first time in around 10 sessions.

Cushing oil inventories by year, Mbbls

Source: Kpler, EIA

Concurrently, MEH differential spread is narrowing from compressed levels, suggesting that the pull to keep prompt barrels at home rather than for the export market is intensifying. The differential between MEH and Cushing sits just above $1/bbl, while it was trading around $4/bbl one month ago.

US crude exports could come off for pricing reasons but also face a hard physical ceiling. Exports hit a record 5.6 Mbd sustainably last month, as the US sought to incrementally capture higher prices and help balance the market. But pipeline and dock constraints cap total US exports to this level, assuming an entire supply chain that works at full capacity with no hiccups. Only two terminals—Enbridge's Ingleside Energy Center and Gibson Energy's South Texas Gateway—can directly load VLCCs, meaning the US cannot replace Middle Eastern volumes at scale.

Meanwhile, the SPR draw remains a finite fix. The temporary oil exchange program has released over 170 mb from the SPR for delivery through August 2026. However, with the SPR depleted to 415 mb entering the crisis, these barrels are insufficient to offset the Hormuz closure long term. The required repayment at an 18-24% premium in kind will severely strain medium-term inventories between 2027 and 2029.

To stem the issue, US crude imports are also jumping, with some 6.4 Mbd imported last week, up by over 1 Mbd on the week. US refiners are further squeezing commercial stocks by running at a 95% utilization rate after a remarkably light maintenance season. This elevated demand faces an immediate risk from Canadian wildfires, with active blazes burning within 20 kilometers of 500 kbd of oil sands sites. A disruption of 300-500 kbd would heavily stress PADD 2 refiners and push the situation at Cushing to critical levels.

The strain on the consumer is starting to show, with implied gasoline demand down by 660 kbd on the week, even approaching peak summer demand.

Weekly Cushing inventory changes, kb

Source: Kpler, EIA

Market insights you can trust

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler