EIA Digest: US crude stocks slide 8Mb as gasoline tightness deepens

The latest EIA weekly petroleum status report delivered another bullish signal for US crude and refined products.

Market & Trading Calls:

- Gasoline inventories extended declines, falling by almost 1.6Mb and settling roughly 2Mb below the 5-year range.

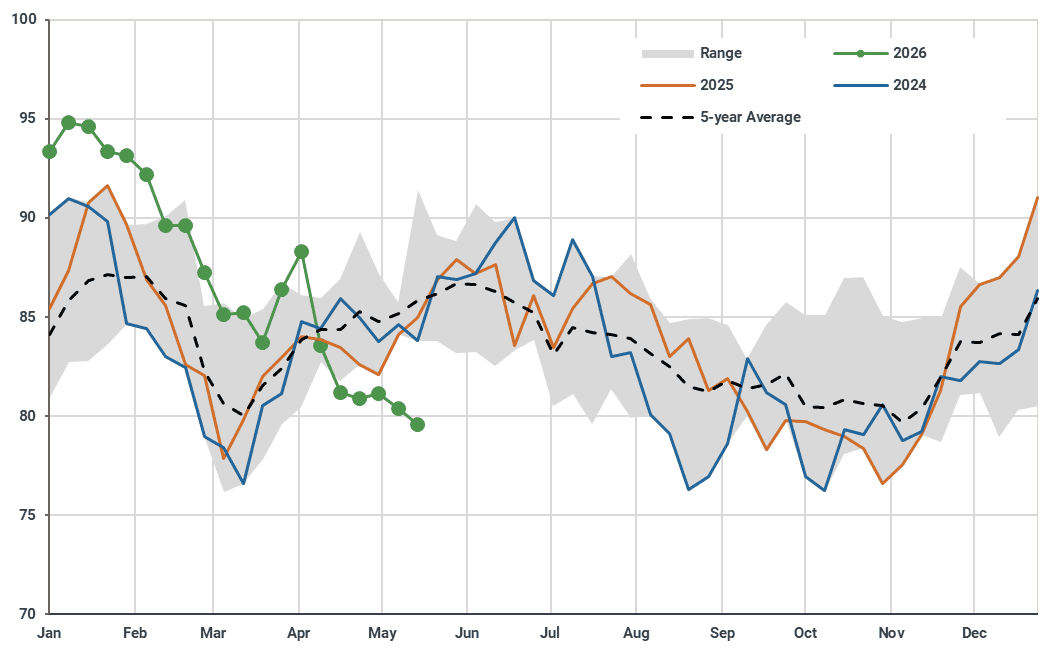

- PADD3 gasoline stocks remain exceptionally tight at around 4.2Mb below the multi-year range, which is attributable to the Jones Act waiver and flows to PADD-1.

- Gasoil/diesel inventories posted a modest 400kb build, although nationwide stocks remain marginally below the seasonal norm.

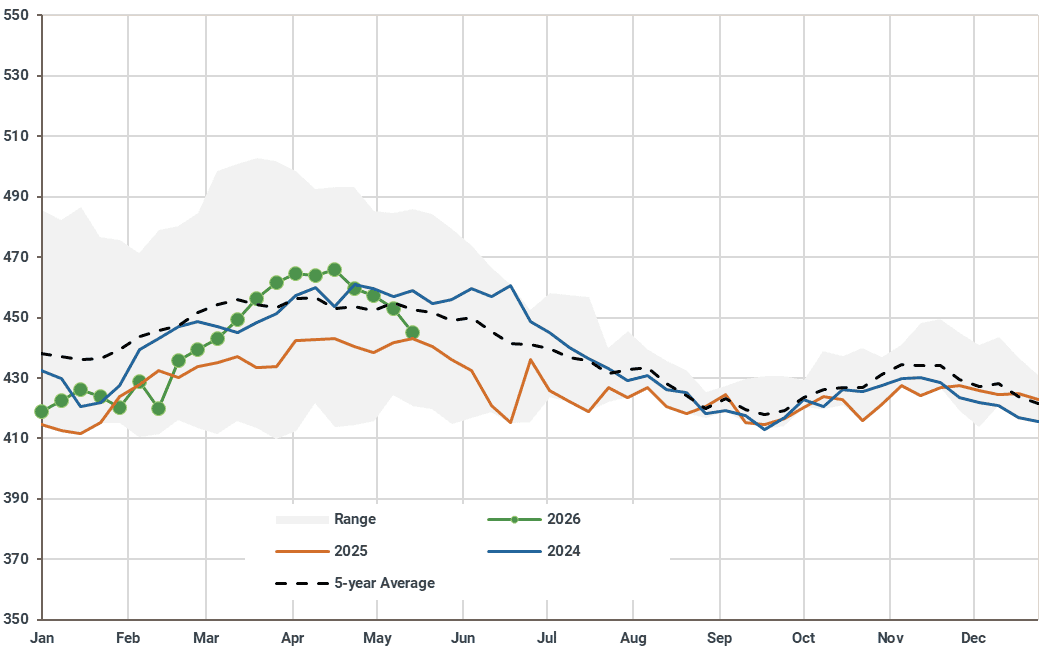

US commercial crude stocks dropped by almost 8Mb over the week ending 15 May in today’s weekly EIA data release. At the same time, domestic crude intake lost some 100kbd w/w, falling behind one and two-year ago levels.

Gasoline stocks extended their draws, this week down by almost 1.6Mb, sitting some 2Mb below the 5-year range. In regional terms, mogas stocks continue to be exceptionally tight in PADD3 (-800kb w/w or sitting some 4.2Mb below the multi-year range), which is a reflection of the Jones Act waiver.

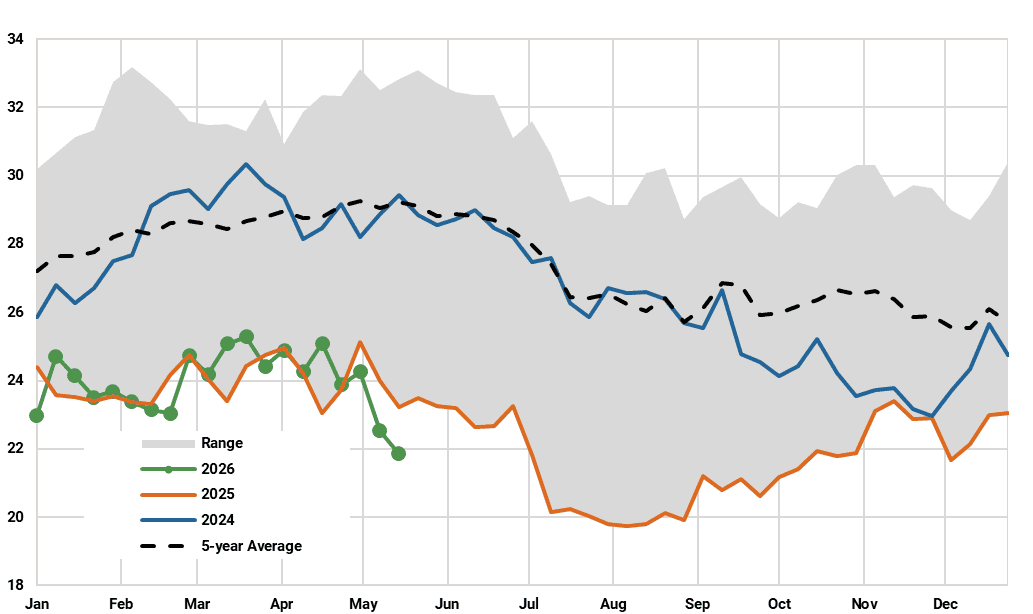

Nationwide gasoil/diesel stocks increased by roughly 400kb, still settling a whisker below the 5-year range. Jet fuel inventories were up marginally by 150kb and fuel oil inventories down by 650kb, with the latter reaching a new year-to-date low, all w/w.

This comes despite sluggish implied demand readings for road fuels as of late, with the proxy for gasoline sitting at 8.77Mbd (-350kbd vs the 5-year average) and the proxy for gasoil/diesel hovering at 3.55Mbd (-300kbd vs the 5-year average).

US: Weekly nationwide crude stocks (excluding SPR) (Mb)

Source: EIA

PADD3: Gasoline stocks (Mb)

Source: EIA

US: Fuel oil stocks (Mb)

Source: EIA

See why the most successful traders and shipping experts use Kpler