European margins turn negative, raising run cut risks

European refining margins have moved into negative territory, driven by a sharp rally in crude prices that has outpaced product gains. While middle distillate cracks remain strong, weak gasoline economics and elevated feedstock costs are compressing margins across configurations. Although run cuts have not yet materialised at scale, the current economics are increasingly unsustainable, particularly for simple and gasoline-heavy refineries. A rebalancing phase is expected, with tighter product supply likely to support cracks in the near term.

Crude-led squeeze driving margin collapse

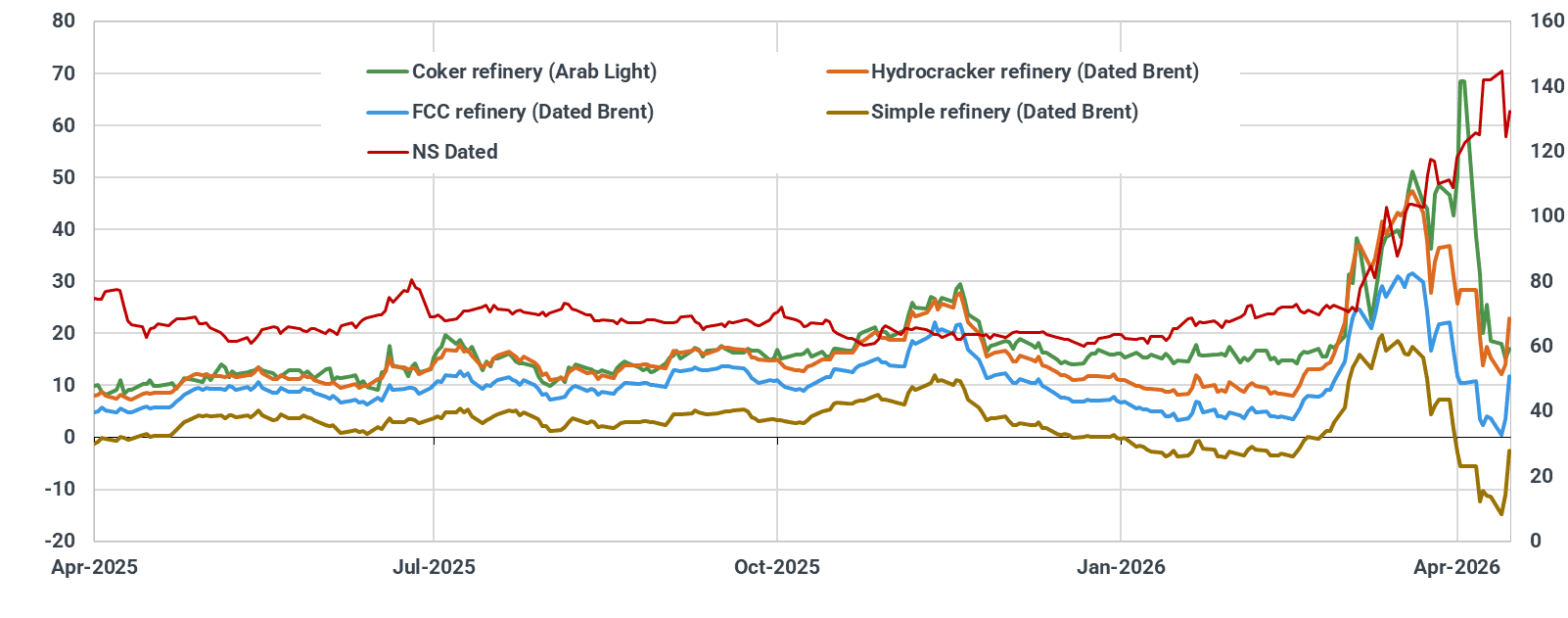

European refining margins have turned negative in recent sessions, reflecting a clear crude-led squeeze rather than a deterioration in product demand. Strength in physical crude benchmarks, particularly Dated Brent and North Sea grades, has pushed feedstock costs sharply higher as Brent landed crossed 130$/b. As a result, Northwest European simple refinery margins have fallen deep into negative territory (minus $10-20/b), while medium (FCC / HCK) and complex configurations have also seen significant compression.

This highlights a growing pricing dislocation, where crude markets have tightened faster than product markets can adjust. At this juncture, margins cannot sustain runs. Either crude must come off (more possibility as traffic through SoH resumes), or cracks must rally – and the path of least resistance points toward tighter product balances, forcing cracks higher.

NWE: refinery margins ($/bbl)

Source: Kpler based on Argus Media

Diverging cracks: distillates vs gasoline

Margin pressure is being amplified by a divergence in product cracks. Middle distillates remain structurally strong, with diesel cracks holding at elevated levels globally and jet fuel cracks even higher, reflecting tight balances. In contrast, gasoline cracks in Europe have weakened significantly and, in some cases, turned negative versus Dated Brent.

This reflects Europe’s structural imbalance, being long gasoline but short middle distillates, leaving it as the key drag on overall margins

Margin compression is now evident across all configurations. Simple refineries are the most exposed due to higher gasoline and naphtha yields, while complex refineries remain relatively more resilient given their ability to maximise middle distillate output. Yield optimisation, shifting away from light ends and bottoms toward distillates, is likely to provide some support, particularly for more complex systems.

Import dynamics point to near-term inflexion

Product flows suggest the market may be approaching a near-term inflexion point. The latest wave of Middle Eastern exports into Europe has largely arrived, and forward inflows from the East are expected to slow, reducing incremental supply pressure.

At the same time, refiners may begin adjusting crude intake if margins remain weak, particularly in regions not structurally long diesel. This combination of reduced imports and potential run adjustments is expected to tighten product balances and support a recovery in product prices and cracks, even if crude remains elevated in the near term.

Run cuts: exposure concentrated in export-oriented systems

Run cut risks are rising, although not yet widespread. The most vulnerable assets are hydro-skimming and FCC-heavy refineries with high gasoline exposure, which are likely to respond first to sustained negative margins.

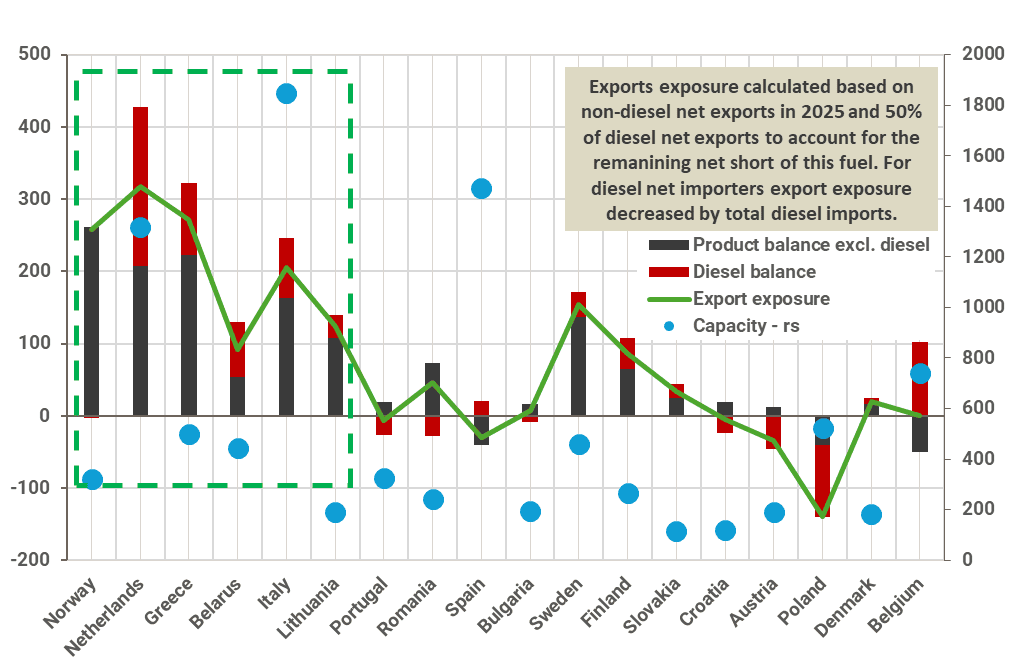

Europe: Export Exposure in Selected Countries and Refining Capacity [kbd]

Source: Kpler

The distribution of export exposure and refining capacity across Europe further highlights where run cut risks are most likely to materialise. Countries such as the Netherlands (runs cuts expectation-75-100 kbd), Norway (25-40 kbd), Finland (25-35 kbd), Sweden (50-70 kbd), Greece (30-50 kbd), and Italy (50-60kbd) stand out with both significant refining capacity and high export exposure, particularly in non-diesel products, making them more vulnerable in the current margin environment. These systems are more reliant on export outlets to clear surplus gasoline and light ends, which are currently under pressure, increasing the likelihood of throughput adjustments. Lithuania and Norway also exhibit relatively high export exposure relative to domestic balances, suggesting that refiners in these markets may face similar pressures, especially if export economics deteriorate further. In contrast, countries with more balanced or structurally short positions in middle distillates, or lower export dependency, are less exposed to immediate run cut risks despite margin compression.

At the same time, policy signals may limit the pace of run cuts. The European Commission has urged refiners to maintain high utilisation and defer maintenance to secure product supply, particularly jet fuel. While margins point toward run cuts, policy intervention could delay or soften reductions.

Overall, the chart indicates that run cut risks are concentrated in export-oriented refining hubs with gasoline-heavy imbalances, where weak product placement and elevated crude costs are combining to erode margins. In these regions, refiners are more likely to respond first through selective run reductions, particularly in simpler configurations, reinforcing the view that any supply adjustment will be uneven and led by structurally long systems rather than across-the-board cuts.

Gradual adjustment and a self-correcting mechanism

Early signs of lower run rates have emerged at select sites, though it remains unclear whether these are economically or operationally driven. Run cuts are expected to develop gradually as a function of margin pressure rather than coordinated action. Sustained negative margins will force refiners to reduce throughput, while high product prices may begin to impact demand at the margin. This creates a self-correcting cycle: lower refinery runs reduce crude demand and tighten product supply, supporting cracks and enabling margins to recover over time.

Conclusion

European refining margins have turned negative due to an extreme crude-led squeeze, with strong distillate cracks insufficient to offset weak gasoline economics and elevated feedstock costs. While widespread run cuts have not yet materialised, the current margin environment is increasingly unsustainable, particularly for simpler configurations.

Run cuts are likely to emerge gradually, led by hydro skimming and gasoline-heavy refineries, tightening product balances and supporting a recovery in cracks. Refining margins will remain the key signal to monitor, as they continue to drive refinery behaviour and broader market rebalancing.

See why the most successful traders and shipping experts use Kpler