Cracks hold firm as product markets tighten ahead of summer

Refined products remain broadly supported by low inventories, constrained Middle Eastern flows, and resilient demand, tightening balances globally, while uncertainty over Hormuz transits persists.

Market & Trading Calls

Naphtha:

- Slightly bullish West of Suez naphtha cracks, supported by positive cracking margins and stronger blending demand into May, while the East continues to draw marginal barrels from the Med and US.

- Slightly bullish East of Suez naphtha cracks as the market rebalances on recovering petchem runs, but ongoing regional tightness is unlikely to ease meaningfully without Middle Eastern barrels.

Gasoline:

- Bullish West of Suez cracks, as low US stocks and depressed yields set the stage for a market squeeze as the summer driving season approaches and middle distillates continue to reign supreme in refinery economics; although rising retail prices should not be ignored.

- Slightly bearish East of Suez cracks, amid prospects of rising Chinese exports and lower Indonesian buying, although the market remains tight and uncertainty around Strait of Hormuz transits lingers.

Middle Distillates:

- Slightly bearish Asian gasoil as the downwards trend is likely to continue with better supply, particularly now from Northeast Asia and China, pressures the prompt.

- Slightly bearish Asian jet as greater jet supply sees further normalization of values, although arbitrages, with the exception of PADD 5, would seem unlikely at this point given the volatile and risky nature of markets.

- Neutral to bearish European distillates as prompt selling and lower flat prices erode the backwardation structure and premiums. However, this does not solve the structural deficits in place and the outlook remains neutral in the very short term and stronger further out.

Residue:

- Slightly bullish West of Suez HSFO cracks: Low HSFO/HSSR inflows, strong USGC coking margins, and ARA fuel oil stocks at multi-year lows should keep regional supply tight.

- Slightly bullish West of Suez VLSFO cracks: Strong VGO demand, limited inflows, and deepening ARA backwardation should keep VLSFO cracks firm.

- Slightly bullish East of Suez HSFO cracks: Deep backwardation, falling Singapore stocks, and rising summer utility demand should support cracks despite recent Russian inflows.

- Slightly bullish East of Suez VLSFO cracks: Lower inflows, a narrower East-West spread, and reduced blendstock availability should support cracks after the recent correction.

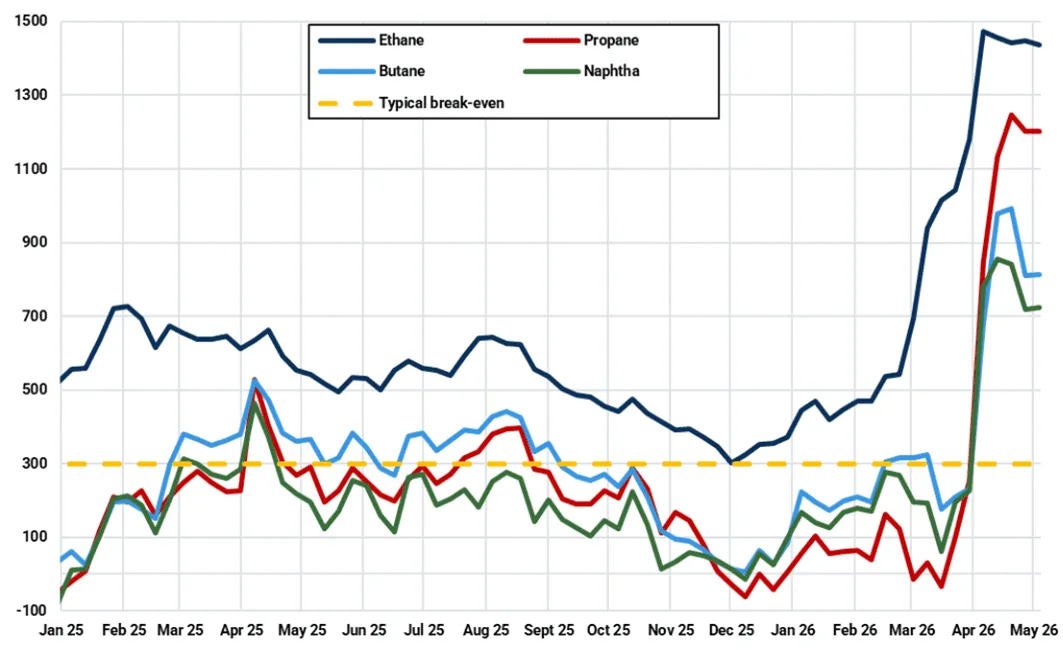

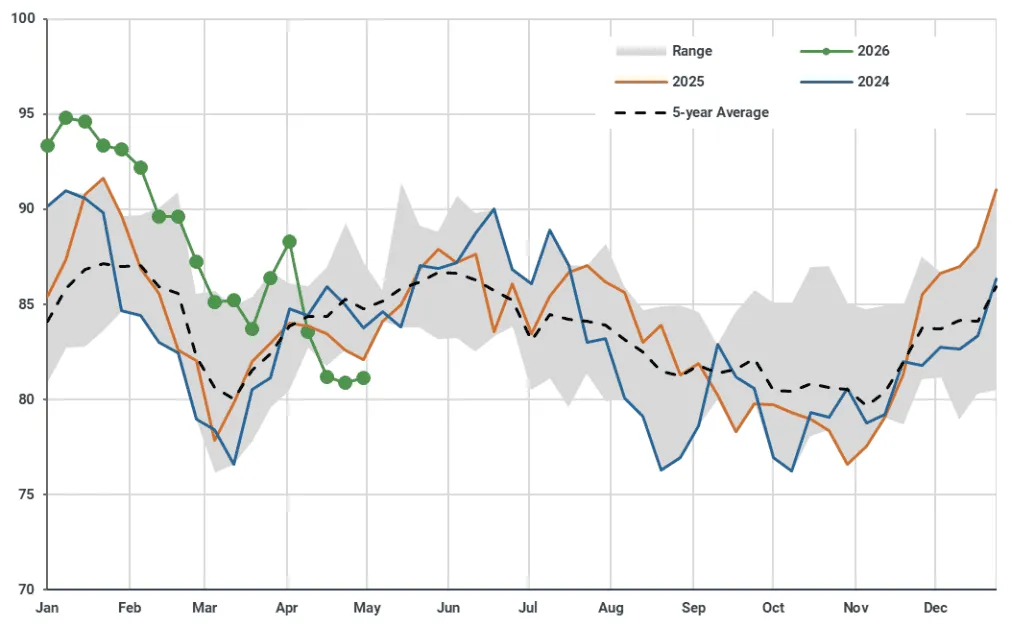

Naphtha: Cracks to find a new lower equilibrium this week, although fundamentals will remain tight through May

Light naphtha cracks ($/bbl)

Source: Kpler calculations using Argus Media prices

The earlier decline in naphtha cracks seen around two weeks ago appears to have found a new lower equilibrium, while ongoing crude price volatility continues to add uncertainty to the near-term price outlook. Fundamentally, the naphtha market is unlikely to see a meaningful improvement amid renewed Middle East tensions, and we expect tightness to persist through May as inventories continue to draw.

West of Suez

Northwest European (NWE) naphtha cracks found a floor after weakening over the past two weeks. While cracker margins have slightly eased from recent highs, operators remain incentivised to raise runs. That said, propane is still preferred where possible. The propane-naphtha spread fell beyond -$300/t as of 5 May, strongly incentivising switching, particularly amid rising C3 outflows from US Neches River 2 terminal.

NWE blending requirements are also set to seasonally rise, with the Eurobob/naphtha spread widening w/w. We expect naphtha cracks to strengthen in the coming weeks as supply remains constrained. Strong Asian demand is likely to pull additional US and Med swing barrels Eastward, while ARA inventories remain below average.

Northwest European gross complex steam cracking margins per ton of ethylene ($/t)

Source: Kpler calculations using Argus Media prices

As mentioned last week, the E/W spread is unlikely to revisit March highs given the renewed strength in NWE fundamentals as crackers also return from maintenance. Indeed, Rotterdam will import a US cargo for mid-May delivery – the first since the start of the Middle East conflict as buyers in the NWE begin more meaningfully competing with Asia for marginal US and Med barrels.

In the US, naphtha exports reached a record high of ~490 kbd in April amid rising volumes to Japan, South Korea, Venezuela and Brazil. Venezuela crude exports also surged to a seven-month high in April, continuing to support naphtha imports for diluent purposes. Going forward, firm export and domestic blending demand will supporting stronger USGC naphtha cracks w/w through May.

Naphtha E/W physical spread ($/t)

Source: Kpler calculations using Argus Media prices

East of Suez

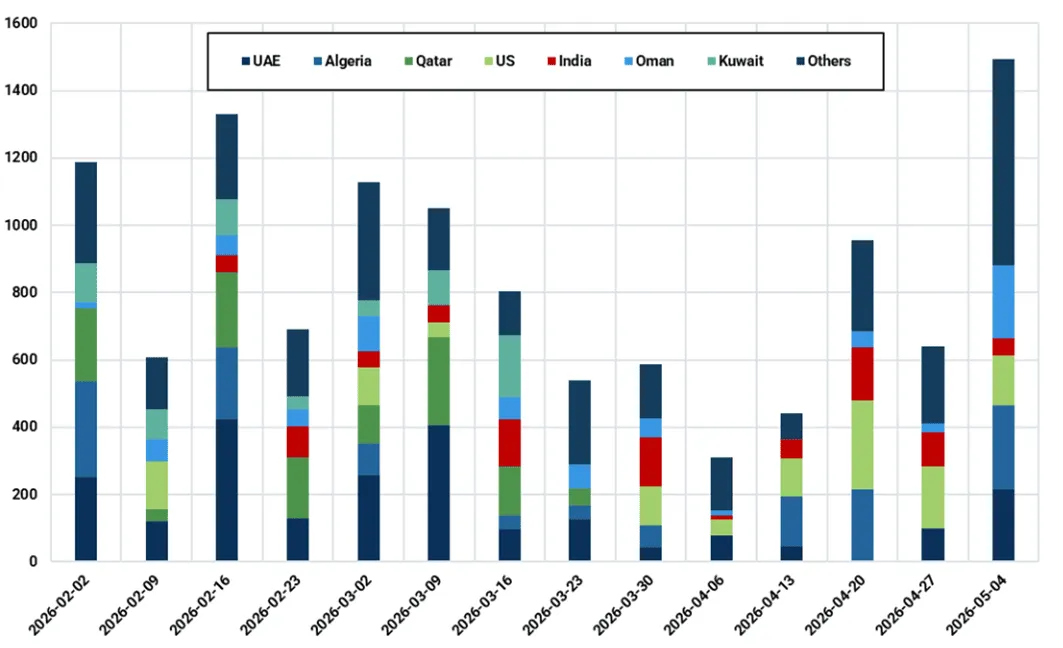

Naphtha cracks in the East strengthened w/w, with crackers gradually raising runs as resupplies from the West arrive, following earlier demand destruction that triggered the olefins crunch.

In Northeast Asia, there are still pockets of inflows from the Middle East this week. Notably, some vessels managed to load from Fujairah and Duqm during US-Iran ceasefire period in mid-April, now reaching the region to provide temporary relief. Furthermore, some refineries are increasing runs (Argus), which will also marginally lift regional naphtha supply in the prompt.

In Japan, naphtha imports from the US set to reach a record high of over 250 kbd next week, as the country seeks to secure alternative feedstock. Japan has also been releasing 20 days’ worth of national oil reserves from 1 May. Officials stated that domestic petchem product supply remains sufficient for the year when taking into account downstream polymer inventories, although we remain doubtful based on the ongoing severity of the crisis.

In South Korea, the $460m support package, imports from alternative sources, and the naphtha export ban imposed since late March have helped stabilise cracker runs rates above 60% (Industry report). That said, we remain sceptical over the sustainability these government measures, as fundamentals are unlikely to improve meaningfully without Middle Eastern barrels.

In China, improving petchem margins has led to state-controlled refiners to shift their yields back toward petrochemicals (Argus). Sinopec has raised run rates at its 1 Mt/year Maoming and 800 kt/year Zhongke crackers in Guangdong, while PetroChina is preparing to increase rates at its 1.2 Mt/year Qinzhou cracker in Guangxi (Argus). A ~10% increase in run rates across these crackers could add ~40 kt/month of naphtha demand, although these integrated units do not rely on imports.

In Southeast Asia, Chandra Asri has also lifted force majeure on polymer production at its Cilegon complex on 2 March (Industry Report).

Overall, recovering cracking demand should continue supporting naphtha cracks. Indeed, downstream olefins tightness remains persistent and is unlikely to ease soon, with further outages continuing to emerge. BASF’s 1 Mt/year butane/naphtha flexi-cracker in Zhanjiang shut last week, likely due to technical issues, while Taiwan’s CPC shut its 700 kt/year No. 6 cracker on 25 April following compressor problems (Argus).

As mentioned earlier, Middle East supply disruptions are unlikely to meaningfully improve in the prompt (even with a deal solving the Strait of Hormuz crisis) given the extent of infrastructure damage and backlog of deliveries of other commodities which would take priority. A pickup in gasoline blending demand into summer, especially in the West, will only mean more pull from marginal barrels, keeping cracks in the East elevated well above seasonal norms this month.

Northeast Asia weekly Naphtha imports by origin country, kbd

Source: Kpler

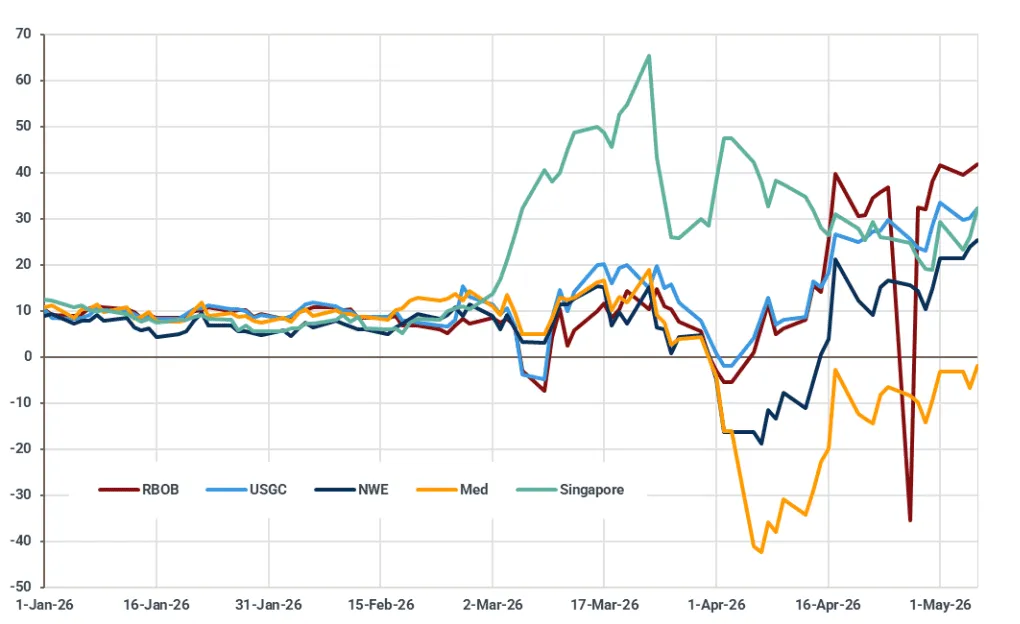

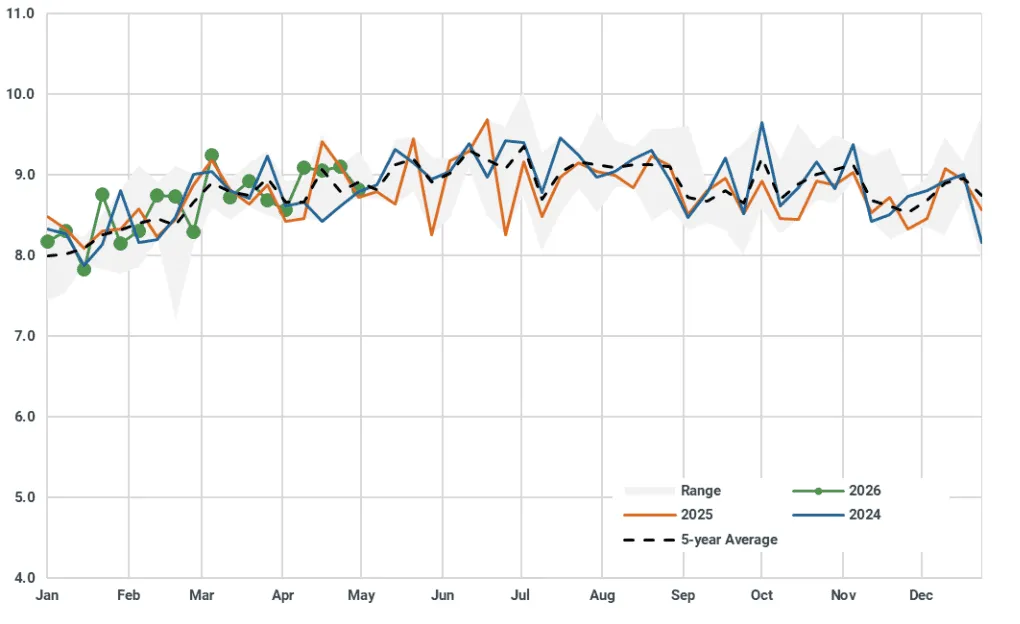

Gasoline: Cracks up, US benchmarks rise to the highest level since 2022

Global Gasoline Cracks ($/bbl)

Source: Kpler based on Argus Media; Singapore 95R crack calculated against Brent.

West of Suez

In the US, benchmark cracks packed further gains w/w, with the USGC up by $7.85/bbl w/w, while RBOB jumped $8.90/bbl w/w, breaking above the $40.00/bbl mark. Both US benchmarks are now sitting at their highest level since 2022, when the outbreak of the war in Ukraine disrupted oil markets.

Yesterday’s EIA release showed total US gasoline inventories down by 2.5Mbbls w/w, dropping to a five-month low and widening the gap to the five-year average to 4%, with PADD 3 inventories remaining below the seasonal range amid elevated exports.

US: Weekly PADD-3 gasoline inventories (Mbbls)

Source: EIA

Gasoline production dropped w/w with yields stabilising around 46.5%, some 4pp below the seasonal average, but production incentives are shifting quickly in the USGC, with both mogas/ULSD spreads and gasoline-adjusted regrades tentatively shifting into max gasoline mode this week.

Implied demand also eased in the latest EIA data, albeit remaining 1% above year-ago levels on a four-week average basis, as retail prices climbed again. At over $4.30/gal, pump prices are over $1/gal above the seasonal average and more than 30cts/gal above the same period in 2022, increasing the financial burden on US drivers with less than three weeks to go to Memorial Day weekend, marking the unofficial start of the summer driving season.

US: Weekly gasoline supplied (Mbd)

Source: EIA

Weekly US Regular Conventional Retail Gasoline Prices (Dollars per Gallon)

Source: EIA

With the market becoming increasingly tight both y/y and vs the five-year average over the coming weeks, we remain bullish on US benchmarks in the near term.

In Europe, cracks also posted sizeable gains w/w, with NWE higher by $12.30/bbl w/w, while the Med 95R gained $7.65/bbl, quickly on the way to positive territory. Fundamentals remain supportive, but the rise in cracks is being tempered by lacklustre export activity.

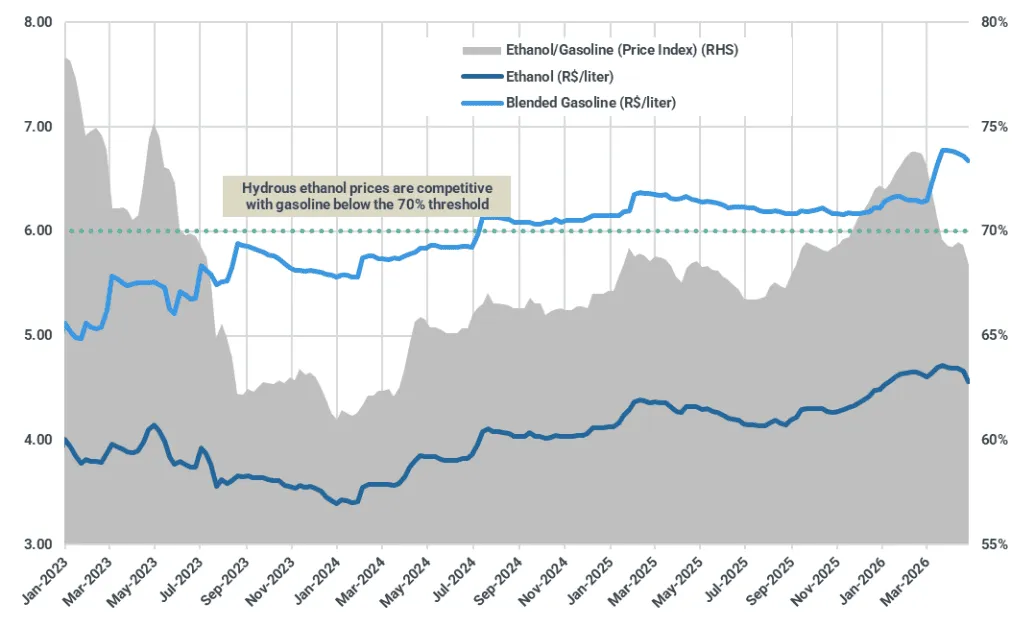

Indeed, despite a wide-open transatlantic arbitrage on paper, transatlantic flows remain moderate, and with Dangote currently running at near full rates and ethanol regaining competitiveness vs blended gasoline in Brazil, poor export activity will moderate the rise in European benchmarks over the coming weeks.

Freight adjusted arb incentive from NWE to US Atlantic Coast ($/bbl)

Sources: Kpler calculations using Argus Media pricing, McQuilling freight data

Brazil: Ethanol and blended gasoline prices (R$/l)

Source: Kpler calculations based on ANP data

East of Suez

The Singapore 95 Ron gasoline added about $2.45/bbl w/w, remaining anchored around $30.00/bbl. The market remains tight, but the gasoline deficit in Asia should begin to narrow this month, while renewed hopes this week for a reopening of the Strait of Hormuz have also affected market sentiment, even if transits remain constrained.

News that China is planning to export more oil products in May, after the export halt at the beginning of the conflict in the Middle East created pressures for state-owned refiners, not least when it comes to storage capacity, coupled with reduced Indonesian buying and high West to East flows over March and April, is also increasing perceived cargo availability within the region, which should help cracks ease from current levels over the coming weeks.

China-Singapore arbitrage incentive ($/bbl)

Source: Kpler based on Argus Media

Middle Distillates: Distillates flashback to the pre-war days

East of Suez

More relative slackening in the Asian jet market was coming to the fore as South Korean May outflows are slated to hit 1 million tons, still comfortably below the government-imposed export cap which is limited to year-ago levels. April saw the lowest jet exports since the Covid-era. This comes as more tapping of SPR crude and lesser maintenance is allowing for more production including gasoil. It is also symptomatic of the bind that many refiners are in, where exporting would allow for greater capture of margin compared to domestic, price-controlled markets (see last week). Added to this expected length, Japanese refinery runs have also been higher on inventory drawdowns. All of which is contributing to a deepening downward adjustment over the last weeks. With demand destruction and a hangover from overbuying, there is perhaps some distance left to run on the current weak trajectory.

Gasoil premiums ($/bbl)

Source: Argus Media

The South Korea export increase comes as the relaxation of the Jones Act has so far proved to be something of a non-event for distillates. Only one vessel carrying jet has landed in PADD 5 from PADD 3, but the first arrival specifically in LA is expected next week. The stocks drawdown in California will accelerate as June is shorter by an estimated 50kbd in PADD 5 overall compared to May. However, with Asian jet coming off, the arbitrage to PADD 5 is starting to become workable on paper, meaning that intra-US flows will likely remain thin.

On a similar theme, while the EFS has weakened sharply, steady arbitraging to West of Suez markets would seem unlikely for the moment, although a newbuild Suezmax has left Jamnagar for Rotterdam, the first cargo since the start of the war.

West of Suez

Physical differentials in Europe have undergone a sharp retracement and barge premiums have flipped negative against the prompt ICE gasoil futures. There has been renewed optimism around the possibility of the Strait of Hormuz reopening – with the resultant drop in outright values reducing the backwardation on futures and swaps curves - as well as selling pressure at the prompt.

This is also taking off some of the workability of US arbitrages to Europe. This is perhaps more of a period of apparent lengthening before an inevitable compression drives values higher – even in the rosiest of scenarios Middle Eastern supply will be reduced for months. An increasingly lighter crude slate in Europe means that distillates production will become increasingly deoptimized.

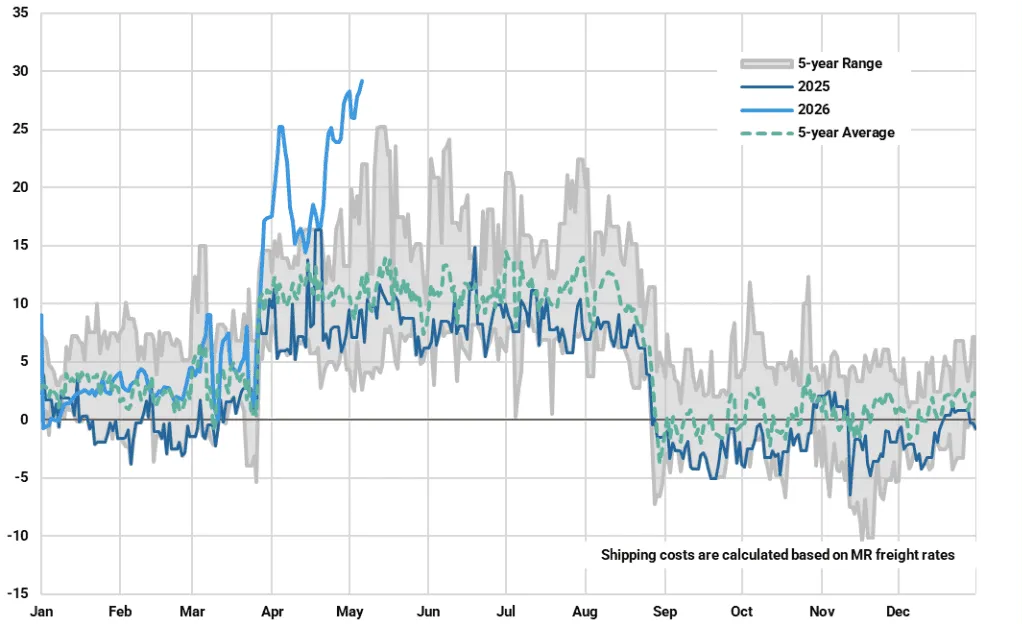

The drop in differentials could also spur more buying form the likes of Brazil who will also be encouraged by US MR freight rates coming back to pre-war levels. As such, the outlook remains robust with this period of lower values unlikely to be the beginning of the end of the crisis. Stocks will trend lower in the near term without Eastern supply setting up a precarious June.

PADD 1 to NWE ($/t)

Source: Kpler using prices from Argus Media

For the USGC, the sharp draw in stocks that started towards the end of March has reversed as exports have slowed. However, this does mean that when the next period of demand returns in the Atlantic Basin, US stocks will be somewhat depleted. Jet has not been immune from the downward correction, but owing to the more extreme nature of the shortage in Europe residual strength will linger.

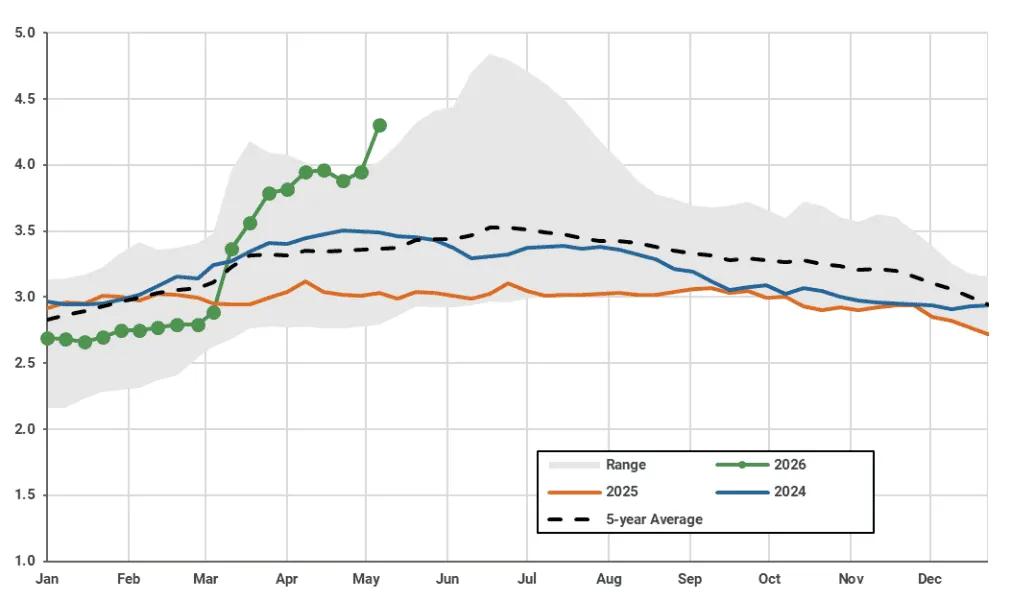

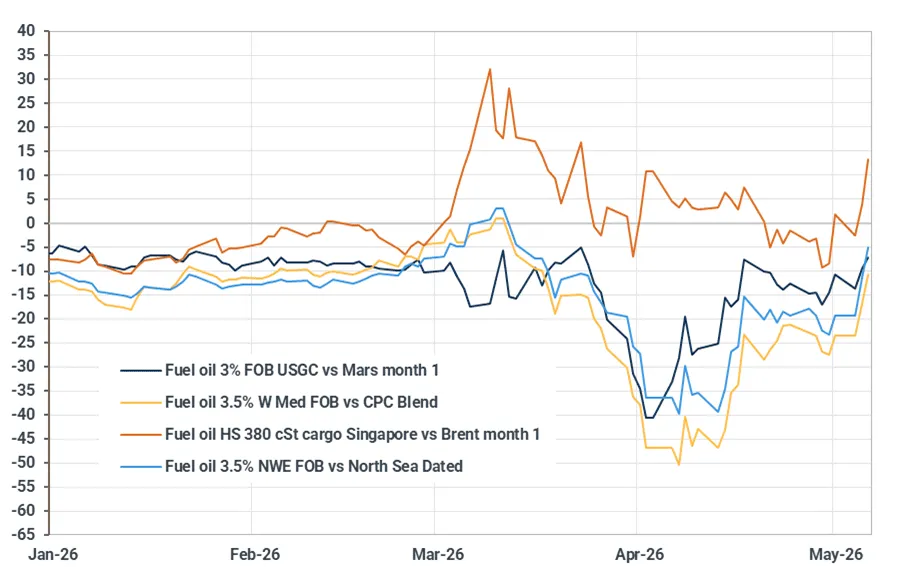

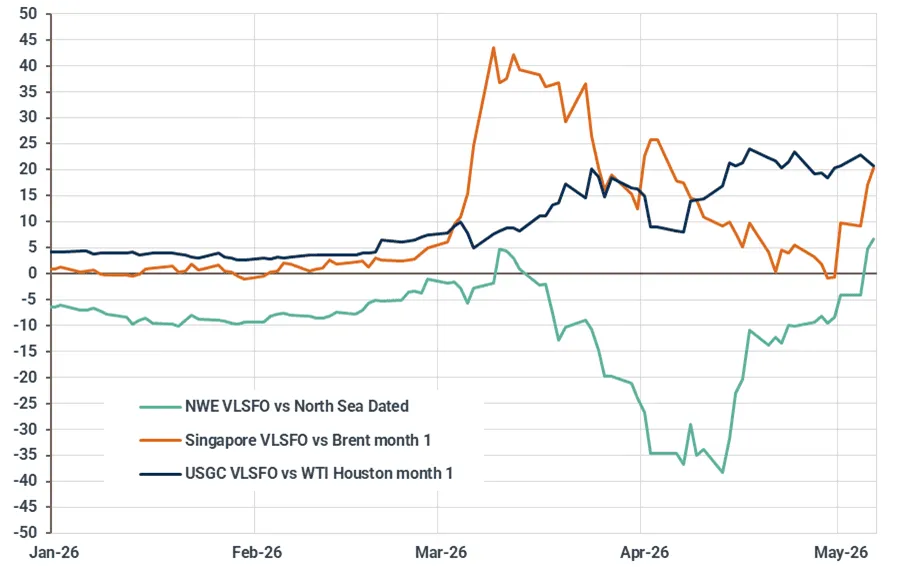

Residues: Fuel oil cracks firm as supply tightens across basins

Global HSFO cracks ($/bbl)

Source: Kpler calculations based on Argus Media data

Global VLSFO cracks ($/bbl)

Source: Kpler calculations based on Argus Media data

West of Suez

USGC high sulfur fuel oil (HSFO) cracks retreated by $2.35/bbl w/w last week before posting fresh gains early this week. European cracks followed a similar pattern.

Mexico's fuel oil exports were steady in the past two months and will potentially increase slightly in May as more refinery capacity becomes available. Mexican barrels will be practically important for the US market amid strong USGC HSFO coking margins and the absence of Middle Eastern inflows. Meanwhile, the US has become an important HSFO supplier to Europe alongside Venezuela, as HSFO/HSSR inflows have remained very low in recent months. Fuel oil stocks in the Amsterdam-Rotterdam-Antwerp (ARA) region dropped by more than 40% from mid-February to their lowest levels since June 2017 (Insights Global). This reinforces West of Suez supply tightness and should support HSFO cracks in the near term.

USGC very low sulfur fuel oil (VLSFO) cracks softened by $2.25/bbl w/w last week but recovered those losses early this week. NWE cracks continued to rebound, flipping into positive territory early this week.

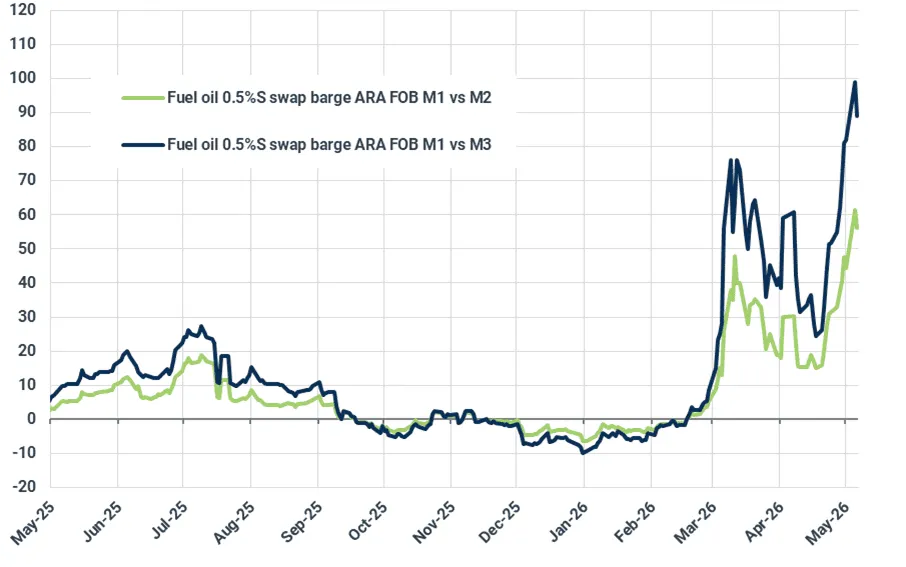

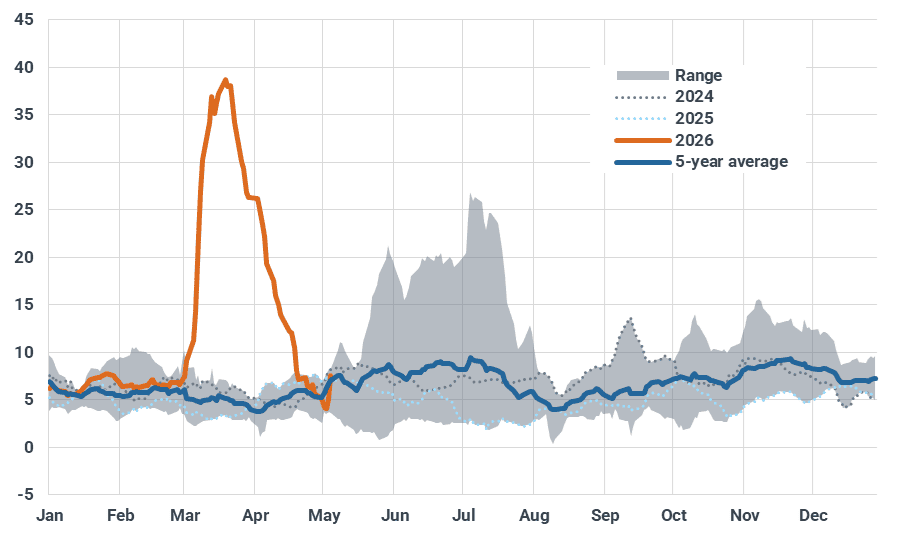

The low sulfur complex in the West of Suez has gained momentum in recent weeks. The USGC Hi-5 spread has widened to its highest level since late 2022, while the differential between NWE 1%S LSFO and 3.5%S HSFO has widened by around $8/bbl since early March. This comes as the VLSFO pool is being stretched by rising vacuum gasoil (VGO) demand from the secondary market, with VGO cracks surging to their highest level since July 2022. NWE supply tightened further as VLSFO/LSFO/LSSR inflows almost disappeared in April. The backwardation in the ARA VLSFO market structure has deepened in recent days, with the M1-M3 spread widening to a record high of $99/t. This also suggests VLSFO cracks will remain firm in the coming weeks.

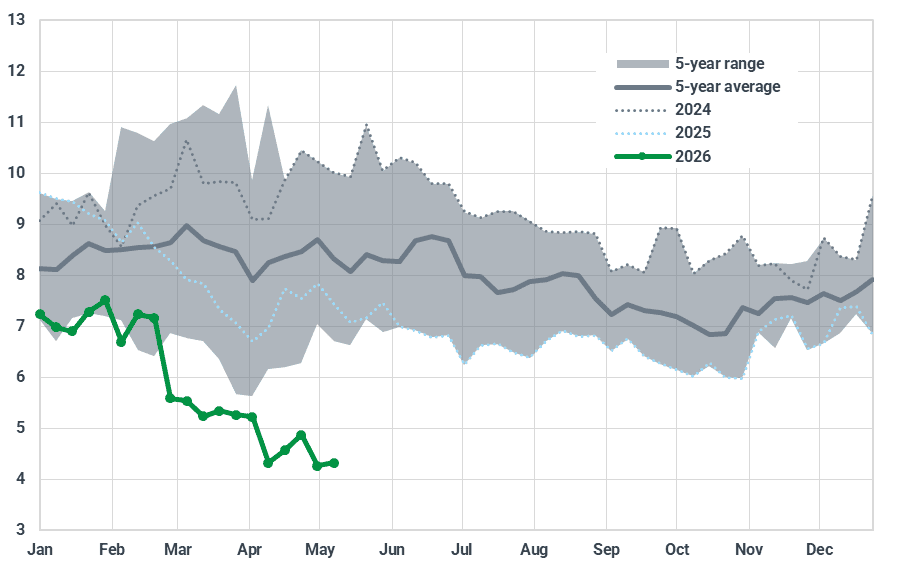

ARA fuel oil stocks in independent storage (Mb)

Source: Kpler calculations based on Insight Global data

ARA VLSFO market structure ($/t)

Source: Kpler calculations based on Argus Media data

East of Suez

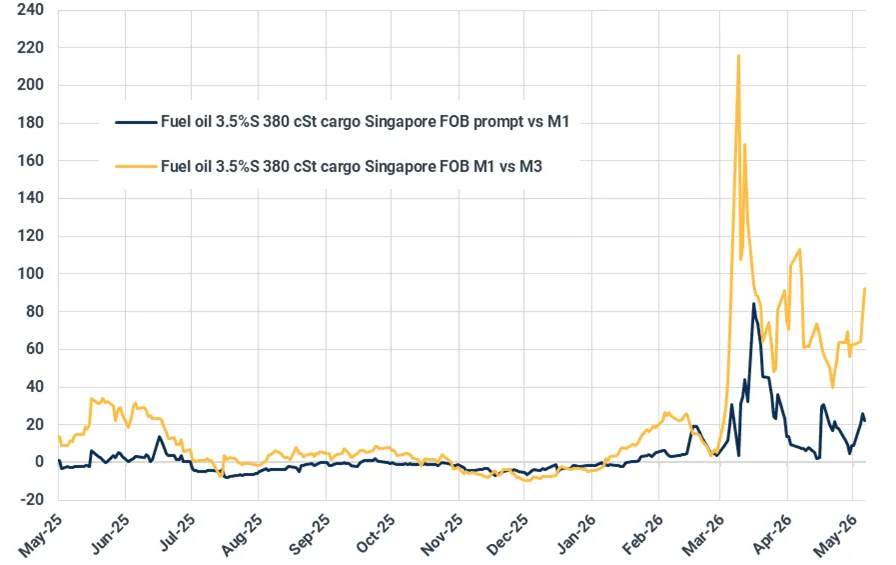

Singapore HSFO cracks fell by $2.15/bbl w/w last week, but rebounded sharply early this week, returning to positive territory after staying in negative territory for two weeks.

Although Singapore HSFO cracks have dropped nearly $25/bbl from their early-March peak, the market structure remains deeply backwardated, with the M1-M3 spread holding around $60-80/bbl for more than a month. This discouraged inventory builds, with Singapore inland fuel oil stocks declining by 5 Mbbls m/m in April to 19.5 Mbbls, the lowest level since May 2025 (Enterprise Singapore). Although strong Russian inflows to Singapore and Malaysia eased regional tightness in April, Egypt and Saudi Arabia have started to increase fuel oil imports from Russia for summer utility use. Without Middle Eastern supply and with heavy reliance on Russian inflows, Singapore and Malaysia's HSFO/HSSR supply sources are highly under-diversified, leaving supply risk elevated in the months ahead.

Singapore VLSFO cracks fell by $1.05/bbl w/w for a seventh consecutive week last week, but rebounded by nearly $13/bbl early this week.

LSFO/VLSFO/LSSR inflows into Singapore and Malaysia trended lower in April after two strong months. The Netherlands and Brazil have become the key suppliers as Kuwaiti shipments remain unavailable and Nigerian LSSR imports decline. However, the East-West spread has narrowed sharply from nearly $40/bbl in mid-March to less than $5/bbl in early May. This suggests inflows from the West will fall, while stronger West of Suez cracks will also encourage suppliers to divert cargoes westward. The Singapore VLSFO M1-M3 spread widened again in early May, reinforcing persistent market tightness amid restrained import sources and reduced blendstock availability.

Singapore HSFO market structure ($/t)

Source: Kpler calculations based on Argus Media data

0.5%S marine fuel Singapore vs Fuel oil 0.5%S NWE Barge ($/bbl, 5DMA)

Source: Kpler calculations based on Argus Media data

Market insights you can trust

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

See why the most successful traders and shipping experts use Kpler