India’s fuel austerity hit demand outlook, triggers 40% downward revision to annual product growth

India’s transport fuel outlook is increasingly being shaped by the government’s efforts to preserve fuel supply stability, contain foreign exchange pressures, and manage the growing financial burden on state-run oil marketing companies (OMCs) amid the ongoing US-Iran conflict. Rising crude import costs, rupee depreciation, and growing under-recoveries at state retailers have pushed policymakers to intensify fuel-conservation messaging and administrative austerity measures, which are expected to slow transportation fuel demand growth during the second half of 2026.

Key Takeaways:

- India 2026 refined products demand growth revised down by 77 KBD (39%) from 128 KBD previously to around 78 KBD as rising crude import costs, rupee weakness and government-led fuel conservation measures begin weighing on transportation fuel demand growth during 2H26.

- Gasoline demand faces the largest downside risk, with growth expected to undershoot previous expectations by approximately 5.3% during July-August and around 4% during September, equivalent to roughly 50 KBD, driven primarily by weaker commuting and discretionary mobility trends.

- Diesel demand is also expected to take a 20kbd downward hit to its annualized growth, while jet demand growth remains less in absolute terms, given its modest growth scale.

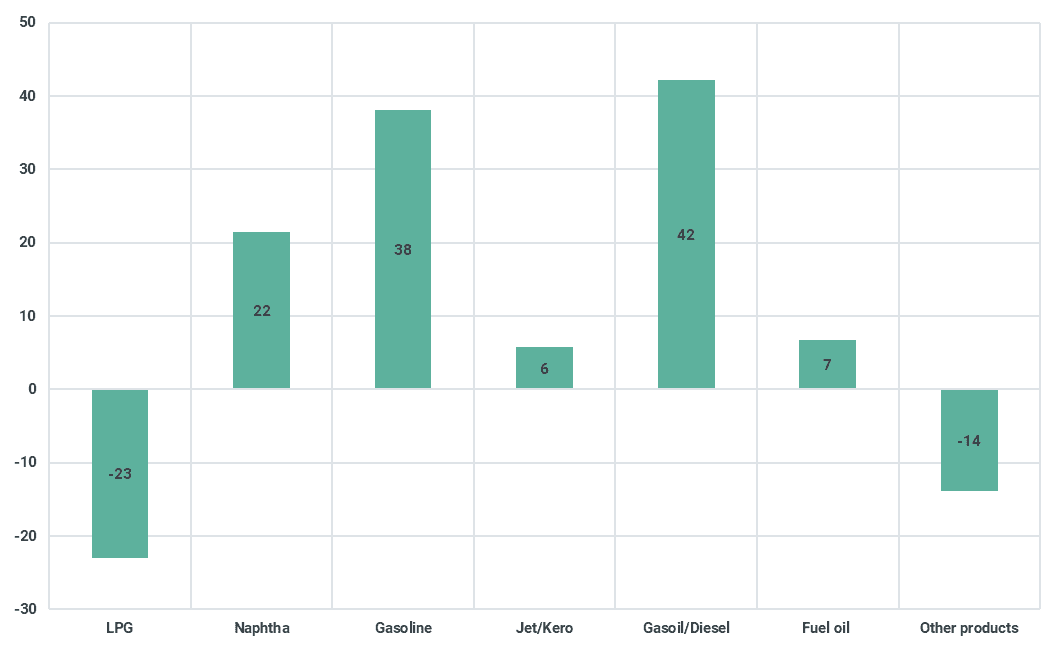

India's 2026 refined products demand growth forecast has now been revised down by approximately 77kbd (39%) from the previous estimate of 128kbd to around 78kbd. The revisions primarily reflect weaker expected growth in gasoline and diesel demand as higher costs, weaker mobility trends, and recent government-led fuel conservation efforts increasingly feed into domestic transportation activity.

Revisions to India’s annual transport fuel demand growth (kbd)

Source: Kpler

India’s macro backdrop has deteriorated since the escalation of the conflict. Higher crude import and refinery operating costs have intensified inflationary pressure, while the depreciation of the rupee has significantly amplified the local currency cost of imported oil. Headline inflation remained relatively contained in April 2026, rising to 3.48% from 3.40% in March, largely reflecting continued government efforts to shield consumers from higher global oil prices through controlled retail fuel pricing. Without these interventions, pass-through from crude and FX weakness would likely have been materially stronger.

The rupee has weakened roughly 6% since the start of the conflict and 10% over the past year. At the same time, FX reserves have reportedly fallen approximately 4.3% since late February as authorities attempt to stabilize the currency, contain imported inflation, and limit volatility in domestic fuel prices.

At the center of the issue is the growing financial stress facing India’s state-run fuel retailers. Retail fuel prices had remained largely frozen since 2022 despite materially higher crude procurement costs and a weaker domestic currency. Although gasoline and diesel prices increased by roughly ₹3/liter on 15 May and by less than ₹1/liter again this week, helping to modestly reduce OMC under-recoveries, the adjustments remain well below the estimated breakeven levels.

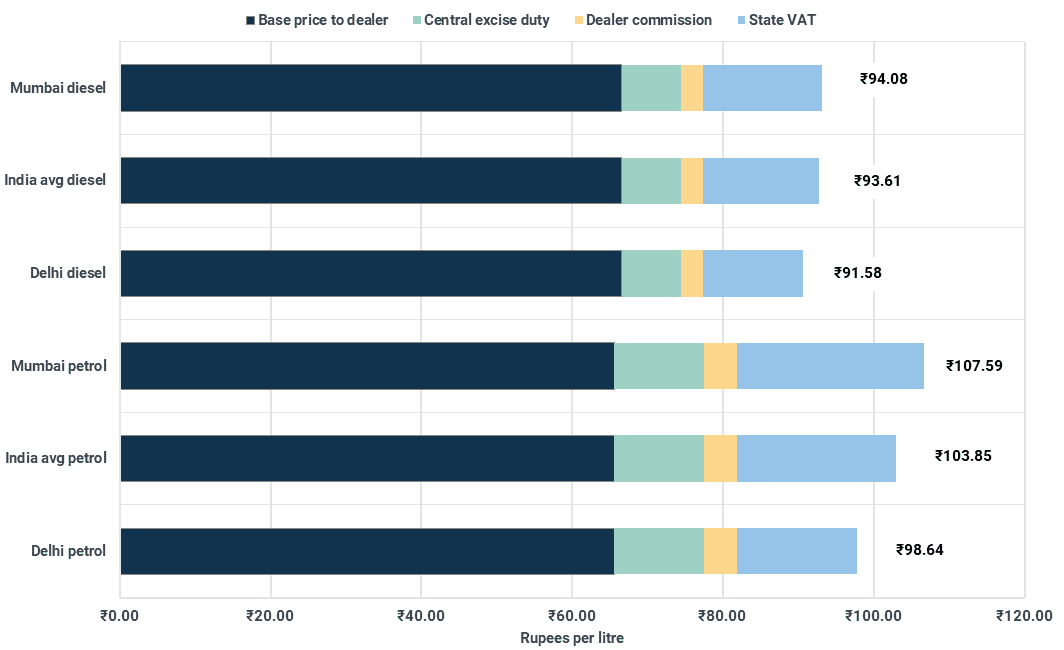

Current national average gasoline prices stand near ₹103/liter, while diesel averages approximately ₹92/liter following the recent hike. Roughly 55–60% of current retail prices still reflect underlying dealer transfer prices and freight costs, with the remainder largely comprising excise duties, VAT, and dealer commissions. Despite the adjustment, current pump prices remain materially below estimated economic breakeven levels.

India retail price build-up - May 2026 (₹/liter)

Source: Kpler, PPAC, Goodreturns, CarDekho

The key issue is the inability of state-run retailers to pass through rising import costs quickly enough to restore profitability. Media reports citing government officials indicate that state-owned retailers are currently losing roughly ₹1,000 crore (c. US$105M) per day as elevated crude procurement costs and currency weakness continue to outpace domestic retail price adjustments.

Based on current fuel demand levels and estimated loss allocations between gasoline and diesel, implied breakeven retail prices remain substantially above current pump prices. Under current assumptions, gasoline breakeven levels are estimated near ₹125/liter versus current retail prices around ₹103/liter, while diesel breakeven levels are estimated around ₹115-120/liter versus current prices near ₹94/liter. This implies the recent ₹3/liter increase offsets only a limited portion of current under-recoveries and leaves state-run OMCs materially below full cost-recovery levels.

The government’s measures came amid rising supply concerns with panic buying and precautionary stockpiling reportedly leaving some retailers temporarily short of fuel. The extension of the US waiver for Russian crude purchases eases near-term feedstock and pricing concerns and reinforces the importance of discounted Russian barrels within India’s crude diet. With Russian imports still running near 1.9–2Mbd and Middle Eastern flows facing ongoing geopolitical uncertainty, Russian crude remains a key stabilizing force for the Indian market.

Against this backdrop, the government has intensified calls for fuel conservation and broader administrative austerity measures, including reduced official travel, increased reliance on virtual meetings and work-from-home arrangements, broader public transport usage, and efforts to curb non-essential fuel consumption. The objective appears less about suppressing economic activity and more about moderating fuel demand growth, limiting imported inflation, preserving FX reserves and reducing the financial burden on state-run retailers.

Our revised framework assumes the impact from austerity measures, inflationary pressure and weaker mobility trends begins feeding progressively into fuel demand mainly from June onward, with the largest downside expected during June-September.

The revisions are based on a bottom-up transportation fuel framework rather than a flat macroeconomic haircut across total demand. Gasoline demand is segmented by end-use category, including commuting, discretionary driving, commercial two-wheeler/three-wheeler activity, and rural/private consumption. The largest downside is assumed within the two-wheeler-dominated commuting segment, which represents roughly 50% of Indian gasoline demand and is expected to be most sensitive to fuel-saving behavior, weaker urban mobility and government conservation messaging. We also expect moderation in discretionary passenger vehicle usage, which accounts for roughly 25% of gasoline demand. Retail prices are likely to continue increasing progressively, although a sudden ₹25–30/liter spike still appears unlikely.

Under current assumptions, gasoline demand growth could undershoot previous expectations by approximately 5.3% during July-August and around 4% during September, equivalent to roughly 50kbd, depending on monthly baseline demand levels.

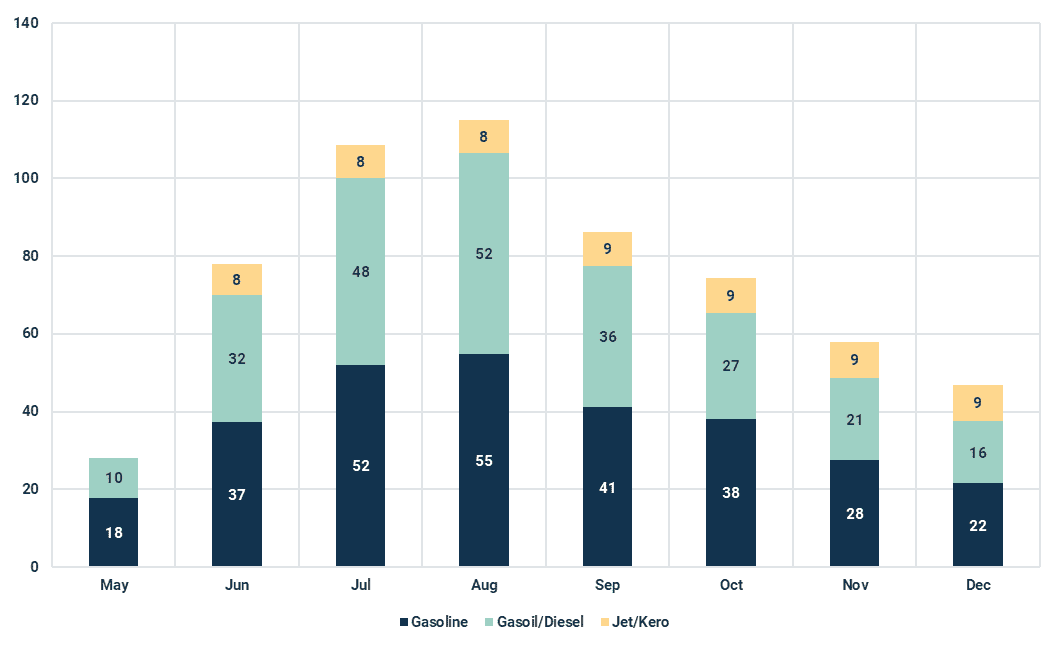

India transportation fuel demand monthly downward revision (kbd)

Source: Kpler

Diesel demand is expected to remain relatively more resilient given its heavier exposure to freight, agriculture, construction, and industrial activity. However, slower industrial expansion and elevated logistics costs are still expected to weigh on overall diesel demand growth during the second half of the year. As a result, annual diesel demand growth was revised down by 20kbd. The monthly adjustments are expected to peak in July-August during the monsoon season, with an average 50kbd downward revision from the baseline.

Calls for reduced foreign travel could also weigh on jet fuel demand during the second half of the year, with annual jet demand growth now revised down by roughly 50%, from approximately 11kbd previously to around 6kbd.

Conclusion

Overall, recent austerity measures suggest Indian policymakers are increasingly prioritizing macroeconomic stability, inflation management, FX preservation and fuel supply security over near-term transportation fuel growth. While the measures are unlikely to trigger outright demand destruction, they are expected to materially slow India’s previously robust transportation fuel growth trajectory during the second half of the year. Unless crude prices ease materially, the rupee stabilizes or additional fiscal support measures are introduced, further retail fuel price increases and additional fuel-conservation measures may become increasingly difficult to avoid.

India annual refined product demand growth (kbd)

Source: Kpler

Market insights you can trust

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler