LatAm’s new barrels arrive as eastbound arbs shut

Brazilian pre-salt production continues to accelerate, but the market is becoming increasingly driven by destination economics. With Eastbound arbs now shut, the next question is not where Brazilian barrels go, but when the economics turn back in their favour.

Executive summary

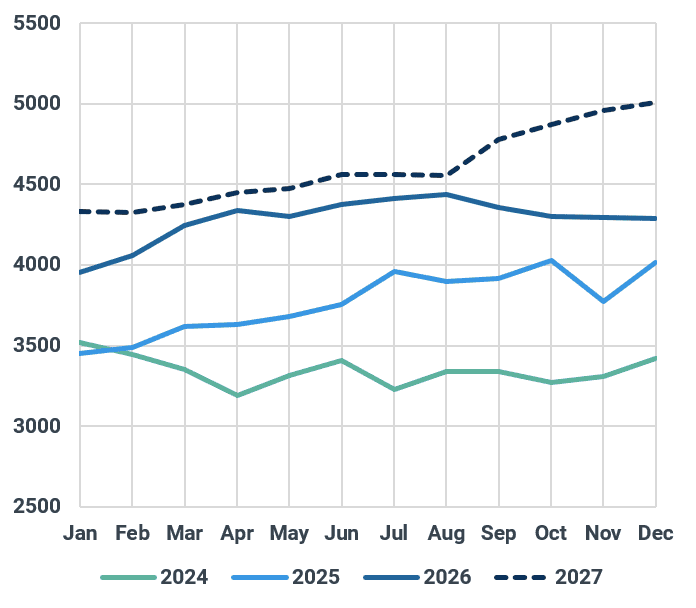

LatAm crude/co supply is rising into a weaker clearing market, with Brazil’s pre-salt ramp already adding close to 400kbd ytd and regional supply expected to increase by roughly 1.5Mbd by 2027. At the same time, cheaper Dubai-linked barrels and higher LatAm-to-East freight have shut Eastbound Mero/Tupi arbs, keeping pressure on implied netbacks. The key swing factor to watch is China, where stronger refinery runs, restocking or SPR buying could reopen the arb and improve sellers' pricing leverage.

Brazil crude/co supply forecast (kbd)

Source : Kpler

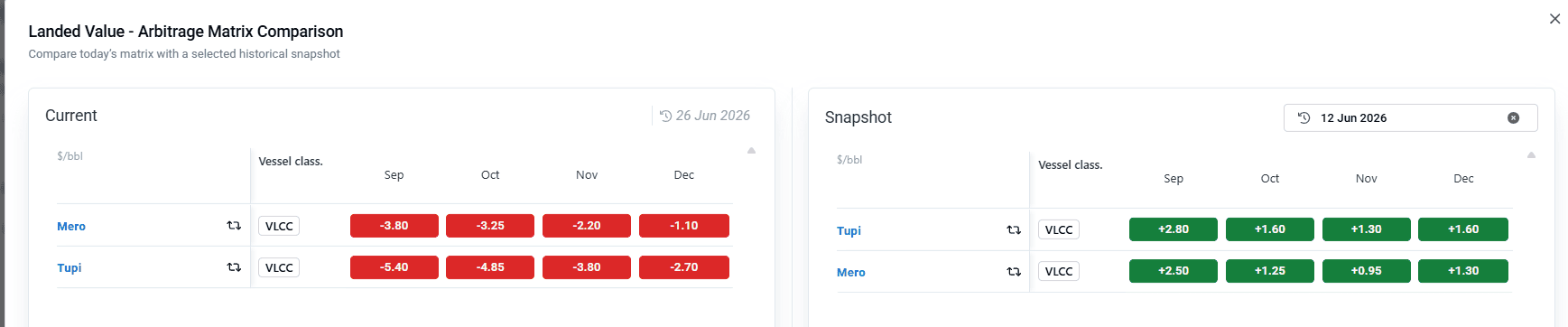

Those extra barrels are now facing a more competitive and well-supplied Eastern market. Strait of Hormuz flows are returning, Dubai-linked barrels have cheapened, and balances are pointing looser by September. Freight has moved against Brazil too, with LatAm-to-East VLCC rates up close to $2/bbl as tonnage shifts back toward the Middle East, tightening prompt Atlantic availability even as demand softens. In mid-June, Brazilian crude still looked workable into East Asia, screening around $2.50/bbl cheaper than Murban for September-delivery cargoes. That window has now shut. With Brazil’s delivered-cost advantage eroded, buyers have less room to pay up, pulling the implied clearing value back to Brazil lower.

Mero/Tupi Eastbound landed-value arb, current vs 12 June snapshot

Source : Kpler

But this does not necessarily point to a structural demand problem. If Chinese buying recovers through higher refinery runs, commercial restocking or strategic reserve buying, the Eastbound arb could reopen quickly. Brazil remains well placed in that scenario, with Mero, Tupi and Búzios offering scale, growing availability and a quality profile that suits complex Asian refining systems.

That is where the commercial question starts. In today's market, sellers may have to accept lower implied netbacks to keep barrels moving. But once the arb starts to reopen, the challenge changes. The cargo is no longer just looking for a home; it is about making sure the improvement in delivered economics is not fully captured by the buyer.

For Brazilian sellers, the risk cuts both ways. Hold out for too much while the arb is shut and the cargo becomes harder to place. Move too quickly when the arb begins to reopen and more of the upside ends up with the buyer. The next opportunity is less about defending a firmer differential today, and more about recognising when destination economics have shifted back in sellers’ favour.

See why the most successful traders and shipping experts use Kpler