Russia’s fuel market: supply risks and export implications

Russia’s energy industry has gained experience in managing the consequence of Ukrainian attacks on refineries and other energy infrastructure. As a result, local motor fuel shortages are likely to persist through end of the summer, while any gasoline imports are more likely to be limited test shipments rather than large scale supplies. For global markets, the main implications are likely to be regular Urals cargo insertions and elevated crude exports, less light end exports out of Russia, potentially shorter gasoline balance in Black Sea, shift from ULSD to HSGO in middle distillates exports and quite stable residue flows out of Russia. Significant seaborne gasoline imports into Russia remain unlikely this summer due to mix of factors: number of measures domestic regulators still have, limited import infrastructure, and high delivered cost of such supplies.

Context: domestic supply pressure

Ukrainian attacks on Russian energy infrastructure resulted in increased attention of media to supply of domestic Russian market, especially gasoline. Several complex refineries in the Western Russian have been forced to stop processing recently, including major gasoline producers Moscow and TANECO refineries. Some regions and companies introduced fuel rationing while domestic prices, especially in wholesale segment, have increased.

These disruptions are occurring at the start of high demand season in Russia that typically lasts till September. There are rumours this summer Russia will import seaborne gasoline for the first time in couple of decades. Although the available information remains incomplete, local shortages are already visible in several regions, especially of high-octane volumes. Market participants say that domestic gasoline stocks decreased couple of hundred thousand tons last 3 months. Situation continues to develop and has similarities to what happened in July-September last year when Ukrainian attacks on Russian refineries and contributed to gasoline shortages late in the high demand season.

Potential sources of supply and demand relief:

There are several sources that could help ease the situation – first, Russia underutilizes primary capacity of domestic refineries – thus with some units out others could be put back into operation from stand-by mode and rationalization of crude supply among refineries will shift volumes towards advanced ones in order to produce more finished grades with less crude.

Second, there are already some speculations in the media that quality standards for producers could be relaxed to meet high demand, including return of high-octane additives.

Third, Russia could put on hold mogas rail export to neighbouring countries under intergovernmental agreements (seaborne exports was temporary banned from April till end of July.

Fourth, Russia will rail available gasoline surplus from neighbouring Belarus. Other potential rail suppliers (though small and temporary) could include Azerbaijan and Central Asian countries (later are gasoline short themselves). Source of rail volumes of last resort could be China that has fleet of independent refineries with underutilized capacity – however in that case transportation cost could be very high and at first will be aimed to free and divert production of refineries of Eastern Russia into the western part.

Russia could also address domestic demand rather than supply. One measure could be easing control of retail prices and allowing them to go up. This will support the financials of industry players though this step would be unpopular and thus unlikely to happen before the upcoming parliamentary elections in September.

Seaborne imports, indeed, could happen even this summer, but they are more likely to test import procedures and infrastructure than to materially change domestic supply. Main candidates for supply could be importers of Russian crude – notably Türkiye and India. Volumes at scale at this moment look unlikely for several reasons:

- Russia has been a net exporter of crude and major oil products for decades, so it lacks terminals capable of importing large product volumes by vessel.

- Previous speculation focused on breaking bulk, ship-to-ship transfers and shuttle movements into Russia, but frequent Ukrainian attacks on vessels would make such operations risky from both safety and environmental perspectives.

- Delivered import prices would be significantly above domestic prices. Domestic prices are currently calculated as a netback to European benchmarks minus potential transportation costs, while imports would be priced at benchmarks plus transportation.

How the situation could develop:

Local shortages are likely to continue spreading and worsening as Ukraine targets both refining and logistics infrastructure. Whether this develops into a nationwide shortage before the high-demand season ends in early autumn remains uncertain and will depend on several factors, including some that sit outside market analysis.

Implications for the global markets:

Crude: Lower available primary refining capacity could leave more crude oil available for export. At least 400 kbd of additional spare export capacity is still available unless Ukraine intensifies attacks on export and transport infrastructure. However, because Russia’s energy industry has gained experience in restoring operations after attacks, any increase in exports may be sporadic and short-lived.

Light products: Gasoline and naphtha exports out of Russia are likely to remain lower until the end of the high-demand season. Black sea gasoline balance could be shorter with the diversion of Azeri and/or Turkish volumes into Russia.

Middle distillates: Lower utilization of complex primary capacity could reduce diesel production and exports and increase HSGO flows.

Residues: Fuel oil export volumes are unlikely to see a major impact.

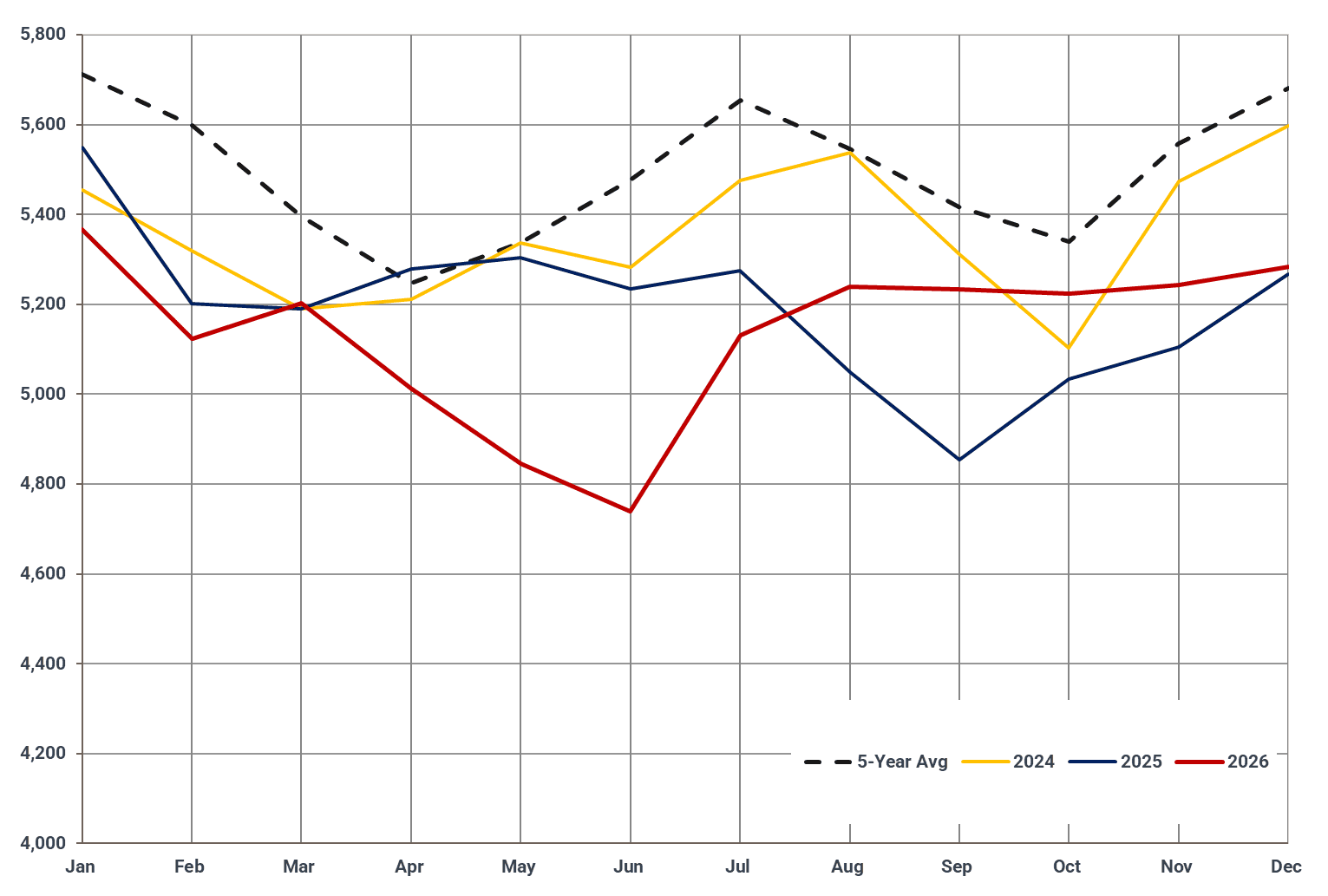

Russian refineries crude intake (kbd)

Source: Kpler

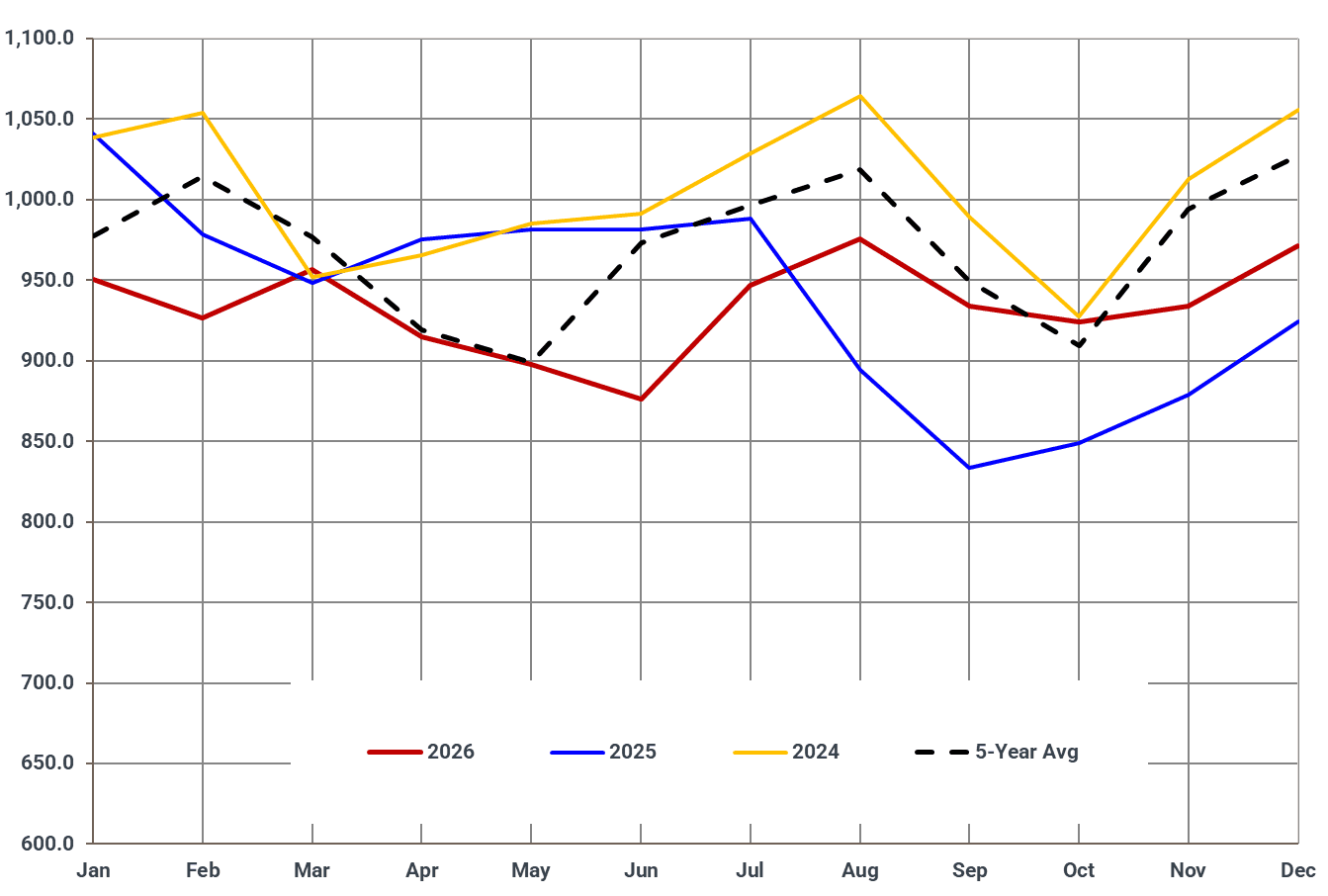

Russian refineries mogas output (kbd)

Source: Kpler

Market insights you can trust

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler