Middle Eastern oil supply recovery could surprise

Renewed Israeli attacks have postponed the formal signing of the US-Iran MoU. As the back and forth continues, we are focusing on the potential timeline and volumes of a Middle Eastern crude and condensate supply return.

Key takeaways:

- The supply comeback could be faster and larger than expected — Iran, Kuwait, the UAE, Iraq and Qatar all show upside surprise potential.

- Most Middle Eastern oil producers would return in weeks rather than months. Our current base case forecast a recovery to pre-war crude and condensate supply of close to 27 Mbd in September (vs 16 Mbd in June).

- Gulf countries' flexibility to ramp up is supported by regional onshore storage (excl. Iran) filled at only around 50%.

As noted in our previous reports, Israeli strikes were identified as a significant downside risk to the US–Iran deal; that risk has now materialised. While news emerged yesterday that the US had lifted its naval blockade on Iranian transits, the Israeli military carried out strikes against Hezbollah across southern Lebanon overnight. Switzerland's Foreign Ministry announced on Friday morning that US–Iran talks have been "postponed," offering no further explanation.

Kpler cargo tracking data show that Strait of Hormuz traffic remains severely constrained; however, a gradual restoration of Iran's crude export logistics may now follow the lifting of the US naval blockade. Kpler has observed more laden Iranian-linked vessels departing Iranian waters with active AIS — notably VLCCs Deep Sea, Hedy, Snow, Starla, and Happiness I, all of which have reappeared on AIS after extended periods of limited visibility. Ballast Iranian tankers are also transiting the Strait with AIS switched on, marking a notable shift from the largely static positioning that characterised many Iranian-linked vessels in recent weeks.

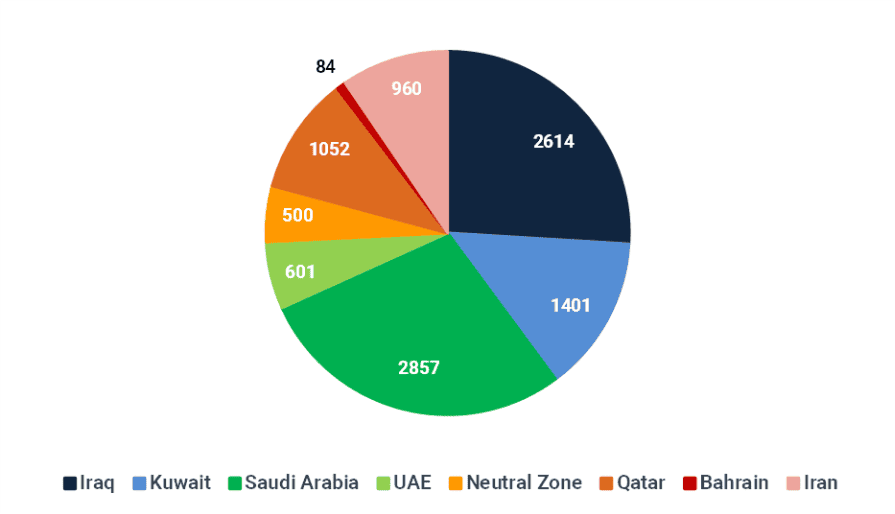

As of 19 June, we estimate that at least 10 Mbd of Middle Eastern crude and condensate production remains shut in, resulting in cumulative production losses exceeding 1.2 billion barrels.

10 Mbd: Middle Eastern crude and condensate supply outages, Mbd

Source: Kpler

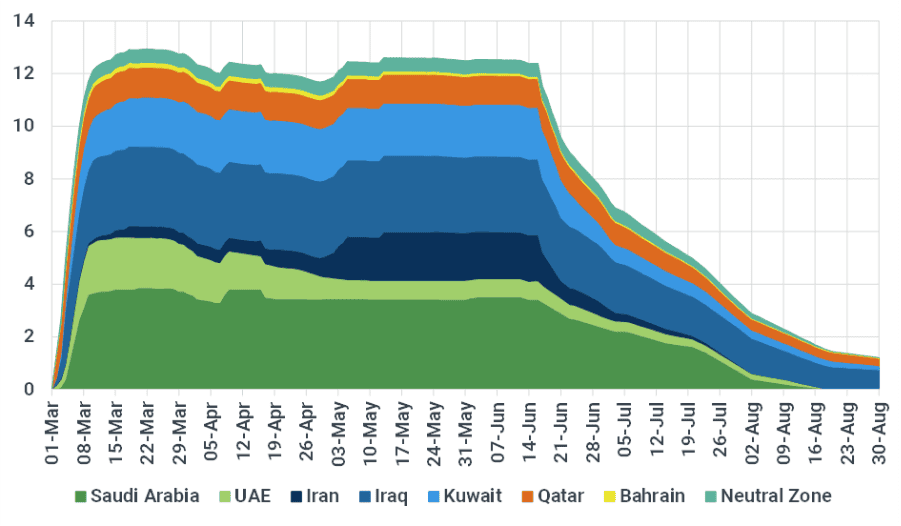

Middle Eastern supply outage forecast by country, Mbd

Source: Kpler

The pace of Kuwait's supply recovery could surprise to the upside. Yesterday KPC stated that the country is ramping up output by 2 Mbd "within one week." While that timeline appears optimistic, it is plausible that Kuwait could begin increasing production in anticipation of near-term export opportunities — even with the Strait of Hormuz still restricted. Most fields could come back online relatively quickly, while a subset of heavier, more complex fields may require up to four months. Kpler data show Kuwaiti crude inventories at only around 50% capacity, and if ballast vessels are available in the region, exports could resume promptly. We therefore estimate Kuwaiti crude and condensate production could rise from approximately 950 kbd in June to 2 Mbd in July and close to 2.4 Mbd in August (vs pre-war of 2.74 Mbd). Should the MoU signing process drag on for several weeks and the Strait remain constrained, these figures would be revised downward.

Iran's recovery pace could also surprise. Assuming the US naval blockade is effectively lifted and exports restart, Iran could see one of the fastest production recoveries in the region. Upstream damage has been limited, and NIOC has extensive experience managing output at scale. Iranian crude production is estimated to have fallen by as much as 1.3 Mbd during the blockade — a consequence of the inability to export rather than any damage to producing assets. Unlike other Persian Gulf exporters, Iran does not require a full restoration of tanker confidence or broader regional security to resume shipments. Iran's oil production is therefore positioned to recover faster than the rest of the Gulf once the Strait reopens. We estimate Iranian crude-only output could reach 3.4 Mbd by August, exceeding pre-conflict levels of 3.2–3.3 Mbd.

Saudi Arabia and the UAE should also be capable of restoring production to pre-conflict levels within several weeks to two months, with the primary constraint being the normalisation of tanker traffic rather than upstream capacity. In the interim, both countries can partially offset logistical bottlenecks by drawing on onshore inventories — currently around 55% full in Saudi Arabia and 44% in the UAE. Recent data showing higher dark exports out of the Gulf of Oman has prompted us to implement an upward revision to UAE supply estimates, now projected at 3.6 Mbd in July and 3.85 Mbd in August respectively, up from 3.3 Mbd in June.

Oil production (February 2026 = 100)

Source: Kpler

We project total Middle Eastern crude and condensate outages to decline to approximately 1.2 Mbd by end-August, with Saudi Arabia and the UAE on track to reach full pre-war production levels in August, contingent on a gradual recovery in transit and exports. Iraqi and Kuwaiti crude supply is expected to return to pre-war levels by November, at which point overall Middle Eastern crude and condensate production should find a new normal — with some residual condensate outages (Qatar, Iran) persisting beyond that point.

See why the most successful traders and shipping experts use Kpler