China’s continued LNG inventory drawdowns in April shift spot LNG demand upside to early Q3

China’s LNG inventories continued to decline through April as end users relied on storage to offset short-term supply disruptions amid weak spot import economics. With ex-terminal prices below Asian spot LNG costs, terminals have remained disincentivized to procure spot cargoes, instead monetizing inventories to meet demand. This dynamic is delaying rather than eliminating LNG demand, pushing restocking into early Q3. As inventories fall below seasonal norms ahead of peak summer, China’s supply buffer is tightening, particularly in southern regions where hydropower risks and stronger cooling demand are emerging. We expect a step-up in spot LNG procurement from June–July, creating a bullish skew to Asian LNG prices in early Q3, with upside risks amplified if supply disruptions persist.

Market & Trading Calls

- China LNG Demand: Slight increase, as 2026 demand revised up by 0.2 mt to 63.2 mt, reflecting stronger restocking demand in Q3–Q4. The revision primarily captures a timing shift in demand rather than stronger underlying consumption.

- China implied LNG Inventory: Lower, as inventories continue to decline as storage is used to offset supply disruptions and weak spot arbitrage delays procurement. Effective inventory tightness increases as buffers fall below seasonal norms ahead of summer.

- Asian Spot LNG Prices: Slightly bullish in early Q3, as restocking demand from China is expected to resume from June–July as inventories tighten and cooling demand rises. Price upside is concentrated in early Q3, particularly if supply disruptions persist.

China’s implied LNG inventories declined by 0.6 mt m/m to 6.4 mt (43% full) at end-April, broadly in line with expectations. The drawdown reflects continued reliance on storage to manage short-term supply disruptions, while weak import economics have discouraged spot procurement. With ex-terminal prices below Asian spot LNG costs, terminals have remained incentivized to monetize existing inventories rather than purchase additional cargoes.

Looking ahead, high Asian spot LNG prices and lagged oil-linked term pricing are expected to keep Chinese ex-terminal prices elevated at around $15/MMBtu on average through Q2 and early Q3. Despite firm domestic prices, spot import margins remain compressed, limiting near-term buying interest. As a result, inventories are projected to decline further to around 6.2 mt by end-May and remain broadly flat in absolute terms through end-June.

However, this flat trajectory masks increasing tightness. The decline in inventory percentage (to ~40% by end-June) is partly driven by terminal capacity expansions, including PipeChina Longkou, rather than outright stock depletion. More importantly, inventory levels are falling below seasonal norms ahead of peak summer, reducing the system’s effective buffer. In this context, usable inventory cover—not absolute volumes—becomes the binding constraint.

As inventories tighten, we expect Chinese LNG buyers to re-enter the spot market from June–July. The trigger for renewed procurement will likely be a combination of lower inventory cover, narrowing spot import losses, and rising cooling demand. Southern China is expected to lead this shift, supported by relatively low stock levels, stronger temperature-driven demand, and weaker hydropower generation early in the summer.

This delayed procurement cycle is expected to tighten Asian LNG balances in early Q3. While the base case reflects inventory-driven restocking, the market impact could be more pronounced if supply disruptions extend into the June–July period, reinforcing upward pressure on prices.

On infrastructure, some terminal expansions, including PipeChina Longkou and Damaiyu LNG, have been delayed into Q2–Q3. This pushes part of the anticipated restocking demand into the second half of the year, contributing to the upward revision in 2026 LNG demand. Overall, the current softness in Chinese LNG imports reflects a temporal shift in demand into Q3–Q4, rather than structural weakness.

China implied total LNG inventory vs terminal capacity (LHS: % of nominal capacity; RHS: mt)

Source: Kpler Insight

China implied LNG inventory forecast (%)

Source: Kpler Insight

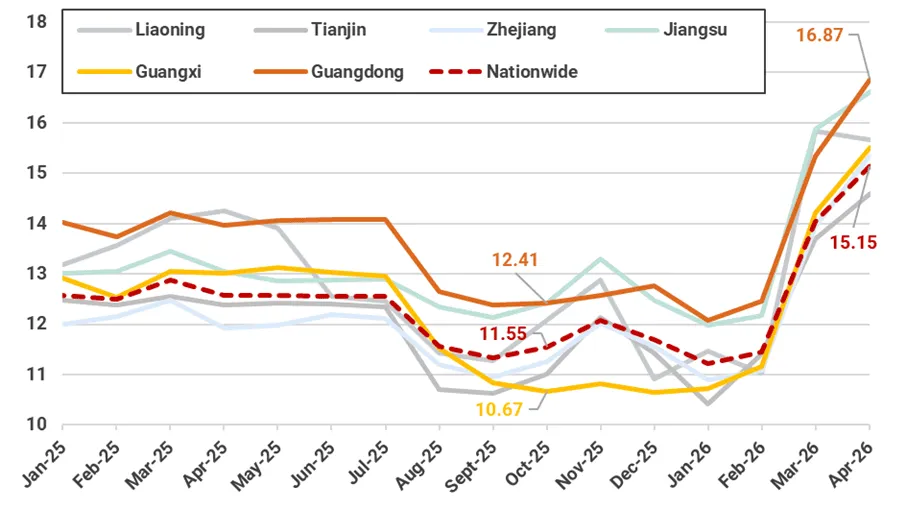

Monthly average ex-terminal LNG prices by province in China ($/MMBtu)

Source: SHPGX, CQPGX, Kpler Insight

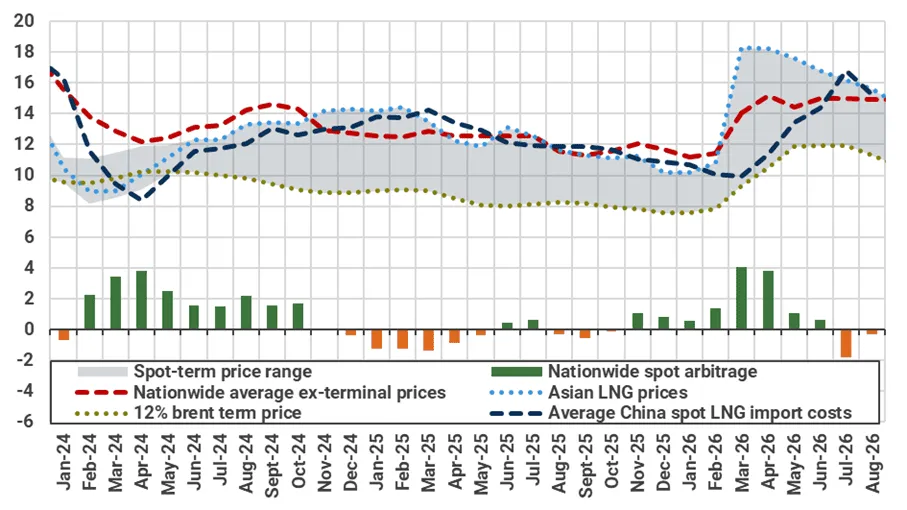

Monthly average ex-terminal prices vs spot LNG import costs in China ($/MMBtu)

Source: SHPGX, CQPGX, Kpler Insight. Note: 1) Average China spot LNG import costs are represented by China’s landed spot LNG prices (CLD) reported by SHPGX. 2) North, East, South represents average ex-terminal prices across the terminals in respective regions. 3) Nationwide spot arbitrage: ex-terminal prices subtracted by Average China spot import costs. 4) Kpler Insight estimation starts from May onwards.

See why the most successful traders and shipping experts use Kpler