Why the real oil shock may only begin when China returns

The oil market has so far avoided a full-blown supply shock through inventory drawdowns, rerouted Middle Eastern flows, higher WoS exports and refinery run cuts across Asia. But the market’s uneasy balance also rests on one often overlooked reality: China has yet to return as a major crude buyer.

Key Takeaway:

- Chinese refiners have scaled back crude buying from both sanctioned and compliant markets amid elevated oil prices and weak refining economics, keeping China largely absent from the global crude market.

- The sharp slowdown in Chinese crude imports is now outpacing refinery run cuts, accelerating inventory drawdowns despite subdued domestic fuel demand.

- As independent refiners reduce operations and refined product inventories stop building, state-owned refiners may increasingly find room to raise runs and return to the crude market in the coming weeks.

- The current oil market balance remains tighter than it appears. Once China returns to the crude market, physical prices could reprice sharply higher.

Physical crude oil benchmarks appear to have settled into a $100-$120/bbl range over the past two months, after the initial wave of panic buying during the first month of the US-Iran war briefly pushed prices above $150/bbl. Beyond SPR releases by multiple countries — particularly the accelerated drawdown in US stockpiles — one key reason oil prices have not sustainably moved above $150/bbl despite a structural supply loss of 8 mbd from the Middle East is the absence of Chinese buying in the market.

But how long can China continue to withhold procurement?

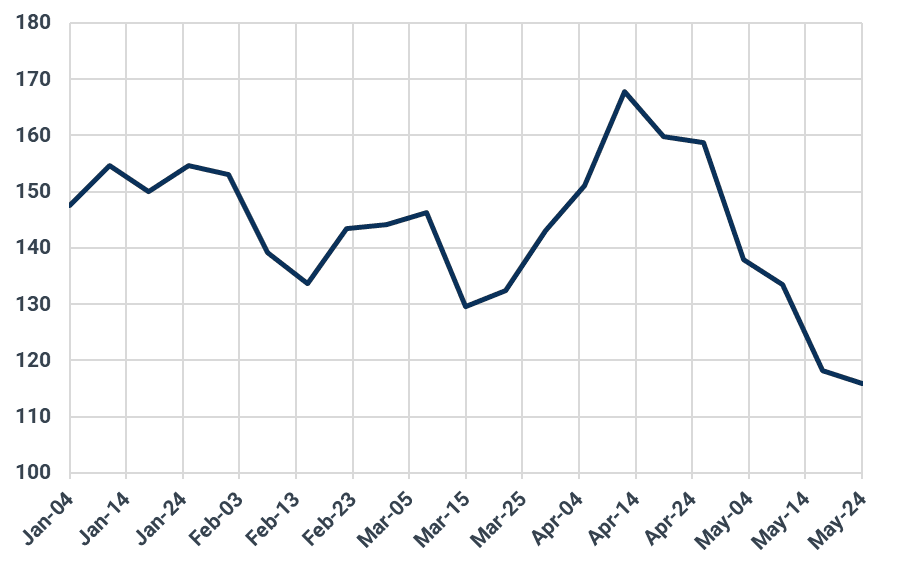

China’s seaborne crude oil imports — including volumes discharged at Myanmar’s Made Island and crude transiting via the pipeline to Yunnan — are forecast to fall to their lowest level in almost a decade at 6.78 mbd, down from 8.5 mbd in April and an average of 10.66 mbd in 2025.

Yet the decline in refinery intake still lags the collapse in imports. Although China’s refinery crude intake has dropped to around 13.5 mbd in May (-154 kbd m/m and -1.92 mbd vs 2025), the decline in demand continues to trail the drop in supplies. As a result, China’s onshore crude inventories have started trending lower in recent weeks, falling to around 1,232 mb from a historical peak of 1,251 mb in early May.

China's onshore crude inventories, mb

Source: Kpler

The pattern is expected to persist in the near term, as refiners continue to keep run rates low while staying on the sidelines of the physical crude market. State-owned refiners — especially Sinopec — are heard to be planning to keep June and July run rates largely unchanged, even as fuel demand typically starts to pick up during the summer season from June onward.

The reluctance to rebuild crude purchases is also tied to increasingly weak downstream economics. High fuel prices and tepid economic activity have dampened oil consumption and accelerated the energy transition in China, raising fears of a lacklustre peak demand season. Market participants told Kpler that state refiners once again failed to meet their transportation fuel sales targets in May, following a grim April. Data from Oilchem shows that China’s commercial gasoline and diesel inventories only recently stopped building, but still remain near two-year highs despite refinery run rates already falling to multi-year lows.

As refiners scaled back procurement of expensive feedstocks and Beijing appeared to be limiting intervention in retail fuel price adjustments, state refiners are now seeing refining margins improve to around -$2/bbl from as low as -$60/bbl in mid-April, according to Oilchem assessments. Even so, margins remain insufficient to incentivise refiners to ramp up production or crude buying.

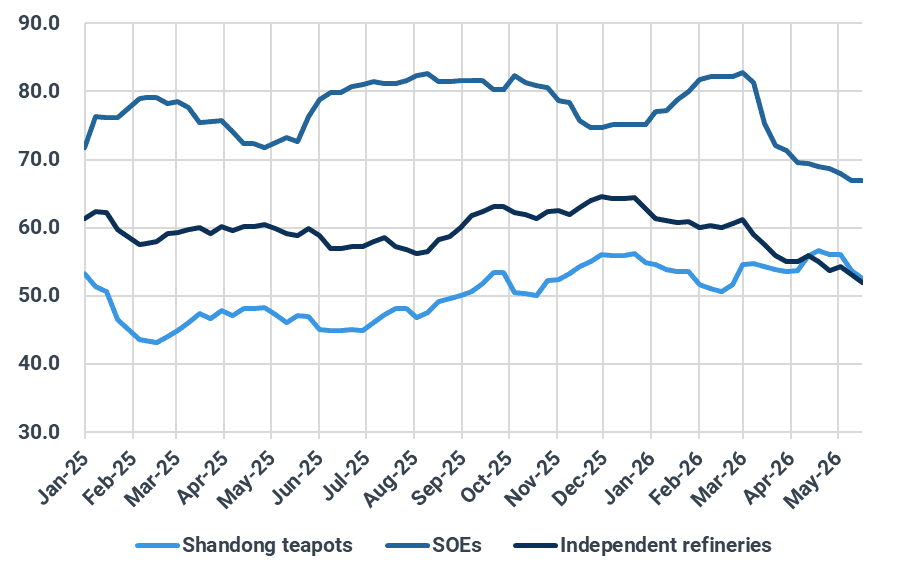

China's refinery run rates by type, %

Source: Oilchem

Media reports suggest that Chinese refiners returned to the physical market in late April after spot premiums for West African and Latin American crude retreated amid softer demand, swiftly snapping up at least 30 mb of July-arrival cargoes. However, the move appears to have been more opportunistic buying than a broader shift in China’s operational strategy.

With Middle Eastern supplies still constrained by the Hormuz closure, China’s state-owned refiners are facing even more limited options than their global peers. Beijing has yet to relax restrictions on Venezuelan buyings while kept the 22.5% tariffs on US crude imports in place.

With Middle Eastern supplies still constrained by the Hormuz closure, China’s state-owned refiners are facing even more limited options than their global peers. Beijing has yet to relax restrictions on Venezuelan crude purchases, while the 22.5% tariffs on US crude imports remain in place.

Russian crude has emerged as a cheaper alternative. However, the latest US sanctions only cover cargoes loaded before April 17, effectively excluding ESPO cargoes arriving after mid-May and Urals cargoes after early June. As a result, state refiners have significantly scaled back new purchases, if not suspended them altogether, leading to an overhang of Russian crude in the Chinese market for both June and even some May-arrival cargoes.

In the meantime, independent refiners have also scaled back spot buying amid a deteriorating margin environment. Prices for both Russian and Iranian crude — which account for the vast majority of their crude slate — have risen sharply, particularly after the US issued temporary sanctions waivers while implementing a blockade on Iranian shipping.

Against this backdrop, some refiners have sought permission from local authorities to lower run rates and have refrained from placing orders at current oil prices. Some market participants told Kpler that crude inventories at most teapots are sufficient to cover demand until early June.

Iranian crude oil on water outside the Persian Gulf and Gulf of Oman, mb

Source: Kpler

That said, if the US were to maintain the blockade on Iranian cargoes, Chinese independent refiners would have to turn to alternative supplies — most likely Russian crude — and compete for barrels currently taken by other buyers such as India. Given elevated prices, they are more likely to further cut run rates, potentially leaving room for state-owned refiners to ramp up operations.

That, however, would require further inventory drawdowns, potentially prompting Beijing to release state oil reserves or step up crude buying.

Chinese refiners are already seen holding tightly to their equity Omani cargoes in the Middle Eastern market in May, in contrast to the active reselling seen in April, suggesting they are already positioning for tighter crude availability ahead.

To borrow a quote commonly attributed to Napoleon, “Let China sleep, for when she wakes, she will shake the world,” the same may hold true in today’s oil market. Once China decides to return to the market — likely affecting July onward-loading cargoes — the balance could quickly shift from “tight” to “significantly tighter”, especially as European and American refiners ramp up operations to meet peak summer demand amid low fuel inventories.

At that point, the market’s current stalemate could quickly unravel, pushing oil prices back toward the levels many had deemed inevitable at the outset of the war.

Market insights you can trust

Kpler delivers unbiased, expert-driven intelligence that helps you stay ahead of supply, demand, and market shifts.

Trade smarter. Request access to Kpler today.

See why the most successful traders and shipping experts use Kpler

.jpg)