Can Venezuela hit its ambitious 1.4 Mbd target by year-end?

Despite a remarkable 400 kbd increase in output since Q4 2025, Venezuela’s push to add another 200 kbd to reach its 1.4 Mbd year-end target is likely to face operational bottlenecks that could slow this rapid growth trajectory.

Key takeaways

- Venezuela aims to reach 1.4 Mbd by late 2026, ~200 kbd above current levels and 100 kbd above our year-end target.

- Near-term upside to be capped by logistical hurdles, while long-term growth will be influenced more strongly by global balances and crude prices.

- Venezuela has remained one of the world's fastest-growing oil producer this year, with output rising by ~400 kbd since Q4 2025.

- Oil reforms and new regulations that have reduced the government’s take on crude ventures to a combined 20–35% are incentivizing more investments.

- Output projected to plateau ~2 Mbd by the end of the decade.

Venezuela aims to elevate its crude production to approximately 1.4 Mbd by year-end, representing a 200 kbd increase from current volumes. Although production should continue its upward trajectory through the rest of the year, this goal surpasses our 1.3 Mbd forecast and appears slightly optimistic given the immediate operational bottlenecks.

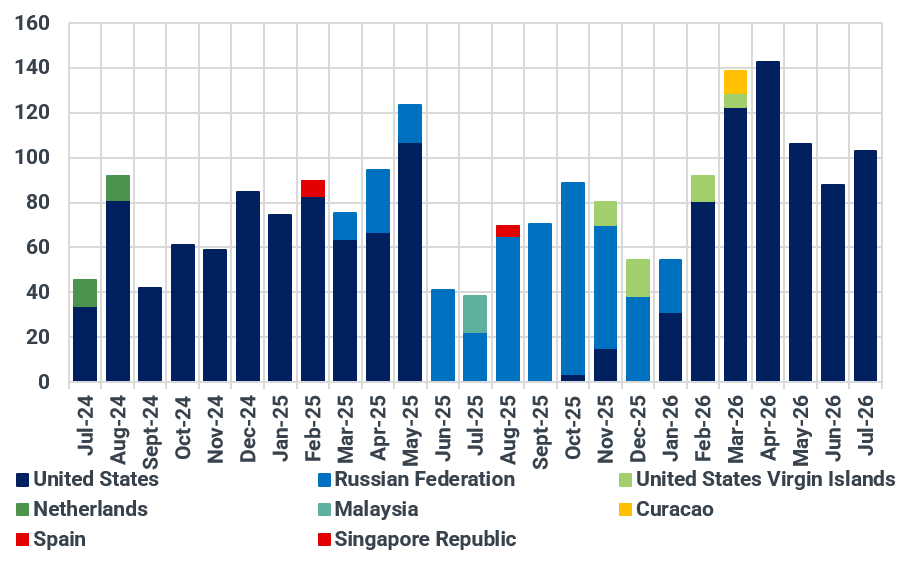

Nevertheless, recent progress is undeniable. Production climbed to about 1.2 Mbd in June—up from roughly 850 kbd in the final quarter of 2025—establishing Venezuela as the world's fastest-growing oil producer this year. This ramp up has been accompanied by higher imports of diluent, with Venezuelan naphtha imports averaging around 100 kbd more recently (see chart below).

Venezuelan naphtha imports by origin, kbd

Source: Kpler

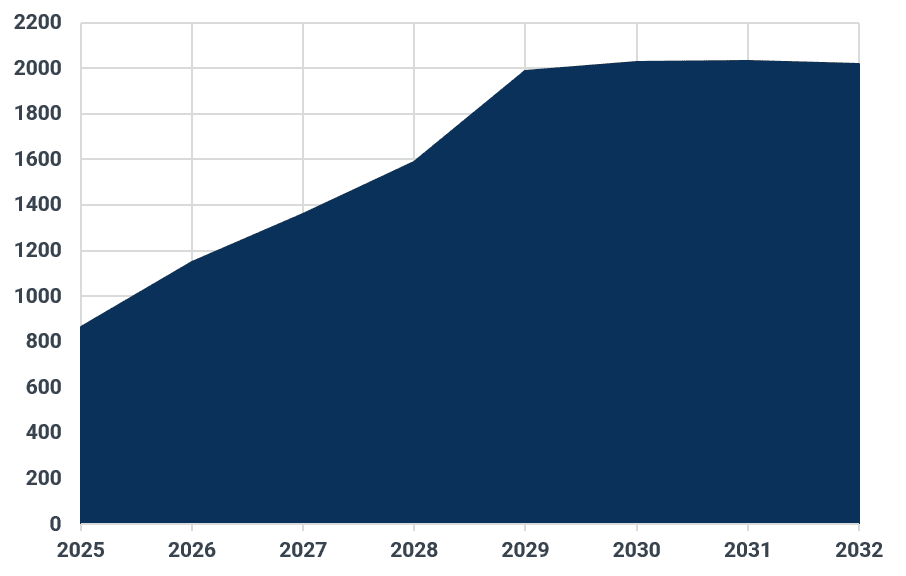

While the government target stands at 3 Mbd by 2030, we project output will reach a more realistic 2 Mbd by the end of the decade, assuming sustained political stability and expanded participation from major international oil companies.

The discrepancies between our estimates and those by Venezuela are related primarily to rig deficits, and decayed infrastructure, which will limit the upside in the near-term. Notably, further upside thereafter (after 2030) will largely depend on global balances and crude prices, with balances expected to remain relatively lengthy in the long-term, capping the upside potential for Venezuela beyond 2030 and keeping output around 2 Mbd in 2031 and 2032 (see chart below).

Long-term Venezuelan supply outlook, kbd

Source: Kpler

A restructured investment landscape is driving renewed foreign interest. Interim President Delcy Rodríguez recently enacted sweeping oil reforms that simplify the fiscal regime. The new regulations slash the government’s overall take on crude ventures to a combined 20–35% for most projects, down from the historical average of nearly 83%, and establish transparent royalty brackets. Stronger global oil prices stemming from the US-Iran conflict have further sweetened the proposition for returning operators.

Existing operators, led by Chevron, have capitalized on these changes most rapidly. Others, such as ExxonMobil and ConocoPhillips, are progressing more cautiously, currently transitioning initial agreements with PDVSA into formal, binding joint ventures. However, persistent hurdles—namely rig deficits, and decayed infrastructure—will continue to bottleneck operations well into 2027. Consequently, we do not anticipate a significant acceleration in output until 2028.

Most notably, Exxon's strategic direction has shifted. By late May, the major was actively negotiating production rights on up to six oil fields across several regions, marking a striking turnaround nearly two decades after its exit from the country. This policy reversal aligns with President Trump's demand for a $100 billion private sector investment package to reconstruct Venezuela's energy infrastructure following Maduro's departure in January. This pivot occurs despite Exxon CEO Darren Woods labeling the country 'uninvestable' just months prior due to a lack of legal guarantees—a stance that reportedly triggered immediate public pushback from the White House.

See why the most successful traders and shipping experts use Kpler