From backwardation to contango: European crude diffs reflect ample supply

Ample crude availability in Europe continues to weigh on physical markets, with differentials across the North Sea, Mediterranean and WAF falling to, or even below, pre-war levels. That said, continued geopolitical uncertainty and weak confidence in SOH transits should still provide a floor to prices for now.

Market & Trading calls:

- Stable to pressured Atlantic Basin crude differentials, with potential further downside if Strait of Hormuz crude transits increase in July and Iranian exports are boosted by the sanctions waiver.

- Stable on high Kazakh CPC Blend flows into Europe, as the grade remains the most economical option for regional refiners compared to similar quality alternatives.

- H2 2026 crude output increases in Brazil, Guyana and Venezuela could imply higher crude flows to Europe.

The past few months have reminded us that Europe is not heavily reliant on Middle Eastern crude oil, with most of its needs historically met by countries such as Norway, Kazakhstan, the UK, Turkey, Libya and the US. Middle Eastern oil has typically accounted for only 5-6% of the import slate, or around 500 kbd, into EU-27 countries.

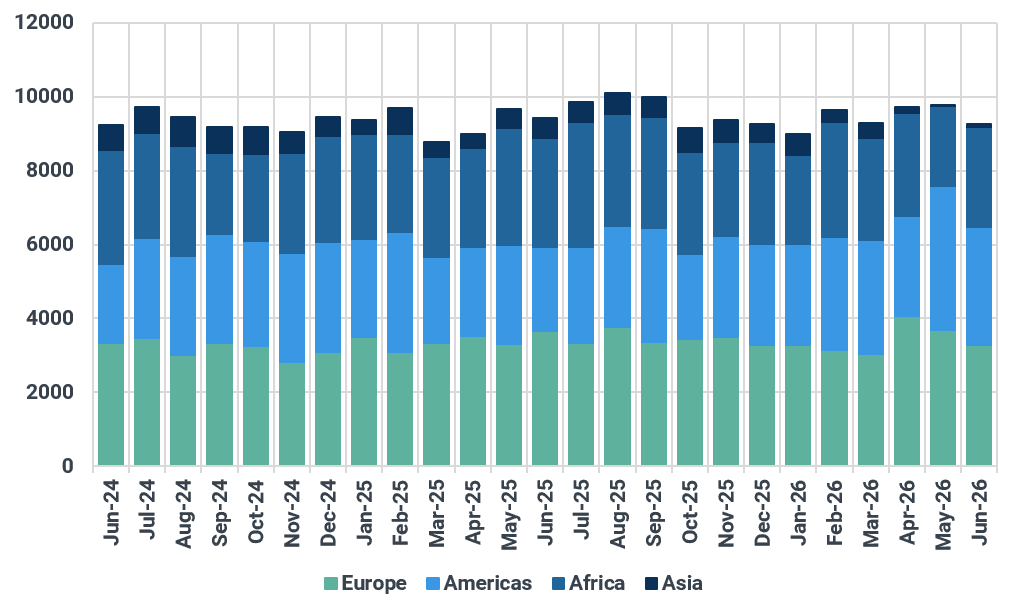

While crude arrivals from the Middle East into the bloc have fallen sharply since March amid the SOH blockade, crude imports from the Americas surged to a record 3.9 Mbd in May and remained at historically elevated levels of 3.2 Mbd in June. This was driven by a sharp rise in US crude imports alongside stronger inflows from Brazil, Guyana, Mexico and Venezuela. Kazakh CPC exports to Europe have also averaged 1.3 Mbd over March-June, 180 kbd above the same period last year, reflecting rising Kazakh crude production in recent months. This month's higher outflows were further supported by the 400 kbd Kashagan oilfield postponing its planned 35-day maintenance shutdown — originally scheduled to begin on 1 June — until next year. Finally, European refinery runs have recently been weighed down by the heatwave, strikes, and low Rhine water levels.

These dynamics have kept total crude imports into the EU-27 at strong levels, allowing EU-27 crude inventories to remain elevated. Kpler data shows the region's crude stocks at 337 Mbbls in June, around 4 Mbbls lower m/m.

EU-27 crude imports, by origin continent, kbd

Source: Kpler

Despite the back-and-forth over the US-Iran conflict and squeezed Strait of Hormuz transits since March, global crude markets have managed to adapt with a combination of bypass routes, crude demand reductions and inventory drawdowns. Crude availability in Europe has also remained ample — reflected in weakening physical benchmarks. Recent progress on a US-Iran deal, along with the 60 days US sanctions waiver on Iran, has further compressed prices.

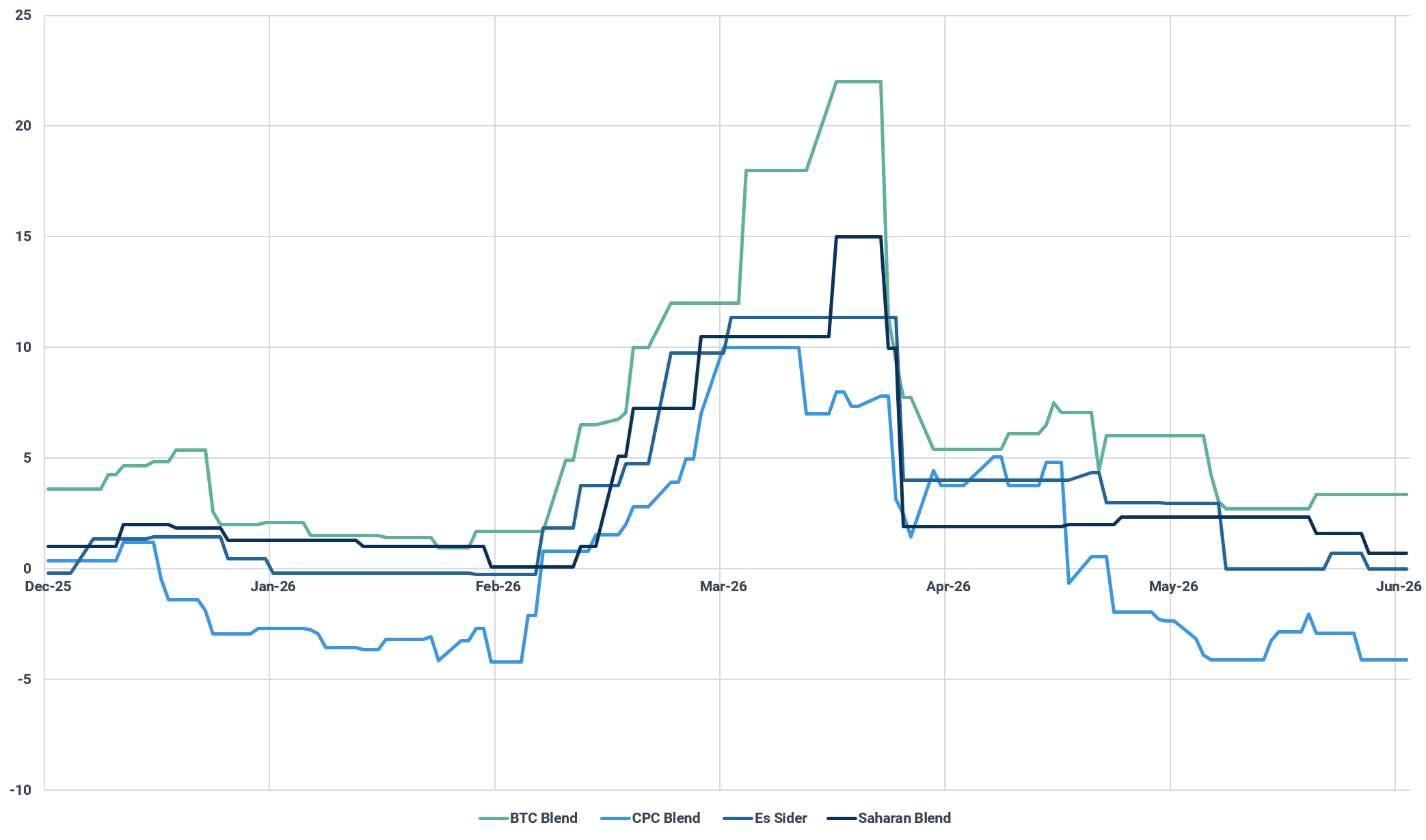

The NSD M1-M3 spread has collapsed from a backwardation of $6/bbl early in the month to a contango of around -$2/bbl in late June, with several differentials across the North Sea, West Africa and the Mediterranean weakening as well. Med light differentials are back to pre-war levels, with CPC Blend trending at -$4/bbl versus NSD (CIF August), close to February 2026 values. Azeri Blend differentials have softened to around $3/bbl against NSD on a CIF Augusta basis — roughly half their late-May levels. Similar pressure has weighed on Saharan Blend and Es Sider, with Es Sider trading close to parity with NSD for most of June (in line with February levels; Argus Media).

Selected Med light crude differentials, cif Augusta, $/bbl

Source: Argus Media

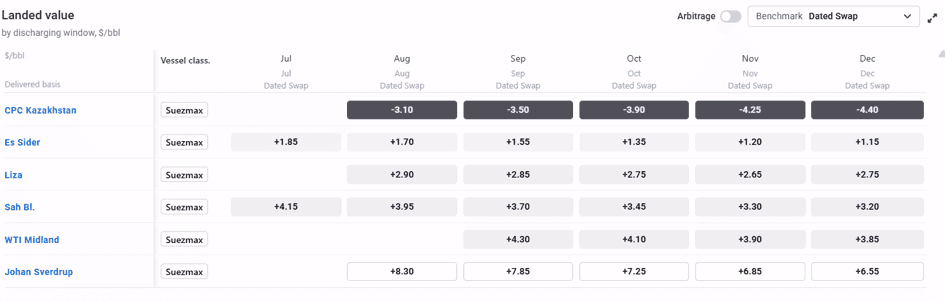

CPC Blend remains the most economical light grade for Mediterranean and NWE delivery over the coming months. The Kpler arbs tool shows CPC Blend arriving in the Med at around -$3.50/bbl for September deliveries (Suezmax) — significantly cheaper than competing grades typically purchased by regional refiners, including Es Sider at $1.55/bbl, Saharan Blend at $3.70/bbl, WTI Midland at $4.30/bbl, and Johan Sverdrup at $7.85/bbl.

Delivered prices of selected grades into the Med, $/bbl

See why the most successful traders and shipping experts use Kpler