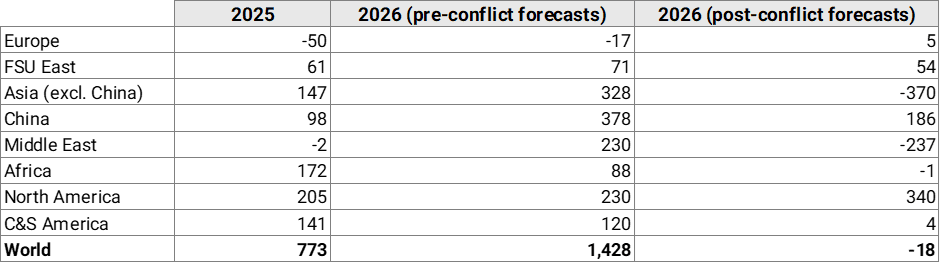

Liquids demand to fall this year, but not as sharply as in Covid-19

Following our latest Refined Products and NGLs S&D release, we consolidate demand estimates for 2026 across regions and products. We now revise total liquids demand from +1.43 mbd y/y growth in our February outlook to a marginal decline of 0.02 mbd, with losses concentrated in Q2-2026, Asia-Pacific, and light ends. While this marks the first y/y contraction since Covid-19, the scale remains far from the 9–10% demand collapse seen in 2020.

Total liquids demand growth (y/y, kbd)

Source: Kpler

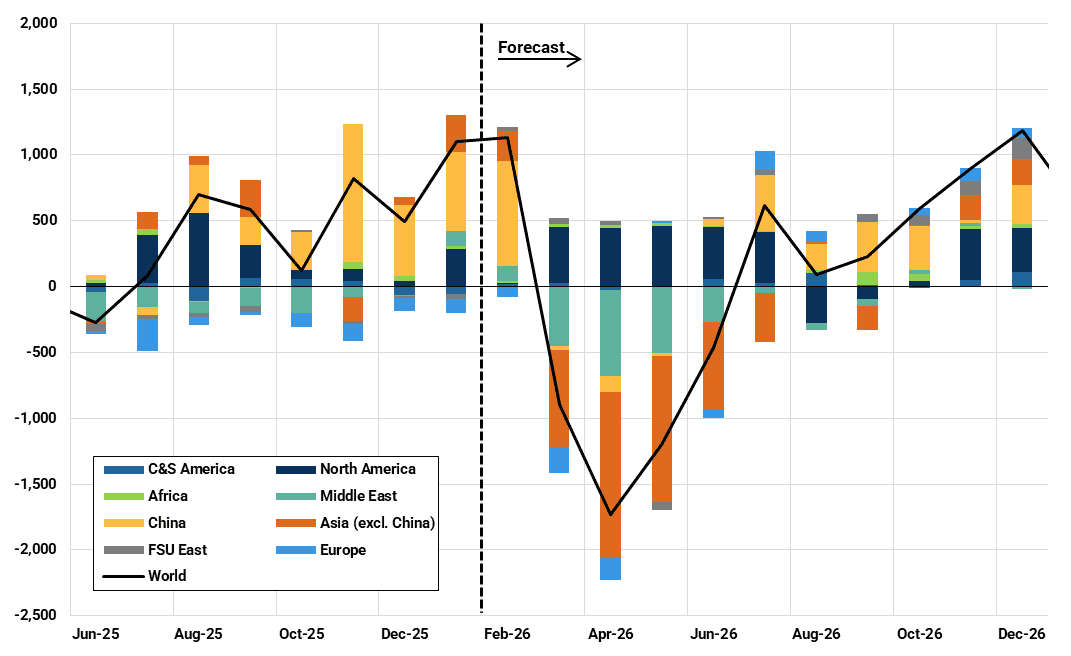

The ongoing US/Israel–Iran conflict is expected to result in liquids demand losses of 4.1 mbd on average in Q2-2026, based on our de-escalation scenario, which assumes normalized transit flows through the Strait of Hormuz by July.

We identify three primary channels driving these losses:

- Immediate disruption to mobility and activity: Direct impacts from military escalation across the Middle East, including airspace closures, flight cancellations, reduced mobility, and a pullback in non-essential industrial and commercial activity.

- Physical supply constraints and policy responses: Fuel and feedstock shortages, the latter mostly pertaining to LPG and naphtha demand from the petrochemical sector, that either constrain consumption outright or prompt demand-side measures, including rationing. This also incorporates offsetting policies in some regions, particularly in Europe, where measures are aimed at cushioning consumers rather than suppressing demand.

- Macro and price transmission effects: Higher prices and deterioration in macro indicators, including inflation and GDP growth, feeding through into demand with varying lags and elasticities across sectors and products.

Among these channels, physical supply constraints exert the most pronounced impact on demand under our current de-escalation scenario. As a result, the adjustment reflects temporary dislocations rather than structural demand destruction, with lost volumes expected to recover swiftly alongside supply from Q3-2026.

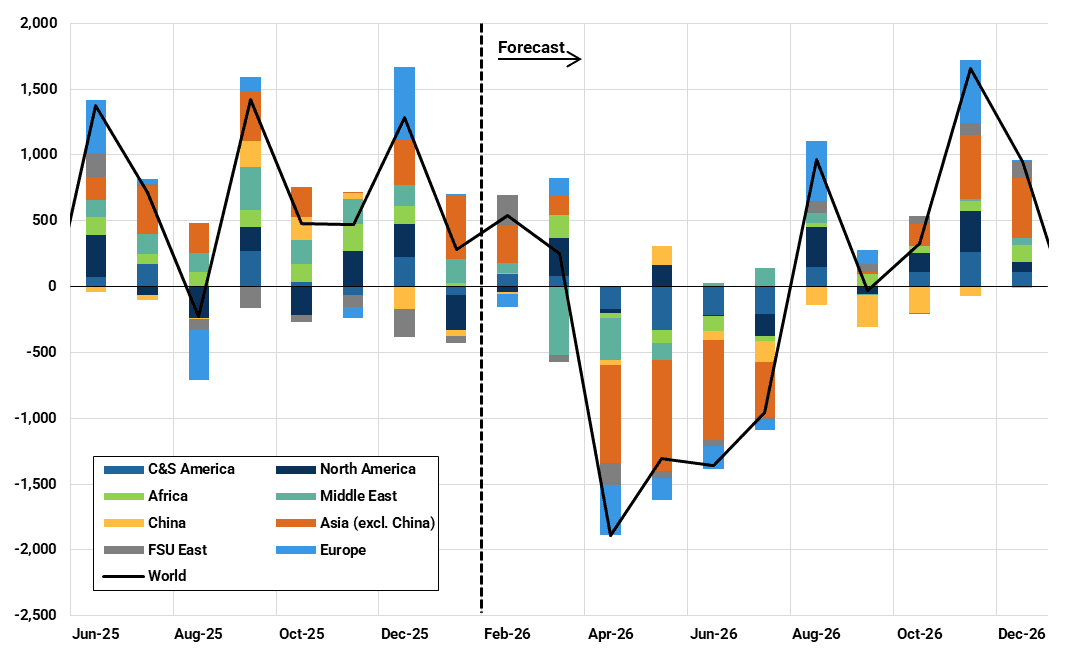

Light Ends

Ethane, LPG and naphtha y/y demand growth by region (kbd)

Source: Kpler

Light ends account for half of total demand losses from the conflict in the front months of our forecast on a global basis. Ethane demand losses are concentrated in the Mideast Gulf, where petrochemical facilities depend on base chemical and cracker co-product exports via the Strait of Hormuz, while also facing operational disruptions due to attacks on upstream and downstream infrastructure.

The bulk of losses, however, are driven by fuel and petrochemical feedstock shortages. India remains particularly exposed, having sourced around 90% of its LPG imports from the Mideast Gulf on average in 2025 to meet cylinder and petrochemical demand, while steam crackers and PDH units across Asia have been forced to cut operating rates or declare force majeure.

Transport Fuels

Gasoline, jet fuel/kerosene and gasoil/diesel y/y demand growth by region (kbd)

Source: Kpler

Transport fuel demand losses are concentrated in Asia, peaking at 1.12 mbd in May under our de-escalation scenario. While this profile is more severe in both timing and magnitude than in our latest written analysis, the underlying drivers remain unchanged. Africa, typically a growth market, is also set to post demand declines through Q2-2026, with East and Southern Africa particularly exposed to fuel shortages.

Elsewhere, Latin America diesel demand is expected to weaken further due to higher exposure to rising international prices. In Europe, the UK and France stand out as the most exposed jet fuel markets, reflecting reliance on Middle Eastern supply and relatively shallow inventories, with peak demand losses of around 100 kbd in July.

Fuel oil demand has been revised lower, reflecting war-driven displacement of bunkering activity away from key hubs in the UAE, Oman, and the wider Middle East Gulf. However, these losses are largely offset by demand shifting to alternative regions as commercial fleet reshuffling and longer-haul voyages increase.

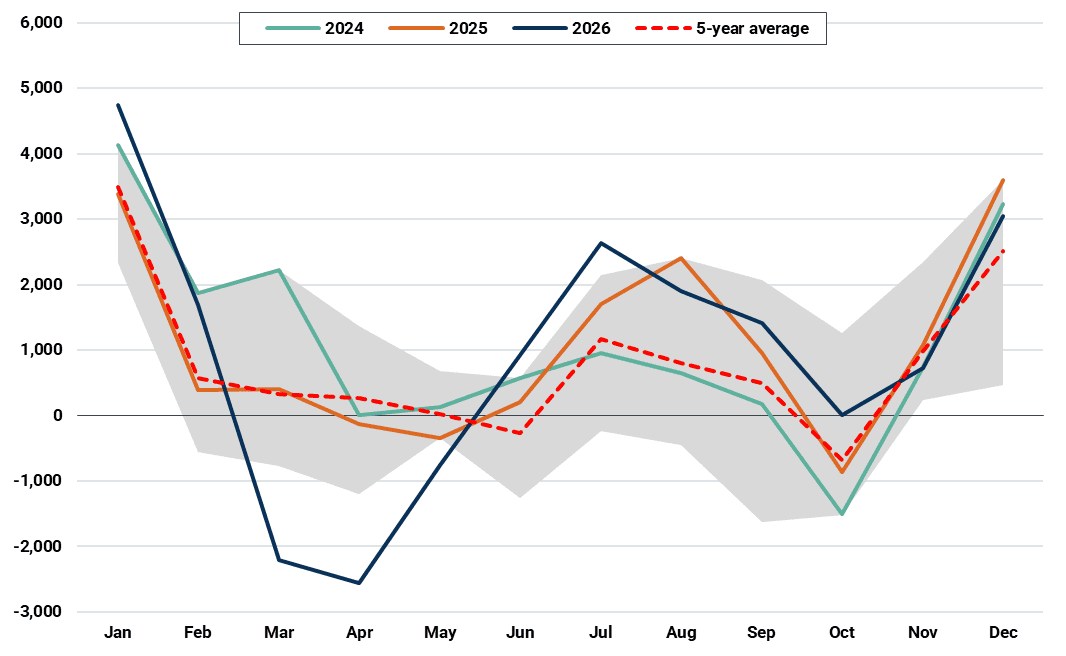

Closing Remarks

Two points are worth highlighting in this outlook. First, risks remain skewed to the downside should the Strait of Hormuz remain effectively closed, as deeper supply shortages and a more adverse macro and price environment would weigh more heavily on demand.

Second, and closely linked, current demand losses are primarily driven by fuel shortages and therefore lag supply disruptions. In this context, tight balances are the root cause of weaker demand, not the opposite, implying that core refined product fundamentals should remain broadly supported.

Core refined products balance (kbd)

Source: Kpler

See why the most successful traders and shipping experts use Kpler