Why hasn’t the clean tanker market corrected (yet)?

Atlantic dirty tanker rates have returned to pre-conflict levels under pressure from tonnage migration, while clean rates remain elevated due to continued clean-to-dirty switching and reduced tonnage in the West of Suez. The drop in dirty earnings has widened the premium for clean vessels, limiting further expansion of the dirty LR2 pool. Meanwhile, tighter Atlantic CPP balances could curb exports to the East, with the clean market likely to correct more gradually due to slower underlying dynamics.

Market and Trading Calls:

- Atlantic dirty tanker benchmarks reverted to pre-conflict levels over April, pressured by tonnage migration.

- Clean rates, however, remain elevated due to further clean-to-dirty-switching as well as a net negative tonnage migration into the WoS

- The correction in dirty benchmarks has pushed clean earnings to a premium to dirty ones, placing a lid over further increases in the dirty LR2 pool.

- Tighter Atlantic CPP balances are likely to see exports to EoS settle lower going forward.

- The clean tanker market is headed for a correction, but slower market dynamics suggest a more gradual easing in rates.

As the de facto closure of the Strait of Hormuz (SoH) pivoted Ton-Mile growth to the Atlantic basin for both the dirty and clean markets, the first fortnight of April saw the dirty (ex. MEG) tanker market correct from the post-conflict highs, partly as the arrival of VLCC ballasters from the East, put pressure on USG assessments, with the weakness eventually cascading to mid-sizes. A similar correction has yet to emerge in the clean sector, particularly in the Atlantic basin, as East of Suez (EoS, excluding MEG) markets were not significantly supported by the conflict to begin with; elevated feedstock costs and the loss of MEG CPP volumes have instead led to reduced refinery runs and the implementation of export controls.

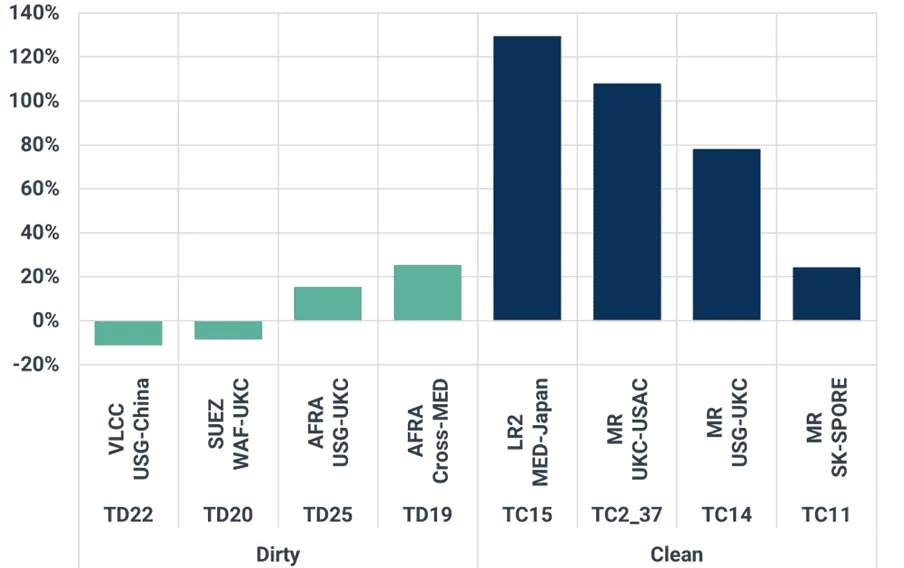

As of the time of writing, VLCC and Suezmax benchmarks have dropped below the pre-conflict levels, leaving the last signs of strength with Aframaxes, whereas LR2 assessments continue to trade circa 130% above pre-conflict levels, a figure that slips to 90% for transatlantic MRs.

Change in key (excl. MEG) tanker assessments (present vs pre-Iran war)

Source: Baltic Exchange, Kpler

Partially offsetting the pressure from the loss of MEG volumes and the knock-on impact on CPP exports across the rest of the EoS market, the clean tanker sector has been supported on the demand side by a surge in Atlantic trade with the East. This mainly features US to APAC, with special reference to Oceania, as well as Europe to Southern/Eastern Africa and Asia flows. While this mirrors an increased pull of Atlantic crude volumes from EoS refiners, a similar tonnage-relocation-driven correction has not yet been observed in LR2s and MRs, as has been the case for VLCCs.

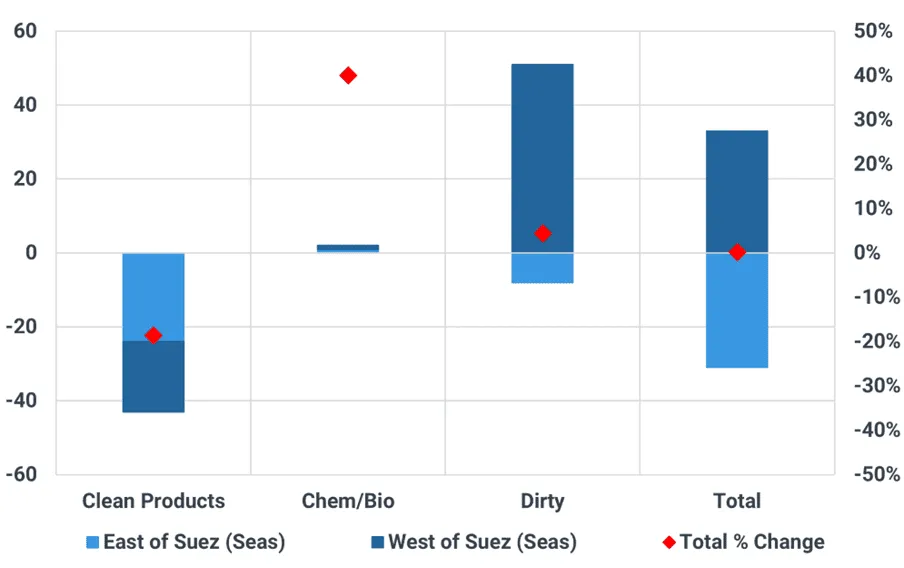

Starting with LR2s, unlike VLCCs, where the loss of MEG barrels naturally pushed tonnage toward the Atlantic, the most attractive option for LR2s, dictated by earnings economics, has been a shift into dirty trades in the Atlantic. In the first month of the conflict, the spread between dirty and clean earnings in the basin averaged $80k/day, exceeding the previous record set before the Russian crude price cap was enforced in 2022. This has triggered further clean-to-dirty switching. Comparing the current employment of the LR2 fleet across basins and products with that before the war, it becomes clear that clean tonnage supply has declined in both EoS and WoS, tightening supply and sustaining clean LR2 freight rates.

Change in Aframax/LR2 employment across basins and commodities (present vs pre-Iran war)

Source: Kpler

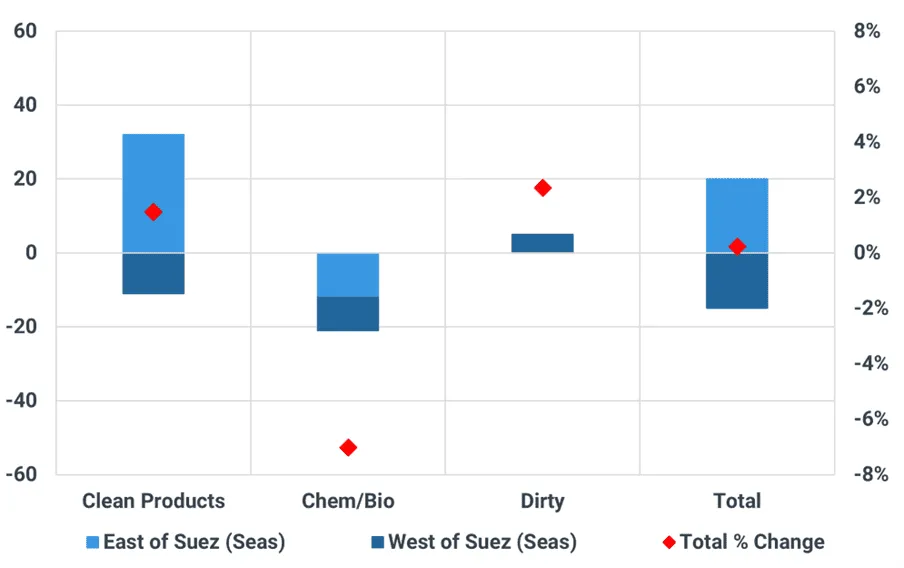

When repeating the above depiction in the case of MRs, however, we reach very different conclusions. While the clean MR pool has increased, seemingly driven by an exodus of tonnage from the Chem/Bio trades, the impact is geographically skewed. Most of these vessels, as of the time of writing, remain in the EoS , with the WoS market actually seeing a decline in tonnage. This appears somewhat counterintuitive, given the large migration waves recorded since the onset of the Iran war.

Change in MR employment across basins and commodities (present vs pre-Iran war)

Source: Kpler

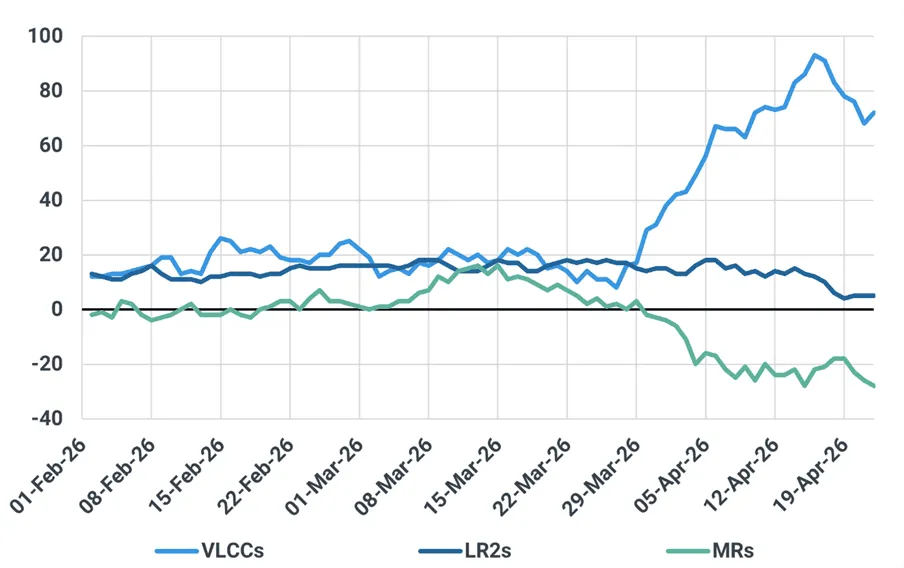

A key factor has been the imbalance between laden and ballast flows.

A more detailed look sheds some light behind this development. Unlike VLCCs, in the case of MRs and to a lesser extent LR2s, the exodus of laden tonnage from West to East has outpaced the inflow of ballast vessels, preventing a significant lengthening of the basin’s position lists.

Net migration into the West of Suez markets by vessel type

Source: Kpler

The above observations help us assess whether a correction in the clean market is underway and understand the mechanisms through which it may occur. In the case of LR2s, dirty-to-clean switching appears necessary for the market to correct itself. The Atlantic Aframax market has already experienced a notable correction, particularly on longer-haul routes (TD25 and TD19), gradually creating a financial incentive to lengthen the clean pool. Indicatively, mid-April saw Atlantic dirty earnings switch to a $14k/day deficit versus the clean ones. However, unlike dirty-ups, clean-ups are considerably more time-consuming, which, on the one hand, calls for a sustained premium in cleaning earnings, while, on the other, suggests a gradual correction in the market.

In the case of MRs, market mechanisms appear more complicated. On the one hand, trickle-down pressure from LR2s will eventually start biting into MRs by poaching interbasin cargoes. In the USG LR loadings have thus far in April reached 156 kbd, the highest In Kpler’s recorded history.

Most importantly, however, net migration in the WoS would need to turn positive. This can be achieved by either a surge in ballasters migrating from the East or more barrels trading within the Atlantic, curbing laden outflows. Focusing on the former, compared to VLCCs, the pool of EoS MR ballasters resulting from the SoH closure appears more modest, offering limited support for such a surge. However, clean exports out of EoS (excl. MEG) have further dropped this month, which, combined with a towering spread in the earnings of the two basins, is likely to lead to more transpacific ballasters, a process that, due to the voyage times involved, sets once again the stage for a gradual correction of the market. It’s worth noting that high fuel prices remain unsupportive of the large ballast legs required for East-to-West migration, with the cost of a trans-Pacific voyage assessed at roughly $800k, while that from the Arabian Sea to USG is higher than $1m. As a result, many owners continue to opt for a wait-and-see approach, betting on a quick resolution of the SoH crisis.

At the same time, the case for increased intra-Atlantic trading continues to strengthen. On the gasoil front, Ukraine’s ongoing drone campaign against Russian refining and export infrastructure is expected to tighten MED and LatAm balances, supporting greater US Gulf buying. Eastern buyers are also likely to face stronger competition for European gasoline from the US, as domestic demand rises seasonally, highlighted by a recent draw in PADD1 inventories after tracking the upper end of seasonal norms for much of the year. On top of the above, European refining margins have recently turned negative, with the Kpler refining team pointing to rising pressure on export-oriented regions that could curb total exports out of NWE.

Considering the above, the key takeaway is that the Atlantic clean tanker market is heading towards a correction, though this is expected to be more gradual than in the dirty segment. Looking at the broader picture, a prolonged Strait of Hormuz crisis requiring sustained inter-basin trade is likely to trigger alternating waves of positive and negative tonnage flows into the WoS basin, leading to similar fluctuations in freight rates. This dynamic could also extend to the dirty markets.

See why the most successful traders and shipping experts use Kpler