China’s lower crude imports helped ease Asian refinery feedstock tightness

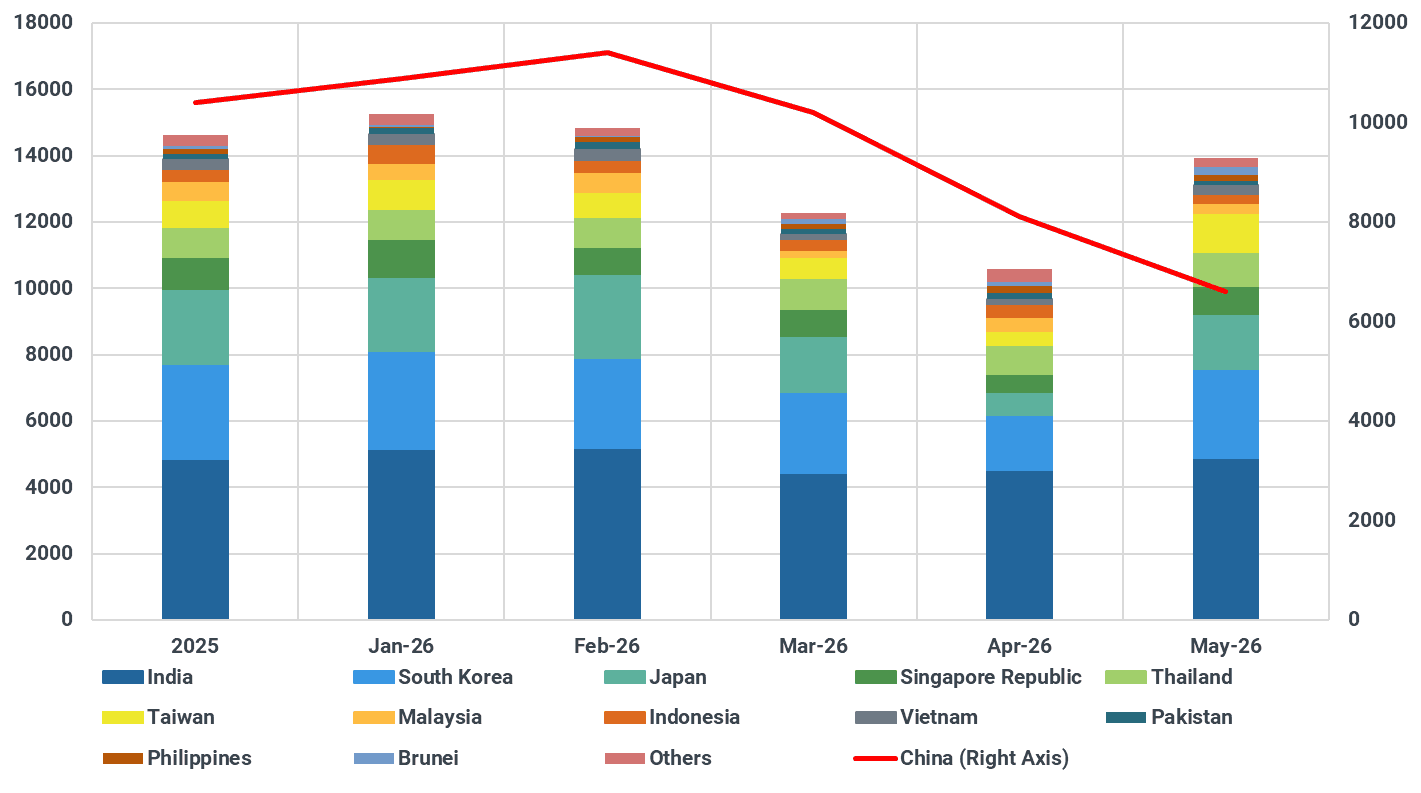

China’s sharp decline in crude imports has unintentionally eased feedstock tightness across Asia, helping refinery runs outside China perform better than previously expected despite ongoing Strait of Hormuz disruptions. Additional availability of Middle Eastern, Russian, West African, and Atlantic Basin barrels supported stronger crude imports into countries such as South Korea, Singapore, Thailand, and India, partially offsetting tighter Gulf flows and preventing a deeper regional supply crunch.

Chinese crude imports in May month-to-date are tracking around 6.6 mbd, the lowest level since 2016. Compared with last year’s average, imports from Russia, Africa, and parts of the Americas have declined materially, effectively freeing additional barrels into the broader Asian market. While weaker Chinese refinery activity and softer product exports have pressured domestic operations, the reduction in crude intake has simultaneously improved crude availability for the rest of Asia.

Asian countries' crude imports (kbd)

Source: Kpler

Note: Data as of 25th May

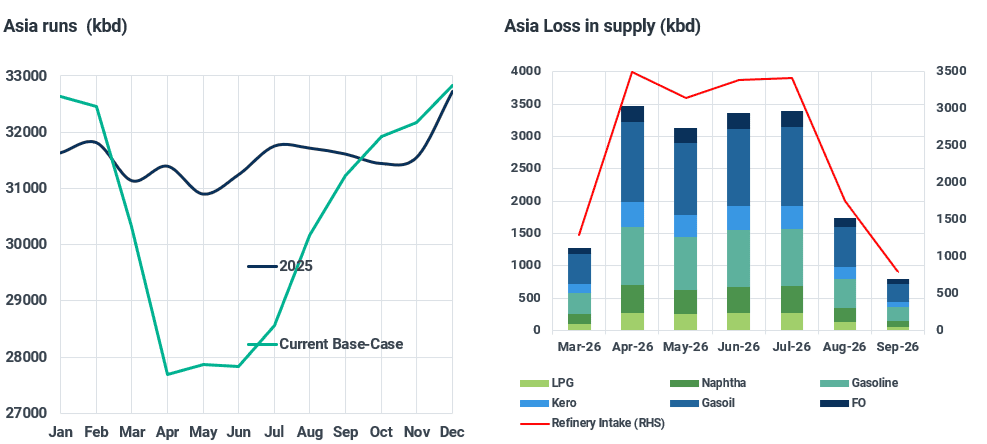

As a result, refiners across South Korea, Japan, Southeast Asia, and India have been able to secure more crude supply than initially expected, allowing refinery throughput to hold up materially better than earlier base-case assumptions despite tighter Middle Eastern flows and Strait of Hormuz disruptions. This has helped Asia (ex-China) refinery runs recover more strongly than initially expected in May, although overall refining activity remains heavily disrupted versus normal conditions. Asia (ex-China) refinery runs are now expected around 14.8 mbd, up roughly 900 kbd m/m, although still around 1.3 mbd below last year’s levels. Looking ahead, a similar rate is expected in June, with Asian (ex-China) runs at around 14.8-15.0 mbd.

Asian refinery runs (kbd)

Source: Kpler

US and African crude flows surge into Asia ex-China

The largest shift has been visible in US crude imports. Asia (ex-China) imports of US crude are currently tracking near an all-time high of around 1.94 mbd in May as regional buyers scrambled to secure barrels from wherever available to manage supply security and offset tighter Gulf availability. A similar trend has emerged for African crude, with Asia ex-China imports also tracking near record highs around 1.7 mbd in May.

South Korea has seen one of the largest increases in crude imports, with May imports rising to around 2.6 mbd, up roughly 1.0 mbd m/m, although still around 450 kbd below last year’s levels. The increase has been largely driven by stronger imports of US and African crude. Singapore and Thailand have also seen a noticeable uptick in crude imports during May as American crude flows into the region surged.

India’s crude imports in May have also remained strong. While the 2025 average stood at around 4.8 mbd, May imports are currently tracking near 5.0 mbd, potentially the highest monthly import in May ever, supported primarily by stronger Russian and Venezuelan crude imports.

Asian downstream activity gains momentum but remains disrupted

Overall, refinery operations across Asia remain heavily disrupted despite some improvement in crude availability in recent weeks. Since the start of the Strait of Hormuz disruption, cumulative crude processing losses across Asia are estimated at around ~2.7 mbd during March–May, significantly impacting fuel production, with gasoil losses around ~940 kbd, gasoline ~700 kbd, and kerosene ~300 kbd. Significant refinery run cuts have been particularly visible in China amid weaker crude imports and softer downstream activity.

Asian downstream disruption (kbd)

Source: Kpler

While some refiners have partly recovered throughput through higher imports of US, African, and Atlantic Basin crude, regional refinery runs remain well below normal seasonal levels and are expected to stay constrained into Q3 under the current base case.

Outlook

Looking ahead, Chinese crude imports will remain a key variable for broader Asian refining balances. If Chinese refinery runs and crude imports remain subdued, Asia ex-China refiners are likely to continue benefiting from relatively improved crude availability and stronger feedstock flows. However, any meaningful recovery in Chinese crude buying could quickly tighten regional balances again, particularly while Strait of Hormuz disruptions and Middle Eastern supply risks remain unresolved.

See why the most successful traders and shipping experts use Kpler

.jpg)